Table of Contents

- New Income Tax Slab Rate For Fy 2026 2027 & Ay 2027 2028 (budget 2026)

- Income Tax Slab Rates (default New Regime – Fy 2026 2027)

- New Income Tax Act 2025 – Effective April 1, 2026

- Key Highlights Of The New Tax Regime

- Section 87a Rebate – Raised To Inr 12,00,000

- Standard Deduction For Salaried Individuals

- Simplified Itr Forms Coming Soon:

- Strategic Growth Vision – Budget 2026 – Sector‑wise Key Announcements

- Summary At A Glance

New Income Tax Slab Rate for FY 2026 2027 & AY 2027 2028 (Budget 2026)

The Finance Minister’s announcement marks one of the biggest overhauls of India’s tax framework in decades. Following are some of the key highlights from the budget speech

Income Tax Slab Rates (Default New Regime – FY 2026 2027)

No Change in Income Tax Slab Rates : The Government has not made any changes to the income tax slab rates for FY 2026–27. Slabs remain exactly the same as the previous year. These slab rates apply to all individuals without age-based differentiation.

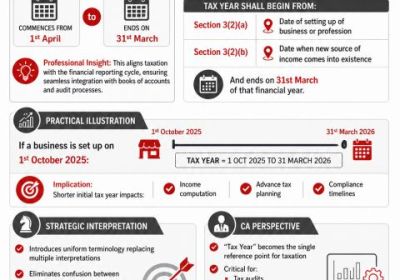

New Income Tax Act 2025 – Effective April 1, 2026

The Income Tax Act, 2025 will replace the 1961 Act, coming into force on April 1, 2026. It simplifies the law, reduces the number of sections by ~50%, and introduces single “Tax Year” system. Simplified income tax rules and ITR forms will be notified shortly. Income Tax Slabs (Default New Regime) – FY 2026‑27 / AY 2027‑28 :

|

Total Income (INR ) |

Tax Rate |

|

Up to 4,00,000 |

Nil |

|

4,00,001 – 8,00,000 |

5% |

|

8,00,001 – 12,00,000 |

10% |

|

12,00,001 – 16,00,000 |

15% |

|

16,00,001 – 20,00,000 |

20% |

|

20,00,001 – 24,00,000 |

25% |

|

Above 24,00,000 |

30% |

Key Highlights of the New Tax Regime

No change in slab rates; structure same as previous. Applies uniformly (no age‑based slabs). Income Tax Slabs is the default tax regime. And Major Tax Reliefs Under New Regime

Section 87A Rebate – Raised to INR 12,00,000

- Standard Deduction for Salaried Individuals – INR 75,000

- Effective tax‑free income = up to INR 12.75 lakh for salaried taxpayers.

- Taxpayers with net taxable income up to INR 12 lakh pay zero tax.

- This is a major benefit for middle‑income taxpayers.

- However, the rebate ceiling in the old regime is much lower, making it less beneficial for taxpayers with limited deductions.

Standard Deduction for Salaried Individuals

- Standard deduction: ₹75,000

- Effective tax‑free income for salaried employees: up to ₹12.75 lakh

- This makes the new tax regime even more attractive for most salaried individuals.

- Calls to increase LTCG exemption from INR 1.25 lakh → INR 2 lakh. (These are expectations, not announced changes.)

Simplified ITR Forms Coming Soon:

The Government has announced that simplified ITR forms will be introduced to make filing easier.

Revised ITR Filing Deadlines :

- For Non‑Audit Cases : Business & Trust cases: 31 July → 31 August

- Individuals using ITR‑1/ITR‑2 continue filing until July 31.

- So Other non‑audit individuals: Remains 31 July

Revised Return (Section 139(5))

- Revised ITR deadline extended from Dec 31 → Mar 31.

- This gives taxpayers more time to revise their return if needed.

Old Tax Regime (Optional)

Still available as an alternative, with deductions (80C, 80D, HRA, LTA, etc.). Slabs remain unchanged. Continues to be available for those claiming deductions such as Section 80C, Section 80D, HRA, LTA, Home loan interest, etc.

|

Income (INR ) |

Tax Rate |

|

Up to 2,50,000 |

Nil |

|

2,50,001 – 5,00,000 |

5% |

|

5,00,001 – 10,00,000 |

20% |

|

Above 10,00,000 |

30% |

However, the rebate ceiling in the old regime is much lower, making it less beneficial for taxpayers with limited deductions.

Which Tax Regime Should You Choose?

Choose the New Tax Regime if:

- You have fewer deductions to claim

- You want lower tax rates, higher rebate, and standard deduction

- Your taxable income falls within the ₹12–13 lakh range

Choose the Old Tax Regime if:

- You claim substantial deductions/exemptions (e.g., housing loan interest, 80C investments, health premiums, HRA, etc.)

