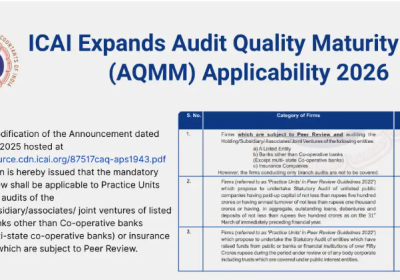

Table of Contents

Banking Fraud on Government-Sponsored Schemes & Dormant Accounts in Banks

Banking frauds have evolved in sophistication, particularly in areas involving government-sponsored schemes and dormant accounts. These segments, designed to promote financial inclusion and welfare distribution, are increasingly being exploited due to control weaknesses and operational gaps. Recent audit observations highlight the need for enhanced monitoring, stronger internal controls, and proactive fraud detection mechanisms.

Strengthening Fraud Detection in Govt-Sponsored Loan Schemes

Fraud in government-sponsored loan schemes has become an emerging concern in the banking sector. Recent internal advisories highlight how forged invoices, fake quotations, and diversion of funds are being used to exploit these schemes.

Key Fraud Patterns Observed like Banks have identified several recurring irregularities. Submission of forged invoices and quotations, loans sanctioned without proper verification, diversion or misuse of funds, and lack of post-disbursement monitoring. Such weaknesses expose not just financial risks, but also reputational damage for institutions.

Where the System Failed. One of the most critical observations is that these frauds remained undetected during audits over multiple years. There was insufficient scrutiny at the sanction and post-disbursement stages. This clearly signals the need for stronger audit frameworks.

Recommended Control Measures:

Auditors and bank officials must ensure Verification of loan documents (quotes/invoices authenticity), Physical inspection of financed assets, Monitoring of end-use of funds and Strengthening sanction and disbursement checks

Fraud prevention begins where verification is strongest. A proactive audit approach and detailed field-level validation are essential to safeguard government-backed funding programs.

Dormant Accounts—A Hidden Gateway to Financial Frauds

Dormant or inoperative accounts present a significant vulnerability in banking systems. Fraudsters often exploit these accounts to execute unauthorized transactions.

How Dormant Accounts Are Misused: Recent findings reveal fraudulent activation of dormant accounts, Unauthorized withdrawals after activation, and use of biometric manipulation for authentication. These activities often occur due to weak monitoring mechanisms. Critical risk areas are mentioned here under the following: Banks must focus on improper account reactivation procedures, lack of customer consent verification, weak KYC compliance during activation, and poor monitoring of activities post activation.

Preventive Measures

To minimize risks Strengthen account activation protocols; auditors ensure customer consent verification. Monitor unusual transactions immediately after activation and conduct periodic audits of inactive accounts. Dormant accounts should never be treated as low risk. Instead, they should be classified as high-risk zones requiring strict surveillance and continuous audit checks.

Role of Auditors in Detecting Banking Frauds – From Compliance to Vigilance

The role of auditors has evolved significantly—from passive reviewers to active fraud detectors. Modern banking frauds require a deeper level of vigilance and analytical scrutiny. Key Areas Auditors Must Focus On

User Login & System Access Controls

- Monitor unauthorized login attempts

- Check for system access by non-branch users

- Ensure proper user ID enable/disable controls

Maker-Checker Mechanism

- Verify adherence to maker-checker controls

- Identify transactions processed by:

- Absent staff

- Transferred employees

Early Warning Signals (EWS) :

Auditors should actively track:

- High-value or unusual transactions

- Repetitive transactions handled by same employees

- Frequent override or exception approvals

- Abnormal transaction patterns

Internal Control & Supervision

- Audit job rotation compliance

- Check inter-branch transactions with anomalies

- Identify suspicious operational patterns

Importance of Immediate Reporting:

A crucial expectation Do not wait for audit completion and Report fraud or suspicious activities immediately. This helps in minimizing financial losses and preventing further damage. Auditors today are the first line of defense against fraud. Moving beyond checklist audits to risk-based auditing is the need of the hour.

Conclusion

Frauds in government-sponsored schemes and dormant accounts underline the urgent need for Stronger internal controls. Risk-based audit approaches, Real-time monitoring systems and enhanced accountability at all levels. Banks must shift from a reactive to a preventive approach, where early detection and swift action form the cornerstone of fraud risk management. Areas perceived as low-risk, like dormant accounts or subsidized schemes, often become the most exploited. Vigilance, not assumption, is the best control.