INCOME TAX

F&O Trading Income Tax: Complete Guide for Traders

RJA 30 Jul, 2026

F&O Trading Income Tax: Complete Guide for Traders Income earned from futures & options trading is generally treated as business income under the Income Tax Act. Therefore, traders are required to report such income in ITR-3. Taxpayers opting for the presumptive taxation scheme and fulfilling the prescribed conditions ...

INCOME TAX

Declaration of Foreign Assets and Income: Compliance for Resident Taxpayers

RJA 16 Jul, 2026

Declaration of Foreign Assets and Income: A Critical Compliance Requirement for Resident Taxpayers Introduction With increasing globalization, many Indian residents earn income from overseas sources or hold assets outside India, such as foreign bank accounts, shares, ESOPs, properties, trusts, and investment portfolios. The Income Tax Department has reiterated the importance ...

INCOME TAX

CBDT to Display Foreign Financial Information in AIS: For NRIs

RJA 12 Jul, 2026

CBDT to Display Foreign Financial Information in AIS: What NRIs, Returning Indians & Global Taxpayers Need to Know CBDT will now display foreign financial information received under CRS, FATCA, and AEOI in AIS. Learn the impact on NRIs, RNORs, returning Indians, foreign asset reporting, DTAA, and tax compliance. Introduction In ...

Chartered Accountants

ICAI Membership Benefits – Exclusive Advantages for Chartered Accountants

RJA 08 Jul, 2026

ICAI Membership Benefits – Exclusive Advantages for Chartered Accountants ICAI was established under an Act of Parliament that empowers ICAI members. Enriching Lives. The Institute of Chartered Accountants of India (ICAI) continues to enhance the professional ecosystem for chartered accountants by offering a wide range of member-centric ...

INCOME TAX

Explained Simply: Form 10-IEA Requirement at a Glance

RJA 28 Jun, 2026

Explained Simply: Form 10-IEA Requirement at a Glance This blog explains when Form 10-IEA is required for taxpayers having business or professional income who wish to opt out of the new tax regime and switch to the old tax regime (OTR). We have to understand the Important Rule for Form 10...

Chartered Accountants

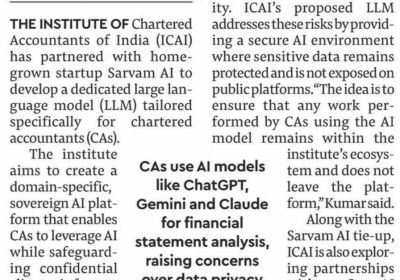

ICAI & Sarvam AI to Develop a Dedicated AI Model for CA

RJA 28 Jun, 2026

ICAI & Sarvam AI to Develop a Dedicated AI Model for Chartered Accountants: A Game Changer for the Profession Artificial intelligence is rapidly transforming the accounting and finance profession. Chartered accountants today increasingly use artificial intelligence tools such as ChatGPT, Gemini, and Claude for research, tax advisory, compliance reviews, audit ...

INCOME TAX

Income tax Rules when Assets Transferred to Family Clubbing of HUF Income

RJA 28 Jun, 2026

Income tax Rules When Assets Transferred to Family—Clubbing of HUF Income Is it a gift to the Hindu Undivided Family by a clubbed member? Yes. If a member transfers or gifts personal assets (cash, property, shares, etc.) to the Hindu Undivided Family without adequate consideration, the income ...

INCOME TAX

NFRA Reporting (Audit Quality & Documentation) Normal finding

RJA 26 Jun, 2026

NFRA Orders, Audit Documentation & Audit Quality normal finding: The inspections indicate recurring weaknesses in four critical areas like independence and ethics, audit documentation, audit evidence, professional skepticism, and quality control systems (SQC-1/SQM). The National Financial Reporting Authority's clear message is "If it is not documented, it ...

Business Setup in India

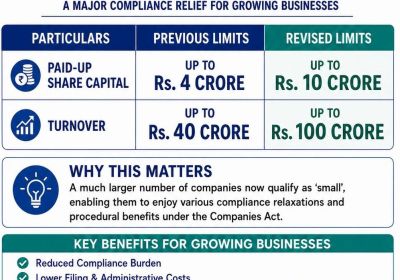

Change in Small Co. Limits: Major Compliance Relief for Businesses

RJA 26 Jun, 2026

Major Compliance Relief for Growing Businesses The Ministry of Corporate Affairs has taken a significant step towards ease of doing business by expanding the definition of a "small company" under the Companies Act, 2013. This revision is expected to bring thousands of growing companies within the ambit of small ...