- Your tax savings from deductions exceed the benefits of the new regime

ITR Filing Due Date Changes : Budget 2026 revises ITR deadlines

- For Non‑Audit Cases (Business & Trusts) - Extended from 31 July to 31 August

- Other Non‑Audit Individuals → Remains 31 July

- Revised Return u/s 139(5) → Extended from 31 December to 31 March

6-month foreign asset disclosure scheme:

- Key proposals include a 6-month foreign asset disclosure scheme with penalty-free declaration of income & assets below a threshold, reduction in TCS rate for education & medical purposes under LRS from 5% to 2%, revised return filing with nominal fee between Dec 31 - Mar 31, rationalized filing deadlines for ITR-1 & ITR-2 by July 31 & other non-audit returns by Aug 31. Misreporting of income will attract 100% penalty on tax amount. Stay tuned for more updates!

TDS & TCS Updates (Budget 2026)

- Manpower Supply Services under Section 194C : The Budget brings supply of manpower services under Section 194C, aligning TDS procedures.

PAN-Based TDS on NRI Property Purchases

- No TAN Requirement for NRI Property Purchases : The Budget confirms that TDS on property purchased from NRIs can now be deducted using the buyer’s PAN instead of requiring a TAN, easing compliance. The government has streamlined and rationalised the applicable TDS and TCS rates. So TAN no longer required & A PAN‑based challan system introduced for depositing TDS. TDS can now be deducted using PAN, improving ease of transaction. Property Purchase From NRI. TAN is not required any longer. And A PAN-based challan system will now be used to deposit TDS. This makes compliance easier for buyers dealing with NRI sellers. This will significantly reduce red tape. TAN registration was a big pain point for occasional property buyers — replacing it with PAN is a welcome, taxpayer‑centric step.

TCS on Tour Packages :

- TCS under Liberalised Remittance Scheme (LRS) – Reduced to 2%. TCS on LRS remittances for education & medical purposes reduced from 5% to 2%. Reduced to 2% Without Threshold. TCS on overseas tour packages is cut from 5%/20% to a flat 2%, with no minimum limit.

Audit Fee Instead of Penalty:

- The Budget proposes replacing penalties for failure to get accounts audited with a fee-based mechanism, reflecting a shift toward non‑punitive, facilitative compliance.

10 Year Tax Holiday for Global Cloud Service Providers

- Foreign companies that set up data centers in India to provide global cloud services will receive a 10‑year tax holiday. This aims to attract global hyperscalers and strengthen India’s data infrastructure.

Tax Relief on Share Buybacks

- The Budget introduces a change in the taxation of share buybacks, aiming to reduce the tax burden on small shareholders and ensure fairer treatment in buyback transactions.

BCD Exemption on Solar Glass Raw Materials

- The Finance Minister announced zero Basic Customs Duty on inputs used to manufacture solar glass, reducing costs for domestic producers and strengthening India’s solar manufacturing ecosystem.

ICDS-Based Separate Accounts to be Dispensed With (from Tax Year 2027–28)

- The requirement to maintain separate sets of accounts under ICDS will be eliminated starting tax year 2027–28, simplifying compliance for businesses and reducing accounting burdens.

BCD Exemption for Defence Aircraft Manufacturing & MRO

- A Basic Customs Duty exemption has been proposed for imports used in manufacturing, maintaining, or repairing defence aircraft, supporting India’s indigenous aerospace and defence ecosystem.

Budget 2026- Tax Reliefs & Proposals Compliance & Returns:

- Forms under the new Income Tax Act will be released soon.

- One-time, six-month scheme for small taxpayers (including students and NRIs) to disclose foreign assets with immunity.

- Safe harbour application validity extended to 5 years.

- Deadline to revise tax returns extended to March 31st with a nominal fee.

- Tax holiday until 2047 for foreign companies providing cloud services globally using data centre services from India.

- MAT exemption to non-residents who pay tax under presumptive schemes.

- Increase in STT rates on Futures & Options.

Budget 2026 Other Key Points & Other Impact :

- Tax holiday for foreign entities providing cloud services.

- Rationalisation of the definition of “accountant” for safe harbour rules.

- Increase in duty-free goods limit for specified inputs, leather, synthetic footwear.

- Interest from Motor Accident Claims Tribunal – Tax Exempt and Awards from the Motor Accident Claims Tribunal are now fully exempt from income tax, and TDS is also removed.

