Table of Contents

Tax Planning and ITR Filing Tips for Salaried Employees in India (AY 2026–27 Ready Guide)

Tax planning is not about last-minute investments in March 2026. Tax planning is a crucial part of financial management for salaried individuals. With the right strategies, employees can reduce their tax burden, maximize savings, and stay compliant with Indian tax laws. Filing Income Tax Returns accurately and on time further ensures transparency, avoids penalties, and enables timely refunds. Effective tax planning is essential for salaried employees to minimize tax liability and build long-term financial stability. it’s about smart structuring of salary, choosing the right tax regime, and filing your ITR correctly under the Income Tax Act, 1961.

We should follow the practical tax planning strategy for fy 2025-26. We should compare regimes in April, structure salary properly, invest monthly, not yearly, track deductions in Excel, reconcile AIS quarterly, and if capital gains or F&O are involved, calculate properly as per tax law. By understanding tax slabs, claiming deductions, optimizing salary components, and filing ITR on time, individuals can ensure full compliance with tax laws while maximizing financial benefits. Staying updated with evolving tax regulations and taking proactive steps can enhance financial well-being and contribute to long-term wealth creation.

Practical compliance-focused guide for salaried employees in India:

Practical tips to help salaried employees plan taxes better and streamline the ITR filing process. Here’s a practical, compliance-focused guide for salaried employees in India:

