Table of Contents

All about LUT Filing for FY 2026–27

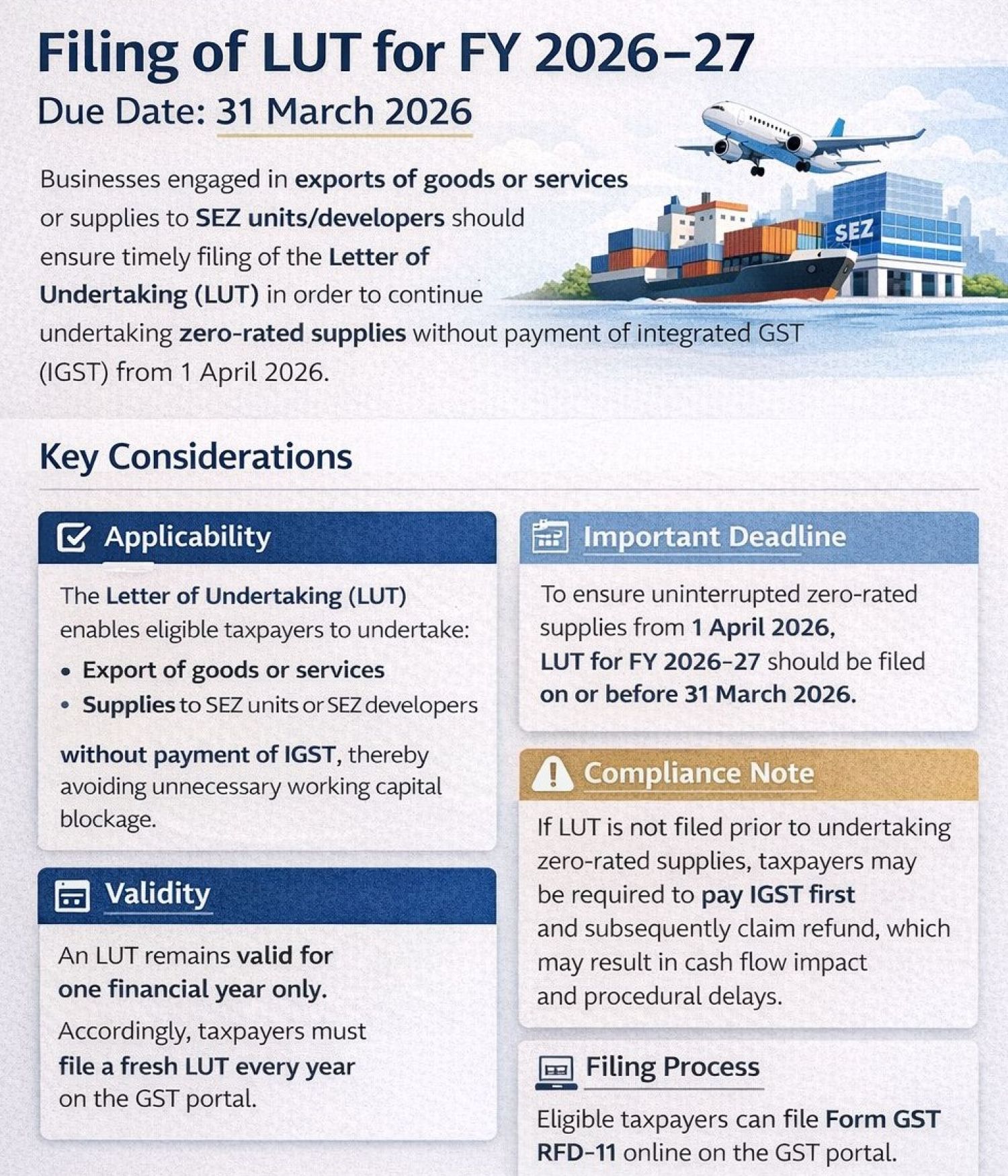

Letter of Undertaking Under GST: Under Section 16 of the IGST Act, 2017, exports and supplies to Special Economic Zones (SEZs) are treated as zero-rated supplies, meaning exporters should not bear the burden of domestic taxes. By furnishing Form GST RFD‑11, an exporter formally undertakes to export goods/services within the statutory time limits, comply with all GST provisions, and pay applicable IGST with interest if obligations are not fulfilled. The LUT is essentially a legal declaration enabling export without upfront IGST payment.

Why Is Letter of Undertaking Filing Critical for FY 2026–27?

As per Rule 96A of the CGST Rules, 2017, any person wishing to export without paying Integrated Goods and Services Tax must furnish an Letter of Undertaking before making exports or zero‑rated supplies to Special Economic Zones. Failing to file the Letter of Undertaking in time means GST taxpayer must pay Integrated Goods and Services Tax upfront on exports, Refund can only be claimed later through Form RFD‑01 and Refunds take weeks or months, locking up large working capital.

Impact Comparison

|

Parameter |

With Letter of Undertaking (RFD‑11) |

Without Letter of Undertaking (IGST + Refund Route) |

|

Upfront IGST Payment |

Not required |

Required |

|

Working Capital Impact |

None |

Funds blocked until refund |

|

Refund Process |

Not applicable |

RFD‑01 filing mandatory |

|

Processing Time |

Instant ARN |

2–6 months typically |

|

Paperwork |

Minimal |

Heavy documentation |

|

Best For |

Regular exporters |

Occasional exporters |

Who Must File Letter of Undertaking (Form GST RFD‑11)?

The Letter of Undertaking requirement applies to all GST‑registered persons engaged in zero‑rated supplies, including Exporters of physical goods, Suppliers to Special Economic Zones units/developers and Exporters of services (IT, consulting, design, freelancers, independent consultants)

Letter of Undertaking Filing Mechanism: Eligible taxpayers can file Form GST RFD-11 online through the GST Portal. GST portal Path: Login → Services → User Services → Furnish Letter of Undertaking.

The Letter of Undertaking process is entirely online. Physical submission is not required unless the officer seeks clarification (rare). There is no government fee. Any cost incurred is purely professional/consultant fees. filing is allowed after April 1. However, there is no retrospective protection. Any export invoice raised before Letter of Undertaking filing becomes taxable, and Integrated Goods and Services Tax and interest applies to those transactions.

Ineligible Category for Letter of Undertaking:

Only taxpayers prosecuted for tax evasion exceeding INR 2.5 crore under CGST/Integrated Goods and Services Tax are barred. They must file a bond with a bank guarantee instead. Exporters of goods must register under GST regardless of turnover (Section 24(i)). Service exporters with turnover below INR 20 lakh may be exempt from registration (Notification 10/2017‑IGST, dated 13-10-2017).

Consequences of Non‑Compliance of Letter of Undertaking:

Without an Letter of Undertaking, the customs/GST system treats the export as taxable. You must pay full Integrated Goods and Services Tax upfront, Cash flow gets immediately impacted, and delivery timelines and client commitments may suffer.

The GST portal does not auto-renew letters of undertaking if an exporter fails to export goods after filing an Letter of Undertaking. There is no penalty, but GST liability arises. If export obligations are not fulfilled within statutory timelines, you must pay integrated goods and Services Tax and interest (18% p.a.) and payable within 15 days of expiry of the time window. The Letter of Undertaking facility may also be temporarily withdrawn.

If a Letter of Undertaking is not filed before undertaking zero-rated supplies, the taxpayer may be required to pay Integrated Goods and Services Tax on export or SEZ supplies and claim a refund later from the GST Dept. This may lead to working capital blockage, delay in refund processing, and additional compliance burden.

Rule 96A –In case Letter of Undertaking Non‑Fulfilment Conditions

|

Condition |

Goods Export |

Services Export |

|

Time Limit |

Export within 3 months |

Realisation within 1 year |

|

Failure Consequence |

Integrated Goods and Services Tax and 18% interest payable |

IGST + 18% interest payable |

|

Payment Deadline |

Within 15 days after expiry |

Same |

|

LUT Facility |

Withdrawn until tax and interest paid |

Withdrawn |

A letter of undertaking cannot be applied retrospectively. Exports before Letter of Undertaking date = unavoidable IGST liability.

How to File GST LUT Online: Step-by-Step Guide

Step 1 — Log in: Visit gst.gov.in → Login with GSTIN credentials.

Step 2 — Navigate: Services → User Services → Furnish Letter of Undertaking.

Step 3 — Choose Financial Year: Select 2026–27 from the dropdown.

Step 4 — Fill Witness Details: Provide name, occupation, and address of two witnesses.

Step 5 — Self‑Declaration: Tick all mandatory declarations confirming that Export of goods within 3 months, Receipt of export proceeds within 1 year (for services), Compliance with GST laws and Agreement to pay IGST with interest if obligations are not met

Step 6 — Sign and Submit: Companies/LLPs: Sign using DSC and Proprietorships/ Partnerships: EVC (OTP)

Step 7 — Download Acknowledgement: Save the ARN and acknowledgment.

Post Submission Statuses: The exporter LUT may show Submitted, Pending for Clarification, Approved, Deemed Approved (no action in 3 working days), and Rejected. The status automatically becomes expired on 31st March 2027.

If exporting goods without filing the LUT for FY 2026–27 :

Exports will be treated as taxable, requiring upfront IGST payment. Refund can only be claimed later through RFD‑01, and interest may apply if Integrated Goods and Services Tax is not paid immediately. LUTs are valid for one financial year only and must be filed fresh every year.

LUT for FY 2026–27: Ensure Timely Filing to Continue Zero-Rated Supplies Without IGST

Businesses engaged in exports of goods or services or supplies to SEZ units/developers must ensure timely filing of the Letter of Undertaking to continue making zero-rated supplies without payment of Integrated Goods and Services Tax from 1 April 2026. U/s 16 of the Integrated Goods and Services Tax Act, exporters can supply goods or services without paying Integrated Goods and Services Tax by furnishing an Letter of Undertaking. A letter of Undertaking allows exports and SEZ supplies without payment of Integrated Goods and Services Tax, Letter of Undertaking is valid for one financial year only. A fresh Letter of Undertaking must be filed every financial year on the GST portal, and the Letter of Undertaking for FY 2026–27 should be filed on or before 31 March 2026. It is advisable to file Letter of Undertaking before 31 March 2026 to ensure uninterrupted exports from 1 April 2026 without payment of Integrated Goods and Services Tax.