TDS on Payments to Non‑Residents w.e.f 1.04. 2026

TDS on Payments to Non‑Residents w.e.f 1.04. 2026, Structural Shift in Law: Replacement of Section 195, Tax deducted at Source Applicability Under the Income Tax ...

Read MoreTDS is among the tax collecting methods in which a individual making or crediting a charge to another needs to subtract a certain proportion of the value from that sum. TDS is like a cash tax charge to the state. It's in preparation. The sum of the TDS shall be paid by the Deductors to the Treasury. Account up until the 7th of the next month in which the balance is withdrawn. As the TDS is being paid by the Deductors to the Treasury. The Accountant shall ensure the daily inflow of cash capital to the State at appropriate intervals.

The Income Tax Act allows defined individuals to subtract tax for some forms of payments made by them. The list of these individuals needing the development of TDS is specified in the TDS section set out below. The following are the specified person who is liable to deduct TDS.

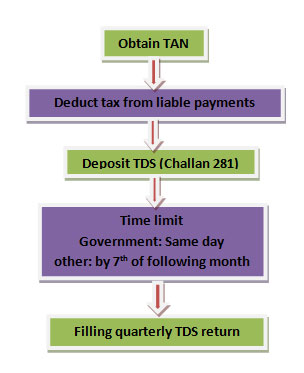

TAN is an alpha numeric 10 digits number. Every person who is accountable to deduct tax at source must obtain TAN no. from the department in form no. 49B within one month from end of the month in which tax was deducted. TAN is needed to be mention on every transaction related to TDS. There is a penalty of Rs. 10000 on failure to apply TAN

Procedure to pay TDS

Due Date of deposit of Challan 281 and filling quarterly return of TDS

Every person who is accountable to deduct TDS shall deposit the TDS deducted by him by 7th of following month in which TDS is deducted however Due date of deposit of TDS for the month of March is 30th April

The deadline of the quarterly TDS return is 15th of the next month in each year, although this deadline could be 15th in the case of the quarter ended March 20XX

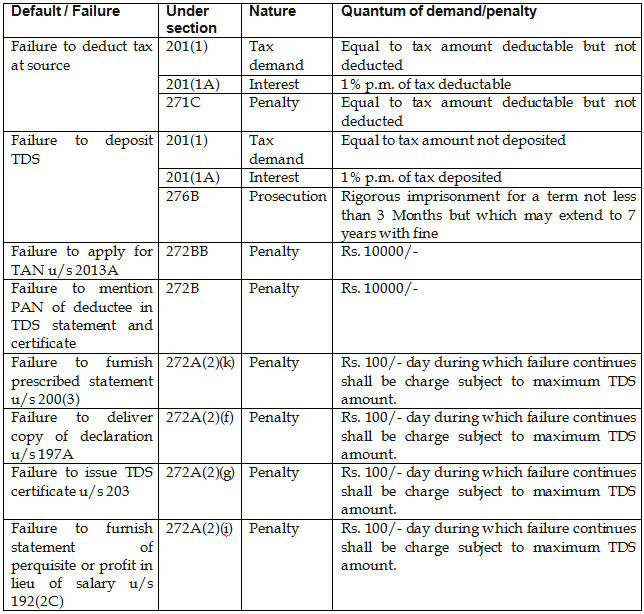

TDS Defaults

Penalties and interest in the event of non-filling / non-deduction and late deposit of the TDS sum.

Are you searching for TDS Specialists in Delhi capable of providing TDS return filling services; we provide TDS return filling services at an reasonable price that totally fulfill the customer's requirements and demands. Rajput Jain & Associates provide total Solutions under one roof regarding preparing of E-TDS Returns & Electronic Furnishing of TDS returns & relevant consultancy work to our clients. We provide the details of following services:

200+

550+

2009

700+

TDS on Payments to Non‑Residents w.e.f 1.04. 2026, Structural Shift in Law: Replacement of Section 195, Tax deducted at Source Applicability Under the Income Tax ...

Read More

Consolidation TDS provision, Rationalisation of TDS Provisions, Section 392 Applicable to income chargeable under head Salaries, Section 393 Applicable to non-salary payments, Structured u/s 393.Continuity of ...

Read More

Payments to Residents, New Section & Code Mapping for tds, Salary (Old Sec 192 → New Sec 392),Tax Collected at Source Section Codes (New), new deduction/collection codes & ...

Read MoreWe are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

All the information related to any client is considered confidential and never be disclosed to anyone.

Having years of experience in respective areas and backed by skilled and experienced workforce keep us ahead.

We believe in the building the good relationship with the clients that ensures the great impression.

If you are not happy with our services then you can request a refund within 30 days.

We provide 24*7 supports through phone, email and live chat.

You can pay online through EMIs, PayPal, net banking, debit card, credit card and more.

We are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

© 2016 Rajput Jain & Associates. All Rights Reserved | Sitemap