NGO

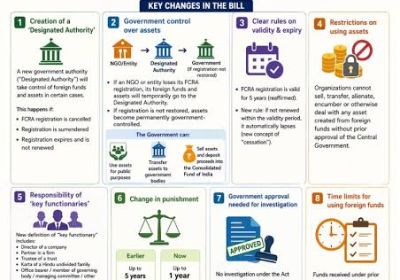

FCRA Update – Foreign Contribution (Regulation) Amendment Rules, 2026

RJA 25 Jun, 2026

FCRA Update – Foreign Contribution (Regulation) Amendment Rules, 2026 The Ministry of Home Affairs (MHA) has notified the Foreign Contribution (Regulation) Amendment Rules, 2026 on 22 June 2026, bringing significant changes to the compliance framework for NGOs and other organizations receiving foreign contributions. The amendments became effective immediately upon publication in the Official Gazette. ...

INCOME TAX

Guide covers due dates for ITR, TRA & Belated ITR for tax year 2026-27

RJA 24 Jun, 2026

Income Tax Due Dates & Return of Income (AY 2026-27 / TY 2026-27): Complete Compliance Guide Timely filing of Income Tax Returns (ITR) and compliance with audit requirements are crucial for taxpayers to avoid penalties, interest, and other adverse consequences under the Income Tax Act. With different due dates applicable to ...

COMPANY LAW

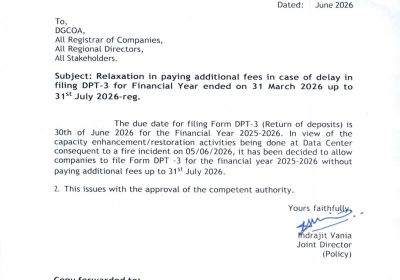

MCA Extends DPT-3 Filing Due Date to 31 July 2026

RJA 19 Jun, 2026

MCA Extends DPT-3 Filing Due Date to 31 July 2026 In a significant compliance relief measure, the MCA has issued General Circular No. 02/2026 dated 19 June 2026 bearing F. No. Policy-02/2/2020-CL-V-MCA, allowing companies to file Form DPT-3 (Return of Deposits) for FY 2025-26 without payment of additional fees up to 31 July 2026. The ...

Income tax return

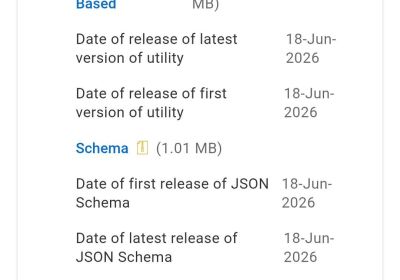

Income Tax Update | ITR-3 Utility Released

RJA 19 Jun, 2026

Key Update: ITR-3 Excel Utility Released for AY 2026-27 The Income Tax Department has released the Offline & Excel Utility for ITR-3 for AY 2026-27. ITR-3 is applicable to individuals and HUFs having income from profits and gains of a business or profession. Excel Utility Version: 1.0, Release Date: 18 June 2026, Offline ...

INCOME TAX

ITR-6 Guide for Companies Filing ITR for AY 2026-27 (FY 2025-26)

RJA 08 Jun, 2026

ITR-6 Complete Guide for Companies Filing ITR for AY 2026-27 (FY 2025-26) ITR-6 is the income tax return form prescribed for companies registered in India to report their income, deductions, tax liability, and various financial disclosures under the Income Tax Act, 1961. This return form is applicable to companies that ...

Financial Services

Valuation for Impairment Testing – A Comprehensive Guide under Ind AS 36

RJA 08 Jun, 2026

Valuation for Impairment Testing – A Comprehensive Guide under Ind AS 36 In today’s dynamic business environment, assets may lose value due to market disruptions, technological changes, economic slowdowns, regulatory developments, or operational inefficiencies. Financial reporting standards therefore require entities to ensure that assets are not carried in the ...