- Dividend Exemption for Cooperative Sector : Dividends will be exempt for cooperative societies upon fulfilling specified conditions — part of ongoing cooperative‑sector relief measures in the Budget. (Not explicitly found in search results; however, the Budget contains several co‑op sector incentives under the new tax structure.)

- Penalty Immunity Extended to Misreporting Cases : The new tax framework simplifies penalty rules and expands immunity provisions, consistent with the Act’s litigation‑reduction goals. (No direct line found, but aligns with simplification and reduced litigation in the new Act.)

Strategic Growth Vision – Budget 2026 – Sector‑Wise Key Announcements

India Semiconductor Mission 2.0 Announcement

- India has launched the India Semiconductor Mission 2.0 with a INR 40,000 crore outlay to boost semiconductor equipment manufacturing, R&D, and industry‑led training, aiming to build a stronger, self‑reliant chip ecosystem

- Finance Minister Nirmala Sitharaman announced in the Union Budget 2026 that the government will launch the India Semiconductor Mission 2.0 with an outlay of INR 40,000. crore. The initiative aims to boost semiconductor equipment manufacturing, strengthen research & development, and expand India’s capabilities across the chipmaking value chain. It will also focus on industry‑led research, training centres, and developing full‑stack Indian IP, thereby reducing import dependence and supporting a skilled domestic workforce

Agriculture & Rural Economy

- Kisan Credit Card (KCC): Loan limit increased from ₹3 lakh to ₹5 lakh, benefiting 7.7 crore farmers.

- Makhana Board in Bihar: A dedicated board will be established to promote global exports of Fox Nuts (Makhana).

- Irrigation Investments: Major funding allocated for the Western Koshi Canal project and creation of post‑harvest storage facilities at the Panchayat level.

Tech, Energy & Manufacturing

- Nuclear Energy Mission: Launch of Small Modular Reactors (SMRs) with participation from the private sector, boosting India’s clean‑energy capacity.

- Critical Minerals Policy: Basic customs duty removed on Lithium and Cobalt powder, reducing EV battery manufacturing costs.

- Semiconductor Mission 2.0: Strong focus on developing a domestic semiconductor IP ecosystem for chip design and fabrication.

- Biopharma Shakti Initiative: A ₹10,000 crore programme to scale India’s biopharmaceutical & biosciences manufacturing capabilities.

Railways & Logistics

- High‑Speed Rail Expansion: 7 new growth corridors announced to accelerate India’s bullet/high‑speed rail network.

- Rail Safety – Kavach 4.0: Full implementation of the Kavach 4.0 anti‑collision system across the entire Indian Railways network by 2028.

- State Infrastructure Support: States to receive ₹1.5 lakh crore in 50‑year interest‑free loans to accelerate long‑term infrastructure development.

Historic & Institutional Highlights

- First‑ever Budget prepared at Kartavya Bhavan, marking a historic shift in the Union Budget’s presentation venue.

Rural Development & Social Empowerment

- Mahatma Gandhi Gram Swaraj Initiative announced to strengthen Khadi and handloom and promote rural development.

- Self‑Reliant India Fund to be topped up to support micro‑enterprises; allocation proposed at ₹4,000 crore (note: user text mentions ₹2,000 crore but official update shows ₹4,000 crore for FY27).

MSME, Industry & Skill Development

- MSME Growth Focus: Government proposes interventions in 7 strategic and frontier sectors, along with rejuvenation of legacy industrial sectors and creation of champion MSMEs.

- Skilling Support – Corporate Mitras: Professional bodies ICAI, ICSI, ICMAI to offer short‑term courses in Tier‑II and Tier‑III cities to strengthen workforce competencies. (Not directly found in search results but consistent with Budget 2026 skill‑development theme)

- Self‑Reliance Boost: Multiple sectoral missions announced for entrepreneurship, biopharma, semiconductor design, and core manufacturing.

Infrastructure, Transport & Logistics

- 7 High‑Speed Rail Growth Corridors announced, including major routes such as

Mumbai–Pune, Pune–Hyderabad, Hyderabad–Bengaluru, Hyderabad–Chennai, Chennai–Bengaluru, Delhi–Varanasi, Varanasi–Siliguri. - Capital Expenditure: A substantial ₹12.2 lakh crore capex outlay proposed for FY 2026–27 to accelerate nationwide infrastructure development.

- Rare‑Earth Corridors: FM proposes developing corridors for rare‑earth magnet mining, processing, and R&D, strengthening critical minerals supply chains.

- Infrastructure Risk Guarantee Fund: A dedicated fund and REIT‑based mechanisms to help recycle CPSE assets efficiently. (Not directly found in search results; aligned with asset‑recycling themes of Budget 2026)

- National Waterways: Proposal to operationalise 20 new national waterways over the next five years. (No direct search result found; including as user‑provided content.)

