Table of Contents

GST Year-End Compliance Summary (FY 2025-26 & Start of FY 2026-27)

As the financial year 2025-26 comes to an end and FY 2026-27 begins, businesses must review several GST compliance requirements, reconciliations, and regulatory decisions. This period is crucial for closing books properly, avoiding tax disputes, and preparing for new compliance obligations such as e-invoicing and input service distributor (ISD) provisions. The key areas of compliance can be divided into four major categories: pre-year-end compliances (before 31 March 2026), beginning of new financial year compliances, year-end reconciliations and ITC checks, and regulatory checks and risk management. The end of the financial year is a critical compliance period under the GST regime. Businesses must review filings, eligibility conditions, and ITC claims to avoid penalties, interest, or credit reversals under the Central Goods and Services Tax Act, 2017. Below is a structured compliance roadmap from March 2026 to November 2026.

- Critical Actions Before 31 March 2026: A. LUT Filing for Exporters: Exporters supplying goods/services without payment of IGST must file Form GST RFD‑11 (Letter of Undertaking). Deadline: 31 March 2026 Purpose: To enable zero-rated exports without IGST payment and required for exports and SEZ supplies.

- Composition Scheme Option: Small taxpayers may opt for the composition scheme by filing Form GST CMP‑02. Deadline: 31 March 2026. If switching from regular scheme ITC must be reversed through Form GST ITC‑03 and Deadline: 30 May 2026

- Reset Invoice Number Series: Every GST-registered business must start a new invoice series from 1 April. Key requirements Unique invoice numbers, sequential numbering, and separate series allowed for branches or business verticals

- Recalculate Aggregate Turnover: Businesses must compute aggregate turnover for FY 2025-26 to determine eligibility for the e-invoicing threshold (INR 5 crore), the QRMP scheme, and the cash payment rule under Rule 86B of CGST Rules.

Key Changes from 1 April 2026: Key Focus Areas for Businesses

- Mandatory E-Invoicing: Businesses with turnover exceeding ₹5 crore in FY 2025-26 must generate e-invoices through the Goods and Services Tax Network portal. Effective date: 1 April 2026. Failure may lead to invalid invoices, ITC denial to customers, and penalties.

- ISD Registration Requirement: Entities operating with multiple GST registrations must obtain Input Service Distributor (ISD) registration to distribute common input tax credits. Effective implementation began from 1 April 2025.

- Job Work Reporting: Businesses sending goods to job workers must file Form GST ITC‑04. Deadline: 25 April 2026 The purpose is to track goods sent/received for job work and ensure compliance with job-work provisions.

- QRMP Scheme Option: Taxpayers with turnover up to ₹5 crore can opt into the Quarterly Return Monthly Payment (QRMP) Scheme. Opt-in/Opt-out deadline: 30 April 2026

May – June 2026 Compliance

- ITC-03 for Composition Switch: Taxpayers shifting to the composition scheme must reverse the input tax credit on closing stock. From: GST ITC-03 Deadline: 30 May 2026

- Real Estate Sector – 80% Procurement Rule: Developers must ensure 80% of purchases are from registered suppliers. If a shortfall occurs, the Reverse Charge Mechanism (RCM) applies, and additional RCM applies to cement purchases. Compliance deadline: 30 June 2026

September – November 2026: Supplier Filing Monitoring

- ITC Reversal under Rule 37A: Under Rule 37A of CGST Rules: if the supplier does not file GSTR-3B, ITC must be reversed by the recipient. Condition: The supplier fails to file GSTR-3B for FY 2025-26 by 30 September 2026: Then the recipient must reverse ITC by 30 November 2026.

- Reclaim of ITC: Once the supplier files GSTR-3B, the recipient can re-avail the reversed ITC.

Ongoing Compliance Checks - Key Focus Areas for Businesses

- Outward Supply Reconciliation: Businesses must reconcile books vs. GSTR-1, GSTR-1 vs GSTR-3B, Stock movement vs. invoices, and advances vs. tax liability

- Inward Supply Reconciliation: Review books vs. GSTR-2B, Vendor compliance, Ineligible ITC reversals and Pending vendor payments

- 180-Day Payment Rule: Under Rule 37 of CGST Rules, ITC must be reversed if vendor invoices remain unpaid for more than 180 days. ITC can be reclaimed after payment is made.

- Supplier E-Invoicing Validation: Recipients should verify that suppliers required to issue e-invoices actually generate them. Otherwise, the invoice may become invalid, and ITC may be blocked.

- Rule 86B – Cash Payment Requirement: Businesses may need to pay at least 1% of GST liability in cash if taxable turnover exceeds prescribed thresholds under Rule 86B.

- GST Refund Compliance: Before applying for refunds Update bank account details, complete Aadhaar authentication, and ensure export documentation is complete.