FIU IND

Current Position of Virtual Digital Assets (VDAs) in India

RJA 02 Jun, 2026

Current Position of Virtual Digital Assets (VDAs) in India Virtual digital assets are recognized u/s 2(47A) of the Income-tax Act primarily for taxation purposes. Transfers of Virtual digital assets are subject to 30% tax on gains, 1% TDS on transfer consideration, and no set-off of losses against other income. There ...

FIU IND

Overview on Obligations of Financial Sector Entities under PMLA, 2002

RJA 29 May, 2026

Overview on Obligations of Financial Sector Entities under PMLA, 2002 About FIU-IND Financial Intelligence Unit – India (FIU-IND) is the central national agency responsible for Receiving and analyzing financial transaction reports and sharing intelligence with law enforcement agencies. It works towards combating money laundering and Terrorist financing . Filing is done through ...

Chartered Accountants

ICAI’s Forensic Auditing Lab: What It Really Means for CA’s

RJA 27 May, 2026

ICAI’s Forensic Auditing Lab: What It Really Means for Chartered Accountants The accounting profession in India is quietly entering a major transformation phase. For years, forensic audits, fraud investigations, and technology-led assurance assignments remained concentrated within large consulting networks and Big 4 firms due to one major barrier: High ...

INCOME TAX

Income Tax Rules – Key Cash Transaction Limits in India

RJA 21 May, 2026

Income Tax Rules – Key Cash Transaction Limits in India Cash transactions under the Income-tax Act are subject to strict limits. Non-compliance may lead to expense disallowance, 100% penalty exposure, and tax scrutiny. 1. Cash Expense Limit – Sec 40A(3) • Cash payment above INR 10,000 per day per person is generally not ...

Chartered Accountants

Latest ICAI UDIN Changes for TAR (Section 44AB(e) Checklist & More)

RJA 20 May, 2026

Big Changes in Checklist & Reporting Enhancements in ICAI UDIN System/Portal for Tax Audits New Checklist & Reporting Enhancements under ICAI UDIN System ICAI has made key updates introduced by the Institute of Chartered Accountants of India in the Unique Document Identification Number system to strengthen compliance and ensure ...

AUDIT

Banking Fraud on Govt.-Sponsored Schemes & Dormant A/cs in Banks

RJA 08 May, 2026

Banking Fraud on Government-Sponsored Schemes & Dormant Accounts in Banks Banking frauds have evolved in sophistication, particularly in areas involving government-sponsored schemes and dormant accounts. These segments, designed to promote financial inclusion and welfare distribution, are increasingly being exploited due to control weaknesses and operational gaps. Recent audit observations highlight ...

INCOME TAX

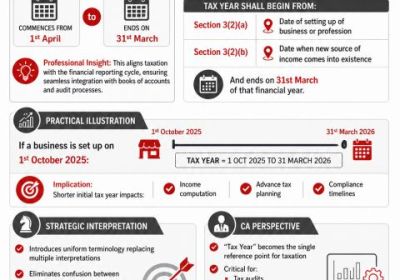

Tax Year – Meaning, Example & Key Changes

RJA 07 May, 2026

Tax Year – Meaning, Example & Key Changes What is Tax Year? A Tax Year is a 12-month period from 1 April to 31 March. Introduced under the Income Tax Act, 2025. Effective from 1 April 2026. Replaces: Financial Year and Assessment Year, Remove confusion and simplify tax understanding. so following are Key Change. Old ...

Goods and Services Tax

Goods & Services Tax Loopholes & Fraud Areas in India

RJA 03 May, 2026

Goods & Services Tax Loopholes & Fraud Areas in India Goods & Services Tax fraud largely revolves around fake Input Tax Credit, fictitious entities, refund abuse & turnover suppression, while classification & Input Tax Credit eligibility continue to drive interpretational disputes & litigation. Challenges faced to overcome fake ...

Goods and Services Tax

Overview GST Returns & Compliance in India

RJA 03 May, 2026

Overview GST Returns & Compliance in India Timely Goods and Services Tax compliance helps businesses to avoid penalties and notices, ensure smooth input tax credit flow, maintain good compliance ratings, and prevent business disruptions (e‑way bill blocking, registration suspension). This blog guide about what Goods and Services Tax returns ...