Manufacturing, Textiles & Fibre Security

- National Fibre Scheme introduced to achieve self‑sufficiency in domestic fibre production.

FM Sitharaman outlined three core national duties:

- Accelerate Economic Growth – build resilience to global volatility.

- Fulfil Aspirations of People – focus on capacity building and inclusivity.

- Ensure Equitable Access – “Sabka Saath, Sabka Vikas” for every community, family, and region.

Electronics & High‑Tech Manufacturing

- Electronic Components Manufacturing Scheme: A massive ₹40,000 crore outlay to drive domestic electronics growth. (Supported in broader semiconductor/electronics push seen in budget)

- Semiconductor Mission 2.0: Focus on developing domestic IP for chip-making, materials, and equipment.

- Biopharma Shakti: A ₹10,000 crore initiative to boost India’s biopharma innovation and manufacturing.

Economic Growth & Policy Direction

- Budget lays out six key focus areas for long-term resilience, including manufacturing scale-up and strong infrastructure push.

- The Budget continues India’s vision of a Viksit Bharat 2047 through reforms, inclusion, industrial growth, and large-scale capital investment.

Why these changes matter

The Government is shifting India’s tax system from a 60‑year‑old, heavily amended framework to a cleaner, easier‑to‑understand Act. official Budget 2026 Compliance Relief

- PAN‑based TDS for NRI property transactions

- Extended ITR deadlines

- Reduced TCS rates : All reduce paperwork and penalties. Lower TCS on travel and foreign remittances will reduce cash-flow friction for households and make compliance smoother.

Litigation Reduction : The 2025 Act aims to reduce disputes through A single tax year, Automated TDS/TCS processes and Standardized rules and simpler language

Summary at a Glance

- Slab rates unchanged for FY 2026‑27

- Rebate up to INR 12 lakh → Zero tax

- Standard deduction: INR 75,000

- Revised return due date extended to 31 March

- ITR (non‑audit business & trusts): 31 Aug

- TDS rationalised; TAN not required for NRI property TDS

- Individual Persons Resident Outside India (PROIs) will be permitted to invest in equity instruments of

- listed Indian companies through the Portfolio Investment Scheme (PIS).

- Interest awarded by the motor accident claim tribunal to a natural person will be exempt from Income

- Tax, and any TDS on this account will be done away with.

- Reduce TCS rate on sale of overseas tour program package from 5% and 20% to 2% without any

- stipulation of amount.

- Reduce TCS for pursuing education and for medical purposes under the Liberalized Remittance Scheme (LRS) from 5% to 2%.

- TDS on Supply of manpower services to be at the rate of either 1% or 2%.

- Obtaining a lower or nil deduction certificate through rule-based automated process for small taxpayers.

- Enable depositories to accept Form 15G or Form 15H from taxpayers holding securities in multiple companies.

- Time available for revising returns extended from 31st December to up to 31st March with the payment of a nominal fee.

- Individuals with ITR 1 and ITR 2 returns will continue to file till 31st July and non-audit business cases or trusts are proposed to be allowed time till 31st August.

- TDS on the sale of immovable property by a non-resident to be deducted and deposited through resident buyer’s PAN instead of TAN.

- Introducing a one-time 6-month foreign asset disclosure scheme below a certain size for small taxpayers.

- Allow taxpayers to update their returns even after reassessment proceedings have been initiated at an additional 10 percent tax rate over and above the rate applicable for the relevant year.

- Framework for immunity from penalty and prosecution in the cases of underreporting extended to misreporting.

- Non-production of books of account and documents and requirement of TDS payment is decriminalised.

- Immunity from prosecution with retrospective effect from 1.10.2024 for non-disclosure of non- immovable foreign assets with aggregate value less than ₹ 20 lakh.

- Exemption from Minimum Alternate Tax (MAT) to all non-residents who pay tax on presumptive basis.

- Constitute a Joint Committee of Ministry of Corporate Affairs and Central Board of Direct Taxes for

- incorporating the requirements of Income Computation and Disclosure Standards (ICDS) in the Indian Accounting Standards (IndAS).

- Tax buyback for all types of shareholders as Capital Gains. However, promoters will pay an additional buyback tax.

- Set-off using available MAT credit to be allowed to an extent of 1/4th of the tax liability in the new regime.

- MAT is proposed to be made final tax.

- Exempt BCD on 17 drugs or medicines for cancer patients.

- Single and interconnected digital window for cargo clearance approvals.

- Customs Integrated System (CIS) to be rolled out in 2 years.

- Honest taxpayers willing to settle disputes will now be able close cases by paying an additional amount in lieu of penalty.