Table of Contents

Ease of Doing Business & Ease of Living through Union Budget 2026

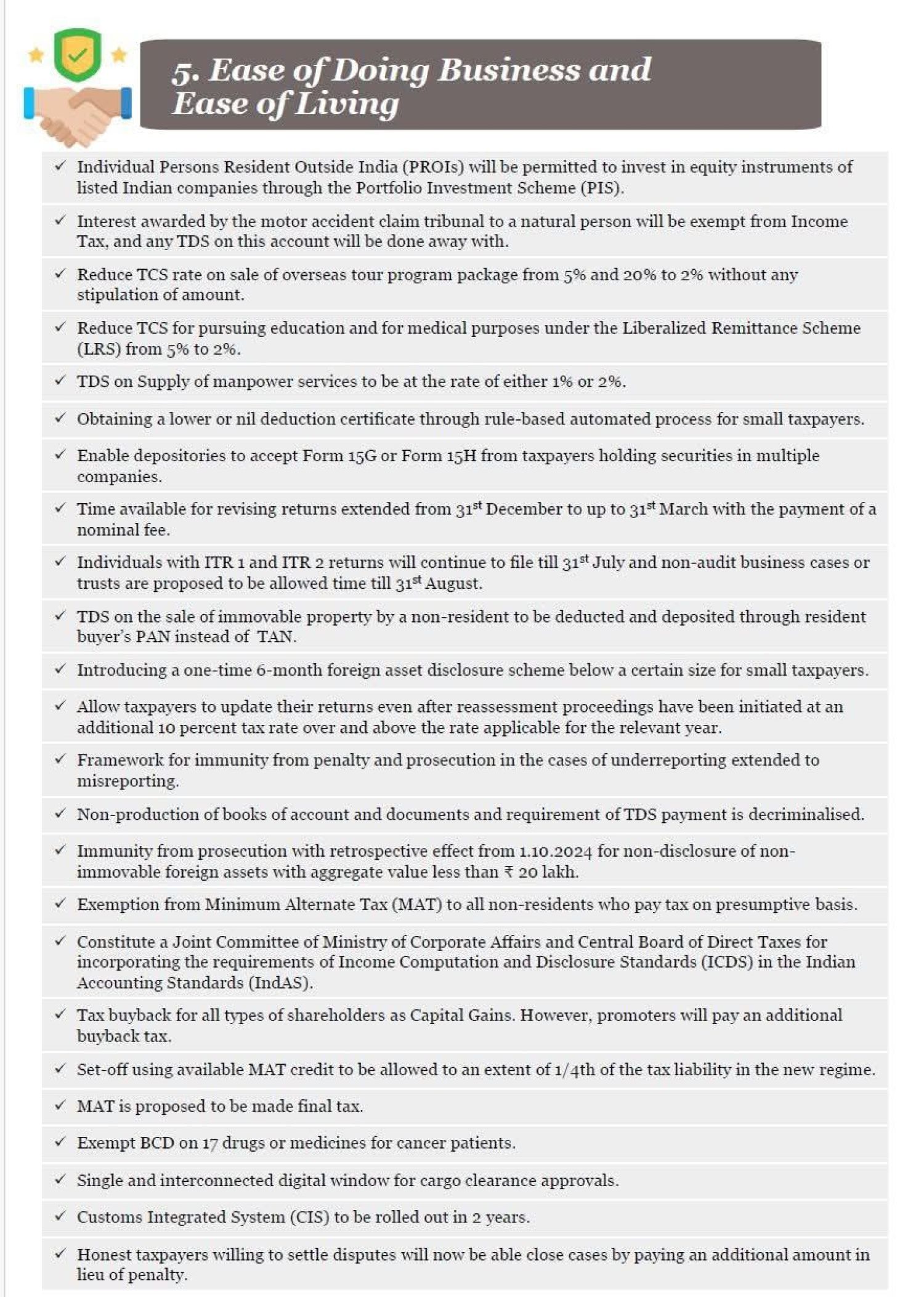

1. Reliefs & Rationalisation

Income tax

- Insurance compensation received by a natural person from a motor accident tribunal is fully exempt from income tax, and no TDS will apply.

- Due date for filing revised returns shifted from 31 December to 31 March (with a nominal fee).

- ITR‑1 & ITR‑2 filing due date remains 31 July for individuals; for business/non‑audit cases, proposed to be 31 August.

Tax Collected at Source / Tax Deducted at Source Changes

- Tax Collected at Source on foreign tour package: Reduced from 5% & 20% → flat 2%, without threshold.

- Tax Collected at Source under LRS for education & medical purposes: Reduced from 5% → 2%.

- Tax Deducted at Source on manpower services: Either 1% or 2%.

- Tax Deducted at Source on sale of Immovable Property to a Non-Resident: To be deducted using the buyer's PAN, not TAN.

2. Reforms for Small Taxpayers

- Lower/nil tax-deducted-at-source certificates to be automated via rule-based processing.

- One-time 6-month amnesty window for disclosure of income below a certain threshold.

