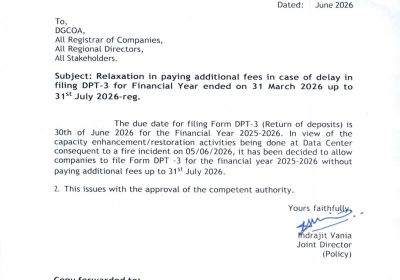

MCA Extends DPT-3 Filing Due Date to 31 July 2026

MCA Extends DPT-3 Filing Due Date, Extends DPT-3 date, MCA Extends DPT-3 Filing Due Date to 31 July 2026, Companies may file Form DPT-3 for the financial ...

Read More Amalgamation as defined in section 2(IB) of the income tax act 1961 is coming together of two or more companies with the aim of forming a new company. The proceedings undertaken are the same except that the surviving entity incorporates the asset base of other into its base. The shareholders of the respective companies will now be identified as shareholders of the new amalgamated company. It has gripped the world lately and is an excellent move in formation of a strong, stable and broad company. The initiatives are undertaken mutually for the expansion and growth of the company. The amalgamation may be preferred in the following cases:

Amalgamation as defined in section 2(IB) of the income tax act 1961 is coming together of two or more companies with the aim of forming a new company. The proceedings undertaken are the same except that the surviving entity incorporates the asset base of other into its base. The shareholders of the respective companies will now be identified as shareholders of the new amalgamated company. It has gripped the world lately and is an excellent move in formation of a strong, stable and broad company. The initiatives are undertaken mutually for the expansion and growth of the company. The amalgamation may be preferred in the following cases:

A company having vulnerable nature may prefer Amalgamation company as security backup. Walking by the phrase “union is strength” the companies adopt potential measures.

We provide highly substantial and effective amalgamation services to business enterprises by supporting the clients in mergers and acquisition process. Our Amalgamation services are available at reasonable price considering the small business companies in the market. We are recognized as one if the best service providers in Virtual Amalgamation Domain in India.

We are dedicated to leave no stone unturned in helping clients achieving world class operations and help the clients in managing risks from boardroom to the network. We develop define and help implement operational strategies for surging the performance level to an appreciable extent.

200+

550+

2009

700+

MCA Extends DPT-3 Filing Due Date, Extends DPT-3 date, MCA Extends DPT-3 Filing Due Date to 31 July 2026, Companies may file Form DPT-3 for the financial ...

Read More

Risk-Based Physical Verification by MCA , MCA Form Consolidation, ROC Form Consolidation, Companies (Incorporation) Amendment Rules, 2026, SPICe+ & DIN Reforms, Registered Office & Verification, Flexible Address Proof (Rule 25 ...

Read More

Roll out a new auditing regime aligned with global standards, 40 auditing standards proposed by NFRA. India’s New Audit Regime, Standard on Auditing 600, principal auditors ...

Read MoreWe are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

All the information related to any client is considered confidential and never be disclosed to anyone.

Having years of experience in respective areas and backed by skilled and experienced workforce keep us ahead.

We believe in the building the good relationship with the clients that ensures the great impression.

If you are not happy with our services then you can request a refund within 30 days.

We provide 24*7 supports through phone, email and live chat.

You can pay online through EMIs, PayPal, net banking, debit card, credit card and more.

We are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

© 2016 Rajput Jain & Associates. All Rights Reserved | Sitemap