- Litigation Monitoring: Businesses should regularly track Show Cause Notices, Adjudication proceedings, and Appeals, and voluntary tax payments can be made through Form GST DRC‑03A.

- Zero-Rated Supply Documentation: For exporters Maintain SEZ endorsement copies and ensure foreign remittance within the FEMA timeline (9 months). Failure may lead to refund recovery with interest.

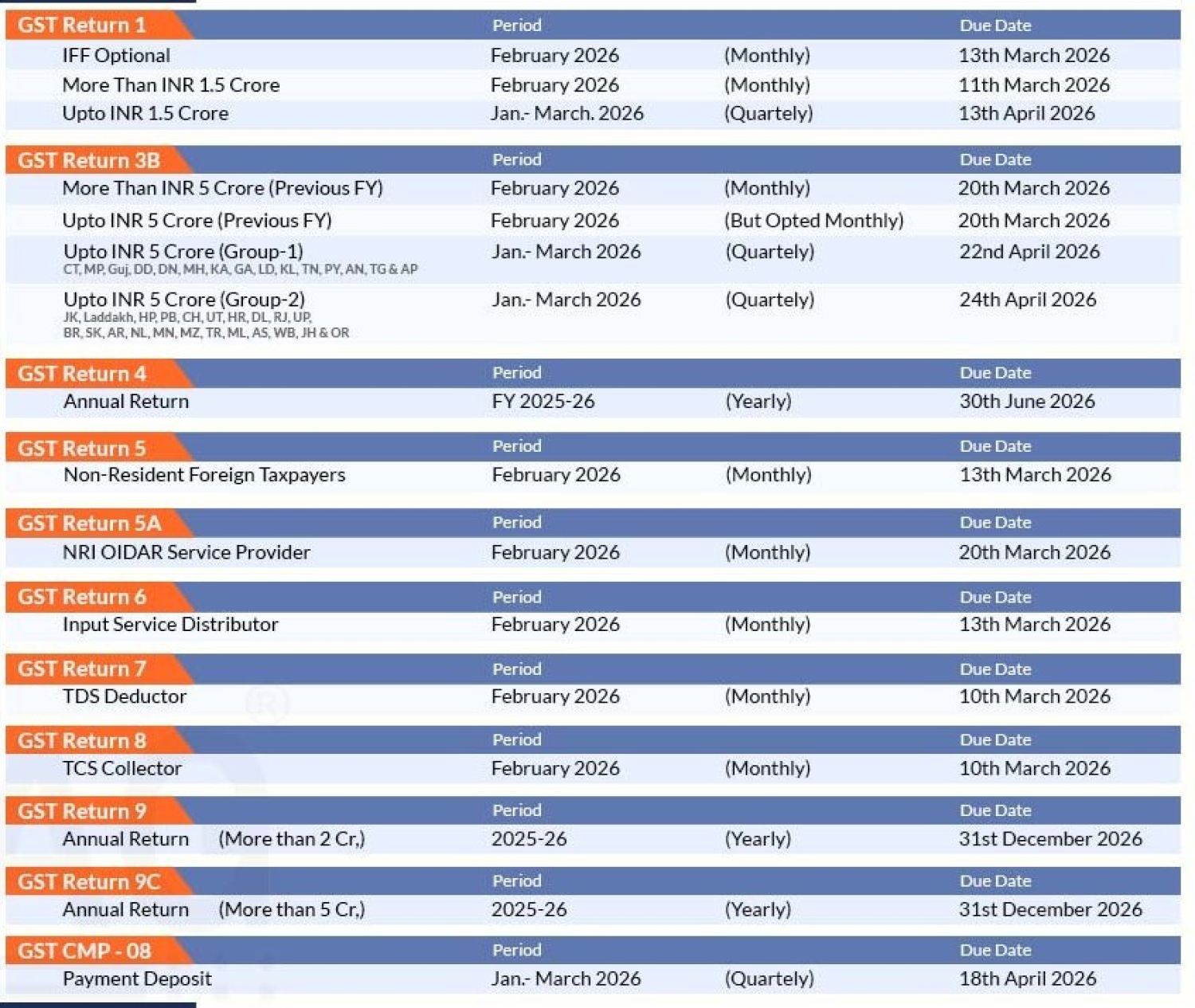

Quick Compliance Calendar Key Focus Areas for Businesses

GST year-end compliance requires systematic reconciliation, timely filings, and supplier monitoring. Businesses that proactively review turnover thresholds, ITC eligibility, vendor compliance, and export documentation can avoid interest, penalties, and ITC reversals while ensuring a smooth transition into FY 2026-27.