- Taxpayers are allowed to rectify past returns even where assessment proceedings were already initiated, if additional 20% tax + interest is paid.

- Non-production of books/documents & non-reporting of Tax Deducted at Source payment made non-criminal, reducing prosecution risks.

3. Incentives for Non‑Residents / NRIs

- PROIs (Persons Resident Outside India) are allowed to invest in Indian equities via the Portfolio Investment Scheme (PIS).

- Exemption from Minimum Alternate Tax (MAT) for non-residents paying tax on a presumptive basis.

4. Capital Gains & Business Income

- A new capital gains regime:

All transfers of shares are taxed as capital gains only.

Promoters will pay additional buyback tax. - MAT regime revised: Certain units allowed to use existing MAT credit up to 1/4th of tax liability.

5. Corporate & Regulatory Compliance

- Depositories can accept Form 15G/15H from investors with multiple demat accounts.

- Finance Ministry + CBIC to develop Indian Accounting Standards (Ind AS) for taxation (ICDS overhaul).

- Quicker customs processes as CIS (Customs Integrated System) rolls out in 2026.

6. Exemptions & Sector-Specific Reliefs

- Immunity from prosecution for non-disclosure of certain non-immovable foreign assets for AYs 2010–2020.

- Digital visa & customs systems to ease compliance for travelers.

- Expenditure deductions expanded for cancer patients.

7. Dispute Resolution & Amnesty

- Honest taxpayers opting to settle disputes can close cases by paying an additional month of penalty, incentivizing faster resolution.

Draft Income-tax Rules, 2026

The Draft Income-tax Rules, 2026 introduce wide‑ranging adjustments aimed at aligning salary‑related exemptions, reporting requirements, and perquisite valuation norms with current economic realities. These proposals—while not reshaping the tax regime—represent a significant inflation‑linked correction, particularly beneficial for salaried employees in metro and high‑cost cities.

PAN Requirement — Wider Reporting Triggers

The draft rules propose making PAN compulsory for additional high‑value financial and lifestyle transactions. PAN would now be required where:

- Cash withdrawals or deposits exceed ₹10 lakh annually

- Vehicle purchases above ₹5 lakh

- Hotel/event expenditures above ₹1 lakh

- Insurance account opening, where specified

- Property transactions of ₹20 lakh or more

These measures extend the government’s reporting infrastructure to curb unreported transactions and enhance taxpayer traceability.

HRA—Broader "Metro" Classification

A major rationalisation is proposed in the HRA exemption, with expanded recognition of metro cities:

-

50% of salary: For accommodation in Mumbai, Kolkata, Delhi, Chennai, Hyderabad, Pune, Ahmedabad, Bengaluru

-

40% of salary: For all other locations

This acknowledges the fact that rent levels in cities like Hyderabad, Pune, Ahmedabad, and Bengaluru have long surpassed traditional Tier‑2 classification and now mirror metropolitan cost structures.

Residential Accommodation—Revised Perquisite Valuation

A. Employer-Owned Accommodation (Non-Government Employees)

|

City Population |

Proposed Perquisite Value |

|---|---|

|

Over 40 lakh |

10% of salary |

|

15–40 lakh |

7.5% of salary |

|

Below 15 lakh |

5% of salary |

B. Leased Accommodation

Perquisite = Lower of Actual lease rent paid by employer, or 10% of salary

C. Hotel Accommodation

Perquisite = Lower of Actual hotel charges, or 24% of salary (15‑day relief for transfers continues.)

D. Furnished Accommodation Add‑on: 10% p.a. of furniture cost, or Actual hire charges, where applicable

These changes simplify computation and introduce population‑based rationalisation.

Allowance Enhancements (Old Regime)—Long Overdue Updates

The draft rules significantly upgrade certain salary allowances to reflect contemporary expenses:

Children-related Allowances

| Allowance | Earlier | Proposed | Notes |

|---|---|---|---|

| Children Education Allowance | INR 100/month | INR 3,000/month | Max 2 children |

| Hostel Expenditure Allowance | INR 300/month | INR 9,000/month | Max 2 children |

Meals, Gifts & Transport

| Category | Earlier | Proposed | Notes |

|---|---|---|---|

| Free Meals | INR 50/meal | INR 200/meal | Via vouchers/canteen |

| Employer Gifts | INR 5,000/year | INR 15,000/year | Non-cash gifts |

| Transport Allowance—Divyang Employees | INR 3,200/month | INR 15,000 (Metro) / INR 8,000 (Non‑metro) | Large increase |

These revisions substantially increase the relevance and utility of the old tax regime for salary earners.

The Draft Income-tax Rules, 2026, represent an inflation‑adjustment exercise rather than a structural overhaul. Yet, their impact is meaningful. Families with school‑going children see major relief. Employees in urban and high-rent cities benefit through expanded metro classification for HRA., Rationalised perquisite valuation introduces greater clarity and fairness. and enhanced allowances make the old regime more competitive vis‑à‑vis the new regime. Overall, these draft rules materially improve the tax experience for the salaried class—especially in an era of rising cost of living.