Table of Contents

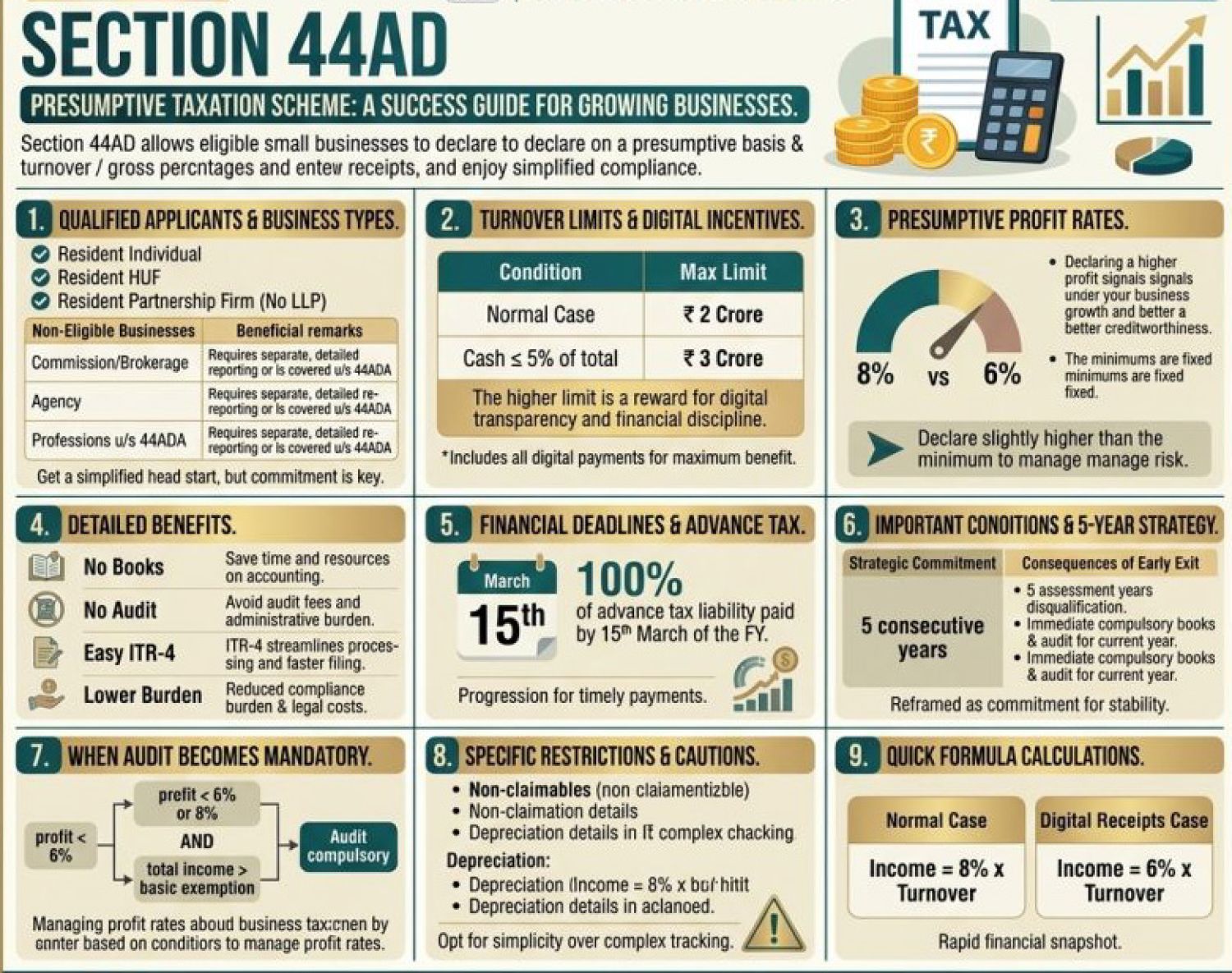

Guide to the Presumptive Taxation Scheme (Section 44AD) (FY 2025 2026)

A tax audit is required to become mandatory; if the tax audit is mandatory, the audit becomes mandatory if taxpayers opt out of 44AD and the declared income is below 6% / 8% and the total income exceeds the basic exemption limit. Then books of accounts are compulsory, and audit u/s 44AB is mandatory. Taxpayers declare a profit below 6% or 8%, and the taxpayer's total income exceeds the basic exemption limit. So, we can say that Total income > exemption limit → Audit required.

For small businesses focused on growth and simplified compliance, Section 44AD under the Income Tax Act offers an efficient, hassle‑free alternative to regular accounting and income tax audit requirements.

Section 44AD is a powerful compliance‑reduction tool, especially for digitally compliant small businesses. But it comes with serious consistency requirements. Always evaluate taxpayers' realistic profit margins, five-year cash flow and growth plans, and banking and credit expectations.