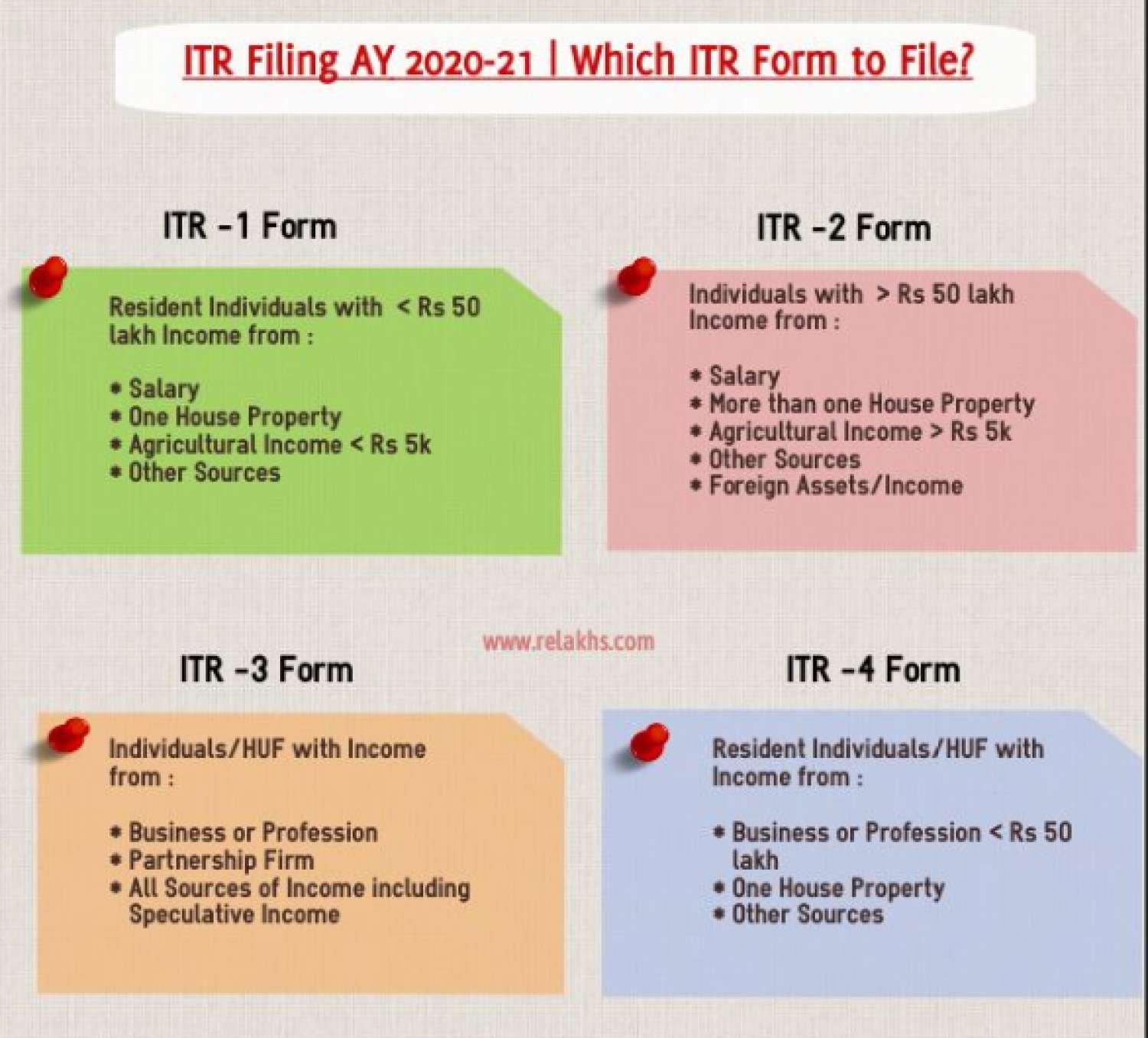

Choose the Right Tax Regime—Old vs New (Section 115BAC) : U/s 115BAC, the New Tax Regime is default, but you can opt for the Old Regime while filing your ITR. New Tax Regime – Suitable If You Don't Claim Many Deductions. Select Correct ITR Form

|

Situation |

ITR Form |

|---|---|

|

Salary + 1 house property + other income |

ITR-1 |

|

Salary + capital gains |

ITR-2 |

|

Salary + business/F&O |

ITR-3 |

Wrong form = Defective return notice u/s 139(9).

Understand Your Salary Structure : Taxpayer Check your Form 16 carefully. Ensure proper tax treatment of basic salary, HRA, LTA, special allowance, employer's PF contribution, and professional tax. Taxpayers must verify PAN is correct, TDS matches Form 26AS, and salary matches AIS/TIS. Your employer hasn’t structured salary with tax-saving components. And You prefer simplicity and lower compliance. And the taxpayer must choose the old tax regime—beneficial if: You claim major deductions like Section 80C (INR 1.5 lakh) – PF, LIC, ELSS, PPF, Home Loan Principal, Section 80D—Health Insurance Premium, Section 24(b)—home loan interest, HRA exemption, and Standard Deduction. If total deductions exceed INR 3–4 lakh, the old regime may be more beneficial. Always compute both before filing. Following are key Sections for salaried employees.

|

Section |

Benefit |

Maximum Limit |

|---|---|---|

|

80C |

Investments (PF, PPF, ELSS, LIC) |

INR 1.5 lakh |

|

80CCD(1B) |

NPS Additional |

INR 50,000 |

|

80D |

Health Insurance |

INR 25,000–INR 50,000 |

|

24(b) |

Home Loan Interest |

INR 2 lakh |

|

80E |

Education Loan Interest |

No limit |

Invest gradually during the year instead of March panic investments.

Know Your Income Tax Slabs and Rates : Understanding the tax slabs applicable for the financial year is the first step in tax planning. Being aware of tax brackets, surcharge limits, rebate eligibility (e.g., Section 87A), and differences between the old and new tax regimes. helps you estimate your tax liability and choose the regime that best suits your income structure.

Make Use of Deductions and Exemptions : The Income Tax Act offers several deductions to lower taxable income. Key ones include:

- Section 80C: PPF, ELSS, LIC premiums, EPF, NSC, principal repayment of home loan (limit INR 1.5 lakh).

- Section 80D: Health insurance premiums for self, spouse, children, and parents.

- Section 80G: Donations to approved charitable institutions.

- Section 80E: Interest paid on education loans.

Using these deductions efficiently reduces overall tax liability.

Optimize Your Salary Structure : Smart salary structuring can significantly reduce taxes. Consider components such as House Rent Allowance, Leave Travel Allowance, meal vouchers/food coupons, conveyance/transport allowance, telephone/Internet reimbursements, and children education and hostel allowance. These components, when structured properly, offer partial or full tax exemption.

