Important GST Limits Every Business Must Know

The Goods and Services Tax is not just about filing returns. It’s about tracking critical limits and thresholds that directly affect taxpayer registration status, input tax credit, cash flow, interest & penalties, and also departmental scrutiny.

Goods and Services Tax compliance is not complicated, but it is unforgiving of ignorance. We observed the most common Goods and Services Tax mistakes. Businesses make by Goods and services tax Taxpayers like Ignoring turnover thresholds, missing input tax credit cut‑off dates, not monitoring invoice applicability, Delayed return filing & tax payment and weak internal compliance tracking. Knowing and tracking these limits helps taxpayers protect input tax credit, avoid interest & penalties, prevent registration issues, and stay audit-ready. Strong Goods and Services Tax compliance starts with knowing your limits.

Once we are missing these, limits can result in input tax credit loss, penalties, blocked e waybills, or cancellation of registration. Let’s simplify the most important Goods and Services Tax limits

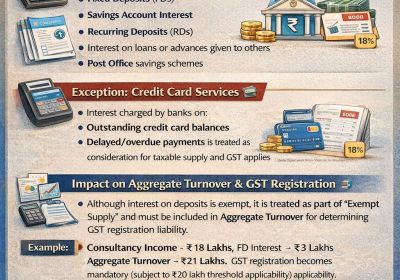

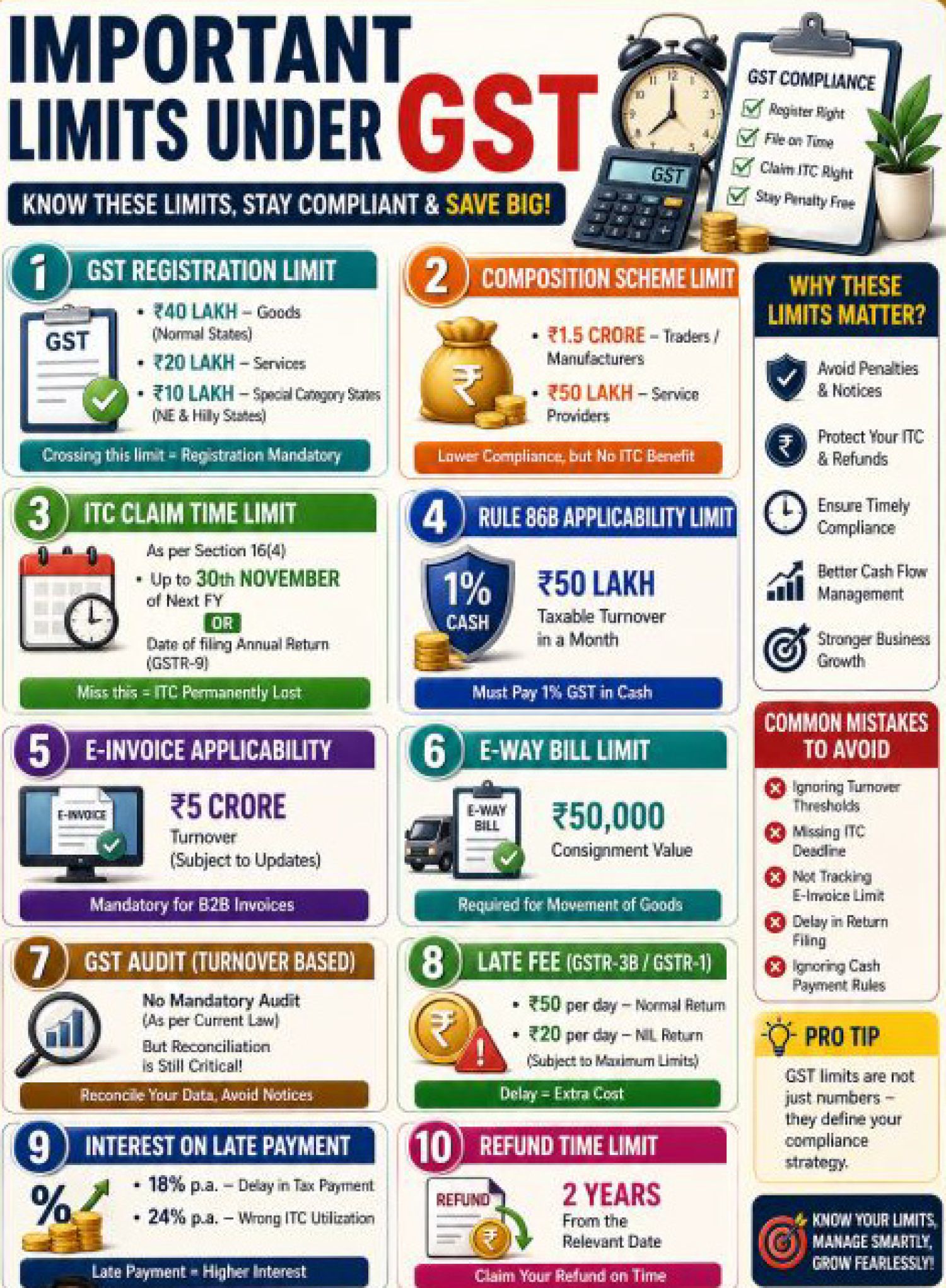

GST Registration Threshold: Goods and Services Tax registration becomes mandatory once turnover crosses the following:

- INR 40 lakh – Supply of goods (Normal States)

- INR 20 lakh – Supply of services

- INR 10 lakh – Special Category States

Crossing the limit = Compulsory Goods and Services Tax registration

Composition Scheme Turnover Limit:

For opting simplified Goods and Services Tax compliance:

- INR 1.5 crore – Traders & Manufacturers

- INR 50 lakh – Service providers

Important trade‑off: Lower compliance, no input tax credit, and cannot charge goods and services tax on invoices.

Input Tax Credit Claim Time Limit (Section 16(4)):

Input Tax Credit can be claimed up to the earlier of 30th November of the next financial year OR the date of filing the annual return (GSTR‑9). Missing this deadline = Permanent ITC loss

Rule 86B – Cash Payment Restriction:

Applicable when taxable turnover exceeds INR 50 lakh in a month, then at least 1% of GST liability must be paid in cash (subject to notified exceptions). Designed to curb fake input tax credit usage.

E Invoicing Applicability Limit:

INR 5 crore turnover (PAN‑based, subject to notifications). Mandatory for B2B invoices under e invoicing, and non compliance = invoice invalid + input tax credit blocked.

E Waybill Requirement:

If consignment value exceeds INR 50,000, an e way bill is required for movement of goods, and non-generation may lead to detention of goods and penalty under Goods and Services Tax.

Goods and Services Tax Audit Current Position:

Turnover‑based mandatory GST audits are abolished. However, reconciliation is still critical, GSTR‑9C (self‑certified) required where applicable, and GST Departmental audit can still happen

Late Fee for Goods and Services Tax Returns: GSTR 3B / GSTR 1

- INR 50 per day – Normal return

- INR 20 per day – NIL return

Subject to maximum caps notified from time to time

Interest in Late Payment / Input Tax Credit Issues

- 18% p.a. – Delay in payment of tax

- 24% p.a. – Wrong ITC availment & utilization

Interest is automatic; no notice is required.

Goods and Services Tax Refund Time Limit:

Two years from the relevant date. Goods and Services Tax refund applies to export refunds, excess tax paid, and input tax credit accumulation. Delay beyond limitation = refund rejected

Summary of GST Limits Every Business

- Goods and Services Tax Registration Threshold: INR 40 Lakhs – Goods and INR 20 Lakhs – Services

- Composition Scheme: INR 1.5 Crore – Traders/Manufacturers and INR 50 Lakhs – Service Providers

- E-Invoicing Applicability: Mandatory if turnover exceeds INR 5 Crore

- E-Way Bill Requirement: Required when consignment value exceeds INR 50,000

- HSN Code Reporting: Up to INR 5 Crore – 4-digit HSN and Above INR 5 Crore – 6-digit HSN

- Input Tax Credit Claim Deadline: 30th November of the next financial year

- Rule 86B (Restriction on Input Tax Credit Usage): Minimum 1% GST to be paid in cash. Applicable if taxable turnover exceeds INR 50 lakhs/month.

- Goods and Services Tax Refund Time Limit: Claim within 2 years

- Revocation of Goods and Services Tax Cancellation: Apply within 90 days

- Rule 14A (Liability Threshold): B2B output liability up to INR 2.5 Lakhs

- Annual Return (GSTR-9): Optional up to INR 2 Crore turnover

- Reconciliation Statement (GSTR-9C): Mandatory if turnover exceeds INR 5 Crore

- Tax Deducted at Source under Goods and Services Tax: Applicable when contract value exceeds INR 2.5 Lakhs