Table of Contents

FAST DS, 2026 : Foreign Assets of Small Taxpayers (Disclosure Scheme 2026)

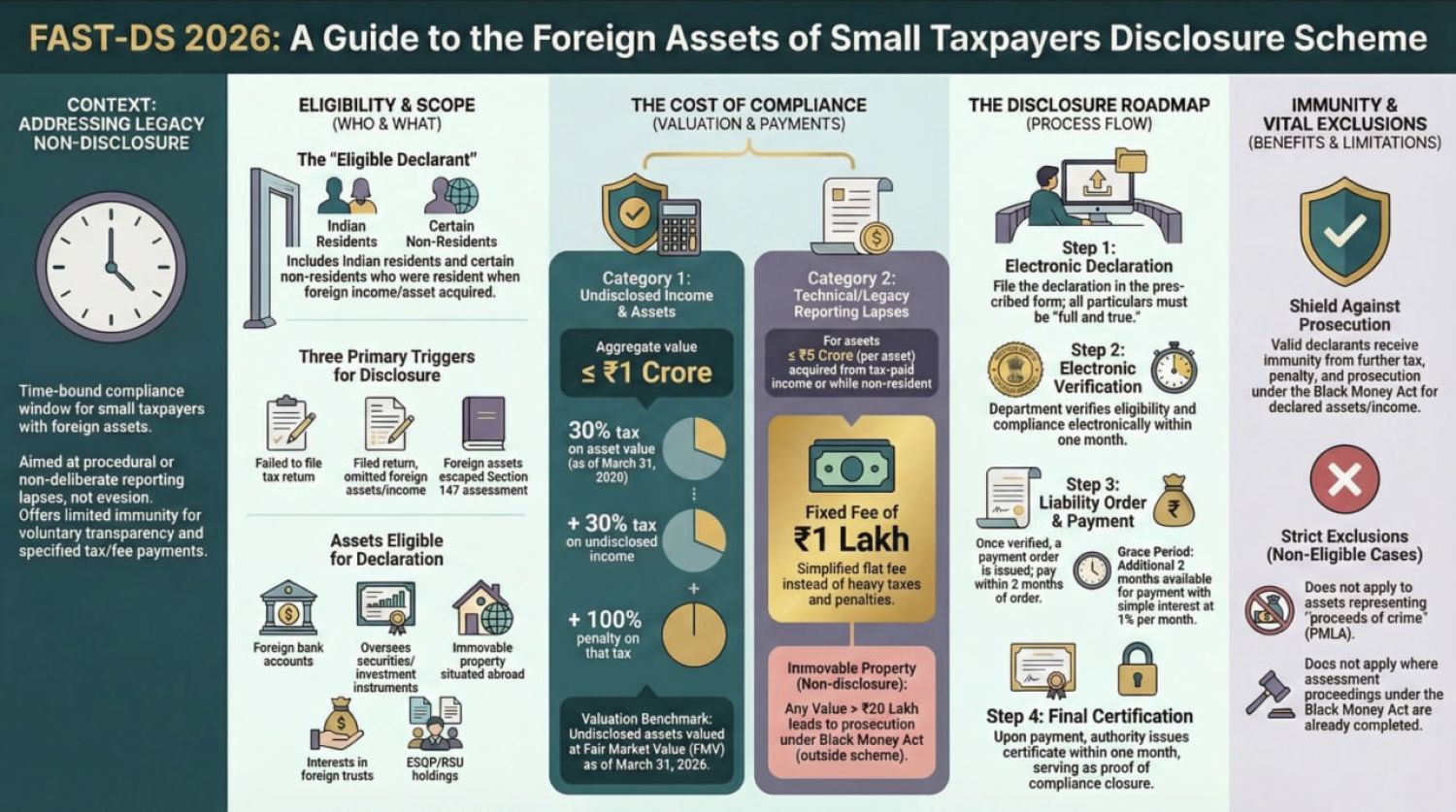

A one time compliance window under the Finance Bill, 2026. FAST DS (Foreign Assets of Small Taxpayers Disclosure Scheme), 2026, is a one‑time, six‑month voluntary disclosure window announced in the Union Budget 2026 and introduced through the Finance Bill, 2026. FAST DS 2026 is a special amnesty-style compliance window introduced under Chapter IV of the Finance Bill, 2026, to help small taxpayers rectify:

- Undisclosed foreign assets

- Undisclosed foreign income

- Missing Schedule FA disclosures

- Errors in Schedule FSI

- Old overseas assets of returning NRIs

- Unreported ESOPs/RSUs, foreign brokerage accounts, property, funds

In exchange for voluntary disclosure, the government grants immunity from prosecution, immunity from penalty, and no reassessment of earlier years for these assets. This is the safest legal route to clean up the past. FAST‑DS (Foreign Assets of Small Taxpayers – Disclosure Scheme), 2026 is designed to help small taxpayers voluntarily regularize:

- Foreign income or foreign assets that were never disclosed for Indian tax purposes, or

- Foreign assets that were reported incompletely (e.g., tax on income paid earlier, but asset not disclosed in Schedule FA), or

- Foreign financial interests that were erroneously or partially reported

It aims to provide a limited-period, low-friction route for taxpayers to come clean without facing the stringent consequences of the Black Money (Undisclosed Foreign Income and Assets) Act, 2015.

What Must Be Disclosed Under FAST DS 2026?

- Foreign Assets: Foreign bank accounts (including old/dormant), Overseas brokerage/custodial accounts, ESOPs, RSUs, stock options, Foreign shares & securities, Foreign mutual funds, ETFs and Overseas immovable property

- Foreign Income: Foreign interest, foreign dividends, capital gains on overseas shares/property, and any income arising from foreign assets. If it exists outside India, it must be disclosed.

Eligible Persons for FAST DS (Foreign Assets of Small Taxpayers Disclosure Scheme), 2026

The scheme is available to small taxpayers, specifically:

1. Individuals : Those who were resident in India at the time when the income accrued or the foreign asset was acquired.

2. Returning NRIs (RNORs/NRIs): Eligible only for assets acquired or income earned during a period when they were residents, even if they later became NRIs.

3. Small Taxpayers with Disclosure Gaps: Persons having Undisclosed foreign bank accounts, Small inherited foreign assets, Remittance‑linked holdings, Foreign stocks/ESOPs, and Foreign investment accounts. that were either never reported or reported incorrectly.

Two Categories of Disclosure & Financial Impact :

FAST‑DS distinguishes between truly undisclosed foreign income/assets and assets already taxed but not reported.

A. Category 1—Undisclosed Foreign Income or Assets

Applicability: Foreign assets/income that were neither disclosed nor taxed nor reported nor fully covered by the Black Money Act if discovered later. The monetary limit is the aggregate value capped at INR 1 crore (value as on 31 March 2026).

Tax & Levy:

|

Component |

Rate |

|---|---|

|

Basic Tax |

30% |

|

Additional Levy |

30% |

|

Total Outgo |

60% of the value |

Benefits:

-

Full immunity from penalty, prosecution, and further proceedings under the Black Money Act.

-

No reopening of earlier assessments for the disclosed foreign component.

B. Category 2—Income Tax Paid, but Asset Not Reported

Applicability: Cases where the foreign income was already included in taxable income, but the corresponding asset was not reported in Schedule FA or other reporting provisions. Common examples:

- ESOPs taxed as salary, but foreign accounts are not disclosed

- Foreign bank balance created from taxed income

- Foreign mutual funds purchased from disclosed income

Monetary Limit: Aggregate foreign asset value up to INR 5 crore (as on 31 March 2026).

Payment Requirement: Flat INR 1 lakh, regardless of asset value (subject to INR 5 crore cap).

Benefits:

- Immunity from penalties relating to foreign asset reporting failures

- No prosecution under the Black Money Act

- No penalty under income‑tax foreign asset disclosure rules (FA Schedule defaults)

Key Conditions of FAST DS 2026 To qualify successfully:

-

Eligibility must be strictly within thresholds: a INR 1 crore limit for undisclosed foreign assets and ₹5 crore limit for assets where tax was already paid

-

Declaration Must Be True, Correct & Complete: Partial disclosures or concealment void the immunity.