It is to be remembered that no separate deductions are allowed for business expenses. Depreciation is deemed allowed (block value should be reduced); a partner's remuneration & interest are not allowed in presumptive income, advance tax must still be paid, and only business income can be declared under 44AD (not professional income). Below is a complete and updated breakdown.

Eligible Taxpayers & Business Types

- Eligible: Resident Individuals, Resident Hindu Undivided Families (HUFs), and Resident Partnership Firms (excluding LLPs).

- Not Eligible: Businesses earning commission or brokerage; agency businesses; professionals covered u/s 44ADA (CA, doctor, architect, etc.); non-resident taxpayers; and LLPs.

- Section 44AD is a powerful compliance‑reduction tool, especially for digitally compliant small businesses. But it comes with serious consistency requirements.

New Turnover Limits: INR 2 Crores vs INR 3 Crores

The Finance Act has provided a major incentive to digital businesses.

General Limit: Applicable to businesses with turnover up to INR 2 Crores

Enhanced Limit (Digital‑Driven Businesses): Increased to INR 3 Crores, provided. Aggregate cash receipts ≤ 5% of total turnover/gross receipts. Moreover, if cash receipts exceed 5%, eligibility reverts to INR 2 crores. This higher limit rewards businesses that adopt digital payments and transparent accounting practices.

Presumptive Profit Rates (Receipt Based):

Instead of maintaining books, taxable income is computed at a fixed percentage of turnover: presumptive income is computed based on the mode of receipt, not merely invoicing.

- 6% of Turnover: 6% of Turnover → If digital receipts are ≥ 95% or more of the total. Applicable for receipts received via account payee check, account payee bank draft, ECS, and any prescribed electronic/digital mode. Receipt must be credited before the due date of filing the return under Section 139(1).

- 8% of Turnover: 8% of Turnover → If cash receipts exceed 5%. Applicable for cash receipts or any non‑digital mode. 6% & 8% are minimum benchmarks; higher income may be declared voluntarily.

- The 6% / 8% rates are minimum presumptive rates. Taxpayers declare 10%, 12%, or 15% or any higher actual income. Declaring a much lower income than evident lifestyle/investments may invite assessment scrutiny.

No Deduction” Rule (Sections 30 to 38):

When Section 44AD is opted for, no further deduction is allowed for rent, salary, electricity, repairs, and depreciation (Sections 30 to 38). However, depreciation is deemed to have been allowed, and the WDV of assets must be reduced accordingly, even though no explicit deduction is claimed. Partner’s remuneration and interest ARE allowed, and as per Section 40(b), deduction is permitted from presumptive income in the case of partnership firms.

This prevents double benefits in future years. Books of accounts become mandatory, and tax audits under Section 44AB become compulsory.

Restrictions u/s 44AD apply only to business expenses. Taxpayers may still claim home loan interest (Section 24). Chapter VI‑A deductions: Section 80C, Section 80D, Section 80G, etc. These deductions are allowed from gross total income, not business income.

Key benefits of the presumptive taxation scheme u/s 44AD (FY 2025‑26) is no books of account required u/s 44AA, no tax audit u/s 44AB, and simple ITR 4 return filing. Predictable tax liability and reduced compliance cost, and it is ideal for micro and small enterprises. Presumptive Taxation Scheme Suitable for Retailers / Shopkeepers, Traders & Wholesalers, Small contractors and small businesses with simple operations and limited cash transactions

However, the decision to opt in should be based on actual profit margins, growth trajectory, loan / investment planning, and long term compliance strategy.

Advance Tax Requirement: Under presumptive taxation: Only one installment: 100% of tax liability must be paid on or before 15th March; however, late payment triggers interest u/s 234B & 234C.

Rule 5 Year Lock in Mechanism:

Once an assessee opts for Section 44AD: Once you opt for 44AD: You must continue for 5 consecutive years. The scheme must be followed for 5 consecutive assessment years.

If opted out during the 5 year period: if you opt out 5 years before taxpayers are barred from re-entering Section 44AD for the next 5 assessment years. You must maintain books & get an audit done if income exceeds the exemption limit. The assessee becomes ineligible to claim Section 44AD for the next 5 AYs. If total income exceeds the basic exemption limit. This prevents misuse of presumptive schemes.

Freelance Software Consultant. Freelance Software Consultant Can not opt for Section 44AD. Software consultancy is a specified profession u/s 44AA(1). The taxpayer must opt for Section 44ADA.

- Presumptive rate: 50% of gross receipts

- Limit: INR 50 lakh (INR 75 lakh if cash ≤ 5%)

- GST registration is not mandatory if the taxpayer opts for Section 44AD.

Income‑tax presumptive taxation has no direct link with GST registration. GST registration depends on INR 40 lakh (goods) or INR 20 lakh (services), subject to state‑specific rules. Taxpayers must ensure turnover figures match between GST and income tax to avoid scrutiny.