If a taxpayer has stock market income, F&O trading, crypto gains, and interest from FD/savings. Taxpayers must report correctly in the appropriate ITR form (usually ITR-2 or ITR-3). Many salaried taxpayers miss reporting Savings interest (Section 80TTA), dividend income, and Foreign assets

Invest in Tax-Saving Instruments : Investments u/s 80C and other sections help with both tax planning and long-term wealth creation. Popular options include Public Provident Fund (PPF), Equity-Linked Savings Scheme, National Savings Certificate, tax-saving fixed deposits (5-year lock-in), and NPS (National Pension System) for additional deductions under 80CCD(1B). Taxpayers must choose instruments based on your risk appetite and financial goals.

Keep Proper Documentation: Taxpayers must maintain organized records of Form 16 from their employer, salary slips, rent receipts, investment proofs, home loan interest certificates, medical bills, insurance premium receipts, and bank statements. Proper documentation ensures hassle-free ITR filing and avoids mismatch notices.

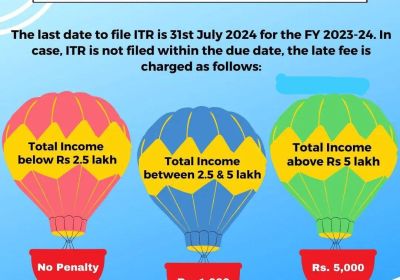

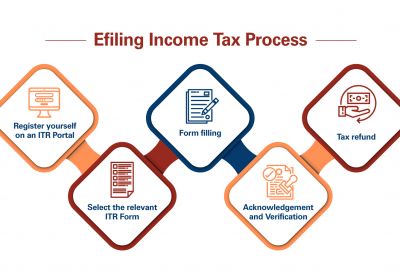

File Your ITR Before the Deadline : The due date for most salaried individuals is July 31st (unless extended by the government). Taxpayer must known that timely filing helps taxpayer Avoid late filing fees (up to INR 5,000 u/s 234F), Claim refunds faster and Maintain financial compliance for visa, loans, and credit purposes. Use the Income Tax Portal or seek help from a tax professional for accurate filing.

Check Your Form 26AS and AIS : Form 26AS, AIS (Annual Information Statement), and TIS (Taxpayer Information Summary) should be checked before filing ITR. They show TDS deducted by employer, TDS on bank interest, High-value transactions and Advance tax or self-assessment tax paid. Taxpayer must ensure all details match your own records to avoid discrepancies.

Use Employee Benefits Wisely : Salaried employees can reduce taxes by leveraging employer-provided allowances:

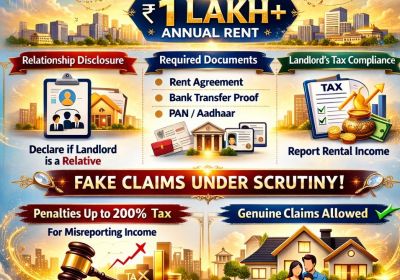

- House Rent Allowance (HRA) : If living in rented accommodation, claim HRA exemption based on salary, rent paid, and city of residence.

- Home Loan Benefits : Section 80C: Principal repayment and Section 24(b): Interest deduction (up to INR 2 lakh for self-occupied property)

- Medical Reimbursements / LTA / Travel Allowances : Use eligible claims to reduce taxable salary.

9. Understand Salary Restructuring : Salary restructuring allows employees to rearrange income components to minimize tax. This includes Increasing tax-free allowances, Utilizing reimbursements, Opting for flexible benefit plans and Choosing tax-friendly perquisites like meal cards or communication reimbursements. Proper restructuring can significantly reduce the taxable portion of your income.

Advance Tax & Self-Assessment Tax : If You have additional income, TDS is insufficient then You may need to pay advance tax (if liability > INR 10,000). Otherwise interest may apply u/s 234B, Section 234C.

Taxpayer must verify Before Filing, taxpayer always reconcile Form 16, Form 26AS, AIS (Annual Information Statement) and Bank interest certificates in case mismatch may trigger notice. Due date for salaried individuals: 31st July (unless extended). Late filing consequences like INR 5,000 late fee (Section 234F), Loss of carry forward of certain losses and Forced New Tax Regime applicability in some cases. Taxpayer must avoid Common Mistakes like Not choosing tax regime consciously, Claiming deduction not reflected in Form 16 without proof, Ignoring AIS entries, Not reporting exempt income and Filing without verification (ITR is invalid unless verified)