-

Payment Timeline: The amount determined by the authority must be paid within the prescribed time (likely within 30 days of order, subject to rules).

-

Immunity Is Limited: Protection applies only to the assets/income disclosed under the Black Money Act and certain Income Tax Act reporting defaults. It does not provide blanket protection for unrelated tax violations.

Mandatory ITR Reporting for Valid Disclosure

For the scheme to be considered valid, the taxpayer must file Schedule FA and Schedule FSI (if foreign income exists). Applicable ITRs are ITR-2 & ITR-3. Incorrect or incomplete schedules can invalidate immunity.

FAST‑DS Checklist for NRIs & Returning NRIs

NRI Before filing ITR, review all past ITRs, Check if Schedule FA was missed, Track foreign bank accounts (even dormant), Review ESOPs/RSUs, foreign shares, ETFs, Identify reporting lapses, Choose correct category (A or B) and Seek professional advice

Rule of Thumb for NRIs: If in doubt, disclose. Compliance under FAST‑DS is cheaper than prosecution under BMA. Moreover, in case an NRI is planning a move back to India, then use the DesiReturn Planner to sync tax compliance with visas, banking, NRE/NRO conversion, asset movement, and residency rules.

Special Relief for Minor & Inadvertent Non-Disclosures (INR 20 Lakh Rule)

The Finance Bill, 2026, provides relaxation in prosecution for small foreign assets (excluding property), aggregate value ≤ INR 20 lakh, and lapse was minor or unintentional lapse. It is useful for old salary accounts abroad, small foreign stocks/ETFs, and forgotten deposits. But immunity applies only if corrected now.

Summary of FAST DS, 2026

| Category | Applicability | Value Limit | Tax/Levy | Benefit |

|---|---|---|---|---|

| Category 1 | Undisclosed foreign income/assets | Up to INR 1 crore | 60% total (30% + 30%) | Full immunity under Black Money Act |

| Category 2 | Tax paid, but asset not reported | Up to INR 5 crore | Flat INR 1 lakh | Immunity from reporting penalties & prosecution |

90% of taxpayers are making a big mistake: an INR 10 LAKH penalty + 10 years jail risk. FAST DS 2026 Explained in Simple Words A shocking number of taxpayers, especially NRIs, returning NRIs, salaried individuals, investors, and freelancers, are unknowingly violating the Black Money Act every year. Not because of tax evasion. But because of non‑disclosure or incorrect reporting of foreign assets like

- Foreign bank accounts

- Overseas trading accounts (e.g., Interactive Brokers, TD Ameritrade)

- Foreign mutual funds & stocks (ESOP/RSU)

- Crypto exchanges outside India

- PayPal / Stripe / Wise balances

- Foreign property jointly held

- Dormant or small‑balance foreign accounts

Under the Black Money Act, 2015: Non disclosure can lead to an INR 10,00,000 penalty per year per asset, up to 10 YEARS of imprisonment, and prosecution even if income is small or tax is already paid. And most people don’t even know they’re supposed to report these assets every year in Schedule FA of the ITR.

FAST DS 2026: A One-Time Rescue Window

The government has launched the Foreign Assets of Small Taxpayers—Disclosure Scheme (FAST DS), 2026, to help small taxpayers fix past mistakes without fear of jail or heavy penalties. Two categories covered:

Undisclosed Foreign Income/Assets (Value ≤ INR 1 crore)

- 30% tax + 30% levy

- Effective 60% outgo

- Full immunity from the Black Money Act (penalty + prosecution)

Tax Paid but Asset Not Reported (Value ≤ INR 5 crore)

- Flat INR 1 lakh

- Immunity from reporting‑related penalties & prosecution

- Applicable in very common cases like ESOP taxed in India but asset not reported.

Foreign asset reporting is now the biggest tax risk for NRIs and returning Indians. Under the Black Money Act:

- Penalty = INR 10,00,000 per year per asset

- Jail = up to 7 years

- No time limitation

- Ignorance is NOT a defense.

This means even a dormant foreign bank account or old employer stock plan can trigger prosecution. FAST DS 2026 is effectively the last chance to fix past mistakes safely.