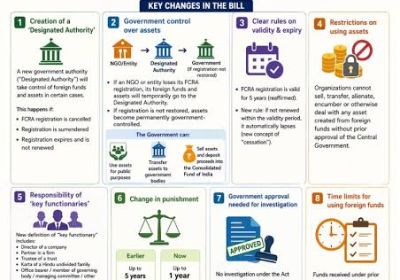

Organizations listed under the Foreign Contribution Regulation Act must hold different

records under the head office of the FC and give a report in the prescribed template to the

Ministry along with the audited report of records of the previous year. Any company

obtaining foreign donations is expected to have a certificate from a CA. The certificate to

be issued by the CA is offered in the form FC-6. In addition to this document, the audited

Balance Sheet, Revenue & Expense Statement and the collection and payment account statement,

together with the certification and verification approved by the Chief Functionary, will

also be issued.

Quick, Simple & Safe Way Annual FCRA return...

FCRA Annual Returns process can be complex.

We can make this simple & Hassle Free

Step by step assistance

For Business-man & Consultants

Our services are quick & affordable

The return is to be submitted for each financial year (1st April to 31st March) within 9

months of the end of the year, i.e. by 31st December of each year. The filing of a ' 0 '

refund, even though no international donation is received / used throughout the year, is

compulsory. The report shall be issued in the specified form FC–6 accordingly followed by

the balance sheet and the revenue and expenditure statement approved by the Chartered

Accountant. On the grounds of the appropriate accounts and receipts, the chartered

accountant is expected to report the following: