Table of Contents

Tax Year – Meaning, Example & Key Changes

What is Tax Year?

A Tax Year is a 12-month period from 1 April to 31 March. Introduced under the Income Tax Act, 2025. Effective from 1 April 2026. Replaces: Financial Year and Assessment Year, Remove confusion and simplify tax understanding. so following are Key Change.

- Old system: Previous Year → Income earned and Assessment Year → Tax paid

- New system: Only “Tax Year” and AY is now referred to as “Succeeding / Subsequent Tax Year”

Section 3 – Definition of “Tax Year” under New Income Tax Act, 2025

- Section 3 simplifies and standardizes the time framework of taxation—enhancing clarity, consistency, and administrative efficiency.

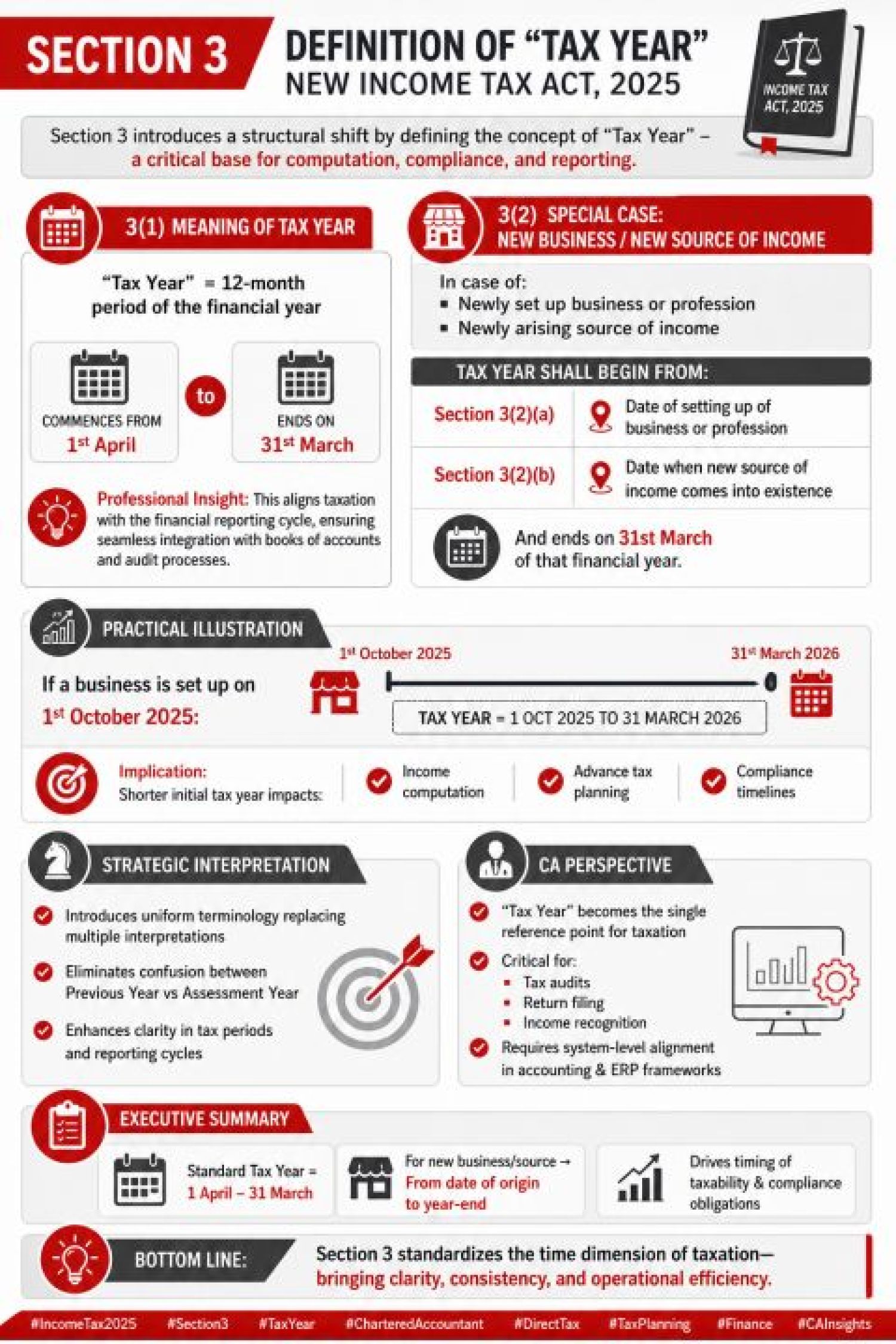

- Section 3 – “Tax Year” Redefined | New Income Tax Act, 2025: Section 3 marks a significant structural reform in the new Direct Tax framework by introducing the concept of a “Tax Year”—the foundation for computation, compliance, and reporting.

- Section 3(1) – Meaning of Tax Year: “Tax Year” refers to a 12-month period aligned with the financial year, begins on 1st April and ends on 31st March. This alignment ensures seamless integration with financial reporting, books of accounts, and audit processes—bringing operational clarity.

Start & End Date :

- Standard Tax Year: 1 April – 31 March

- Example: Tax Year 2026–27 = 1 April 2026 to 31 March 2027

Can Tax Year be less than 12 months?

- Yes, in case of New business/profession, New source of income. Example: Business starts on 1 June 2026. Tax Year = 1 June 2026 to 31 March 2027

“Tax Year” becomes the central anchor for all tax provisions, and key impact areas include Tax audits, return filing, and income recognition. Tax year requires alignment of accounting systems and ERP frameworks. A shortened initial tax year impacts income computation, advance tax liability, and compliance timelines. Practical Illustration: If a business is established on 1st October 2025: Tax Year = 1 October 2025 to 31 March 2026

Section 3(2) – Special Cases: New Business / New Source of Income

In case of: A newly established business or profession. A new source of income arising during the year. The Tax Year shall commence from:

- Section 3(2)(a): Date of setting up of business/profession.

- Section 3(2)(b): Date when the new source of income originates.

- It will end on 31st March of the same financial year

- Establishes a single, uniform reference period.

- Removes the dual concept of Previous Year vs Assessment Year

- Enhances clarity in tax computation and reporting cycles

- Standard Tax Year: 1 April – 31 March

- For new business/source: From inception date to year-end

- Directly influences timing of taxability and compliance

Comparison (Old vs New in Tax Year)

|

Aspect |

Tax Year (New Law) |

Old Law |

|

Concept |

Single term |

FY + AY |

|

Purpose |

Income + tax reference |

Separate for earning & taxation |

|

Complexity |

Simple |

Confusing for taxpayers |

|

Filing |

After Tax Year |

In Assessment Year |

Impact on Taxpayers Tax Year

No change in return filing timelines, no change in tax calculation method, significant reduction in confusion, and better clarity for compliance, reporting, and interpretation. The introduction of a tax year is a conceptual simplification, not a structural overhaul of tax liability. It improves clarity by replacing dual terminology with a single reference period.