March 2026 :

- 31 March: Before 31 March 2026: LUT filing, composition scheme option, invoice series reset, and turnover calculation. Composition scheme decision, Invoice number reset and Turnover calculation

April 2026

- 1 April: E-invoicing mandatory (> INR 5 crore turnover), ISD registration applicable. E-invoice readiness, ITC-04 filing, QRMP scheme decision.

- 25 April – ITC-04 filing

- 30 April – QRMP opt-in/out

May 2026 :

- 30 May – ITC-03 for composition switch

June 2026 :

- 30 June – Real estate 80% procurement compliance

- June 2026: Real estate RCM compliance

September 2026 :

- 30 September – Supplier GSTR-3B deadline (important for Rule 37A)

November 2026 :

- 30 November – ITC reversal if supplier fails to file GSTR-3B.

- September – November 2026: Monitor supplier filings and Reverse ITC under Rule 37A if required

Beginning of FY 2026 2027 Compliance

- E-Invoicing Applicability : Businesses whose PAN-based aggregate turnover exceeds ₹5 crore must generate e-invoices. Effective from: 1 April 2026. Steps required Register on the Invoice Registration Portal (IRP), Generate Invoice Reference Number (IRN) and Include QR code on invoices. Failure consequences Invoice becomes invalid and Recipient cannot claim ITC

- Mandatory Input Service Distributor (ISD) : After the Finance Act 2024 amendment, offices receiving invoices for common services for multiple GST registrations must register as ISD. Effective: 1 April 2025. Purpose is Proper distribution of ITC across multiple GSTINs, Replace misuse of cross-charge mechanisms.

- Year-End Reconciliation Requirements: Proper reconciliation helps prevent notices, tax demands, and ITC reversals. Outward Supply Reconciliation Businesses should compare: Turnover as per books vs GSTR-1 vs GSTR-3B. E-way bills vs tax invoices, E-invoices vs IRN generated, and Advances received vs adjusted invoices

- Other checks like Correct HSN/SAC codes, Correct GST rates and Adjustment of advance tax on services

- Inward Supply Reconciliation : Key ITC checks include Books vs Electronic Credit Ledger, Books vs GSTR-2B, ITC blocked under Section 17(5) and Supplier filing status of GSTR-3B. Businesses must also identify Unclaimed ITC, ITC wrongly claimed, and ITC pending due to supplier non-compliance.

- ITC Reversal Rules : Rule 37 – Non-Payment to Vendors, If payment to supplier is not made within 180 days from invoice date ITC must be reversed and Interest must be paid from the date of availing ITC. However, ITC can be reclaimed once payment is made.

- Rule 37A – Supplier Non-Filing of GSTR-3B : If supplier fails to file GSTR-3B for FY 2025-26 by 30 September 2026. Recipient must reverse ITC by 30 November 2026. But ITC can be reclaimed later once supplier files the return.

- Special Compliance Areas: Real Estate – 80% Procurement Rule. Developers must procure at least 80% of inputs from registered suppliers. If not GST must be paid under Reverse Charge Mechanism (RCM) on the shortfall. Additional rule Cement purchased from unregistered suppliers attracts 28% GST under RCM. Deadline: 30 June 2026

- Export Proceeds Realisation under FEMA : Export proceeds must be received within 9 months. If refund was claimed but payment is not received Refund must be returned with interest within 30 days. If payment is received later Refund can be claimed again.

- E-Invoice Status of Vendors: Businesses should verify if suppliers are required to issue e-invoices. If supplier should issue e-invoice but does not Invoice become invalid and ITC may be denied to the recipient

- Rule 86B 1% Cash Payment Rule: Businesses must pay at least 1% of GST liability in cash if Monthly taxable supply exceeds INR 50 lakh. Exceptions is Income tax paid > INR 1 lakh in last 2 years, Refund received > INR 1 lakh and Government entities.

- GST Litigation and Risk Management: Businesses should review Pending Notices Examples: ASMT-10 , Show Cause Notices and Adjudication proceedings. Appeals: If demand order is received Appeal must be filed within 3 months and 10% pre-deposit is mandatory.

- DRC-03A Adjustment : If tax was paid earlier using DRC-03 instead of demand payment facility, the new Form DRC-03A allows linking such payments with demand orders to avoid recovery proceedings.

- Administrative Compliance Checks : Businesses should also review Bank account details on GST portal, Aadhaar authentication of authorized signatory, Update of authorized signatory details and Proper record maintenance for audits

The year-end GST review is not just about filing returns. it is a comprehensive compliance exercise involving ITC reconciliation, vendor compliance monitoring, export compliance, regulatory threshold checks, and litigation management. Timely completion of these activities helps businesses avoid ITC reversals, prevent departmental notices, ensure smooth transition to FY 2026-27 and maintain accurate GST reporting