Table of Contents

- Profiteering (incorrect – Profiteering) Under Gst Law (india)

- What Profiteering Means Under Gst:

- When A Business Fails To Reduce Mrp (incorrect – Profiteering) In Case Of Profiteering Under Gst:

- Why Prices Must Be Reduced After A Gst Rate Cut:

- Actions That Authorities Can Take In Case Of Profiteering Under Gst

- What Businesses Must Do To Comply Profiteering Under Gst:

- How Authorities Investigate Profiteering: Compliance Steps Shown For Profiteering Under Gst

- In Summary :

Profiteering (Incorrect – Profiteering) under GST Law (India)

What Profiteering Means under GST:

Profiteering under GST refers to a situation where a business does not pass on the benefit of a reduction in GST rates or input tax credit (ITC) to consumers by reducing prices. The objective of this rule is to ensure that tax benefits reach the final consumer rather than increasing the profit margin of suppliers. The anti-profiteering provisions are mainly contained in Central Goods and Services Tax Act, 2017, under Section 171, which mandates that any tax benefit must be passed on to customers through commensurate reduction in prices

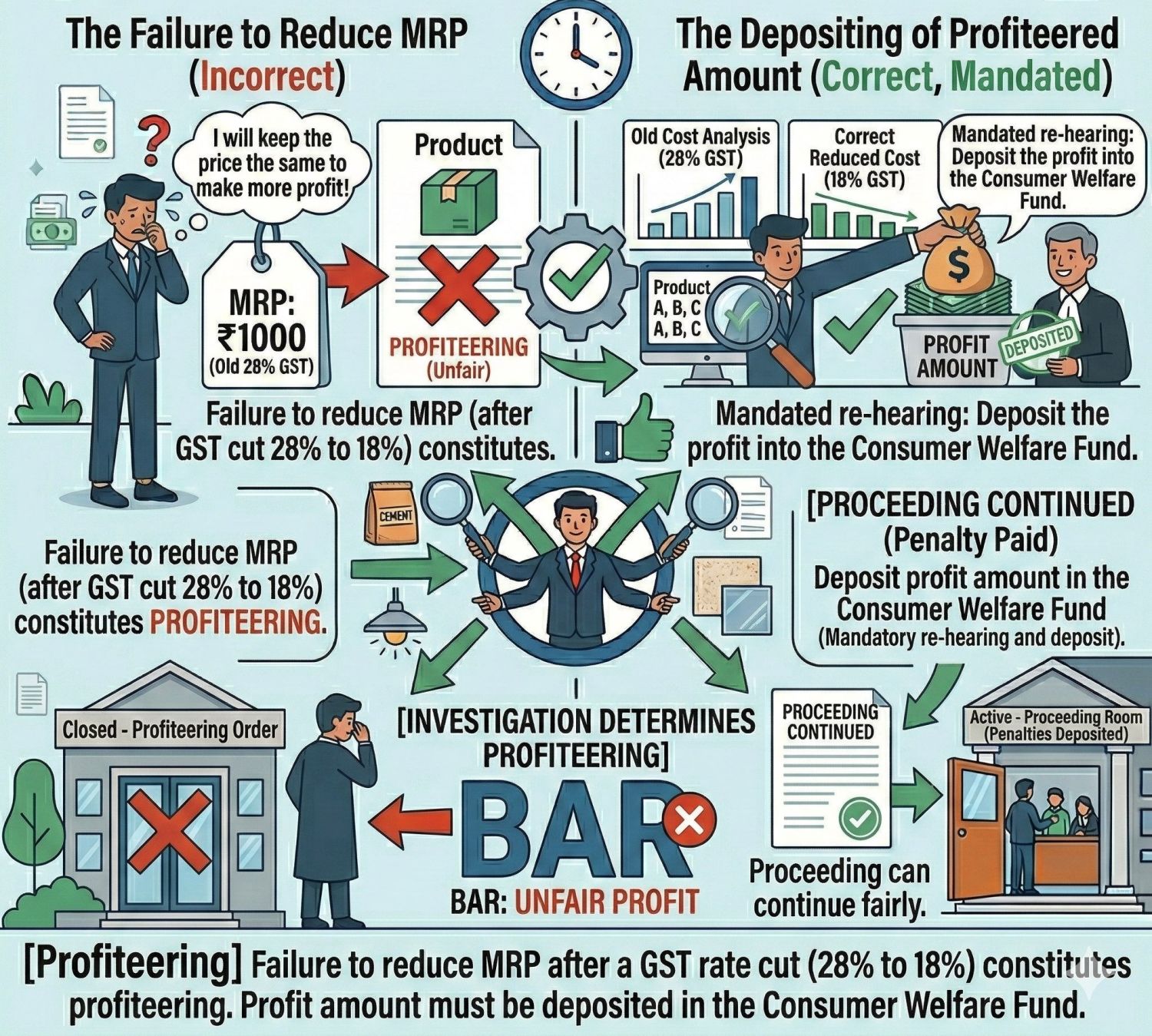

When a business fails to reduce MRP (Incorrect – Profiteering) in case of profiteering under GST:

Scenario A's product sells for INR 1000 when GST is 28%. The GST rate is reduced to 18%. But the business continues selling at INR 1000 instead of lowering the price. The tax burden has decreased, but the business keeps the extra margin. And this extra margin is treated as unfair profit or profiteering. Here, the supplier is retaining the tax benefit, which amounts to profiteering. Profiteering occurs when a supplier fails to reduce the price of goods or services after the GST rate is reduced or retains the benefit of additional input tax credit instead of passing it to consumers.

What Happens Next in case Profiteering Under GST: A formal investigation is launched. Authorities check whether the business actually gained extra profit. And If profiteering is confirmed A profiteering order may be issued. The business must deposit the extra profit into the Consumer Welfare Fund. And additional penalties or legal proceedings may follow.

Why Prices Must Be Reduced after a GST Rate Cut:

When the government reduces GST rates, businesses are required to pass on the benefit to customers by reducing the MRP. If they don’t, it is considered profiteering. The GST system aims to ensure that tax reductions benefit consumers directly. Key reasons:

- Consumer Protection: Tax reductions are intended to reduce the cost of goods and services for the public.

- Fair Market Practices: Businesses should not use tax rate changes to increase margins unfairly.

- Maintain Trust in the Tax System: Ensuring benefits reach consumers helps maintain the credibility of GST reforms.

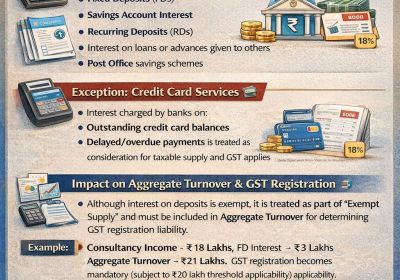

Actions that Authorities Can Take in case of Profiteering Under GST

Deposit the Profiteered Amount (Mandated by Law) : Correct Action for Profiteering Under GST If profiteering is established, authorities may order the business Reduce prices immediately, return the profiteered amount to consumers, and deposit the amount in the Consumer Welfare Fund if consumers cannot be identified. Pay interest on the profiteered amount. Pay penalties. And cancel GST registration in severe cases. In other words, If a business has wrongly earned extra profit due to not reducing MRP, it must Calculate the reduced cost after GST cut., Identify how much extra profit was made. And deposit that amount into the Consumer Welfare Fund.

What Businesses Must Do to Comply Profiteering Under GST:

To avoid anti-profiteering violations, businesses should follow these practices:

- Pass on Tax Benefits: Whenever GST rates are reduced or ITC increases, prices should be reduced proportionately.

- Maintain Documentation: Businesses should keep Cost sheets, pricing calculations, and Records showing benefit passed to customers

- Monitor GST Rate Changes: Businesses must regularly track notifications issued by the GST Council.

- Transparent Pricing: Price revisions should be clearly reflected in Invoices, Price lists, Product labeling

Practical Compliance Example: If the GST rate reduces from 18% to 12%, businesses should recalculate the base price, reduce the final selling price accordingly, and update invoices and billing systems. And maintain documentation proving benefits passed to consumers.

How Authorities Investigate Profiteering: Compliance Steps Shown for Profiteering Under GST

Proof of “Profit Amount Deposited." Mandatory rehearing before authorities. Proceedings continue until profit is deposited and any penalties (if applicable) are paid. This shows the business correcting the mistake and complying with GST law. Profiteering complaints are investigated through a structured mechanism.

Step 1: Complaint Filing: A complaint may be filed by Consumers, Government authorities, businesses, and Consumer welfare organizations

Step 2: Preliminary Examination: The complaint is first examined by the Standing Committee on Anti-Profiteering.

Step 3: Detailed Investigation: Officials conduct a cost and profit analysis. If unfair profit is identified It is marked as “Unfair Profit." Proceedings remain open until all profiteered amounts are deposited. And compliance requirements are fulfilled. If a business does not reduce MRP after a GST rate cut (such as from 28% to 18%), it is treated as profiteering. The extra profit must be deposited into the Consumer Welfare Fund. If prima facie evidence exists, the case is referred to the Directorate General of Anti-Profiteering for investigation. The investigation may include Examination of pricing data, Analysis of cost structures, Review of GST rate changes and Study of profit margins before and after rate reduction

Step 4: Decision by Authority: The final decision is taken by the National Anti‑Profiteering Authority (earlier framework), which determines whether profiteering has occurred.

In Summary :

Profiteering provisions under GST ensure that tax benefits are transferred to consumers rather than retained by businesses. The law promotes fair pricing, transparency, and consumer protection, while requiring businesses to maintain proper documentation and adjust prices whenever tax benefits arise. The cost reduces due to the lower GST rate. Taxpayer: Keeping the same MRP means the business earns extra margin (unfair profit). And This is classified as profiteering. Anti‑profiteering authorities perform a detailed cost and price analysis. If they confirm unfair profit It is treated as violating Section 171. The business must follow mandated corrective actions. methodology for determining profiteering varies case by case

Consequences

Authorities may initiate an investigation through anti‑profiteering mechanisms. (Standing Committee → DG Anti‑Profiteering → Authority. If guilty A Profiteering Order may be issued. The excess profit must be deposited in the Consumer Welfare Fund. Proceedings continue until the amount is deposited and penalties (if any) are paid. If GST is reduced (e.g., 28% → 18%), the price/MRP must be reduced proportionately. Otherwise, it is profiteering, and the extra profit must be deposited into the Consumer Welfare Fund.