Table of Contents

Overview GST Returns & Compliance in India

Timely Goods and Services Tax compliance helps businesses to avoid penalties and notices, ensure smooth input tax credit flow, maintain good compliance ratings, and prevent business disruptions (e‑way bill blocking, registration suspension). This blog guide about what Goods and Services Tax returns are, types of returns, due dates, filing flow, Input Tax Credit rules, penalties, and compliance responsibilities under Indian Goods and Services Tax law.

What are GST returns?

GST returns are statutory statements filed by registered taxpayers to report outward supplies (sales), inward supplies (purchases), Tax collected and tax paid, and input tax credit claimed. They ensure transparency, tax matching, and correct revenue collection under the Goods and Services Tax.

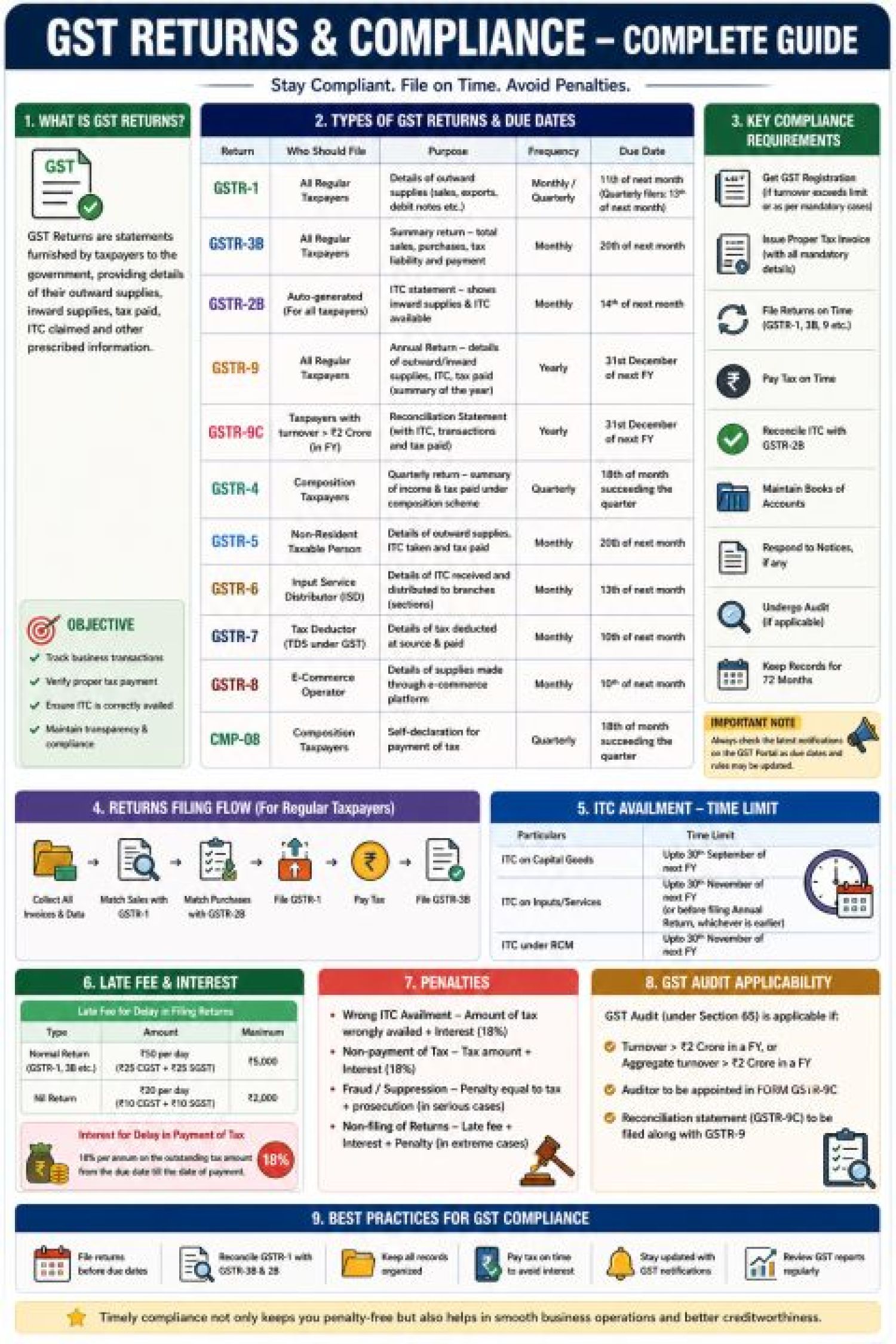

Types of GST Returns & Due Dates

GSTR 1

- Filed by: Regular taxpayers

- Purpose: Details of outward supplies (B2B, B2C, exports, credit notes)

- Frequency:

- Monthly (turnover > INR 5 crore)

- Quarterly under Quarterly Return Filing and Monthly Payment scheme

- Due date:

- Monthly: 11th of next month

- Quarterly: 13th of next month after quarter

GSTR 3B

- Filed by: Regular taxpayers

- Purpose: Summary return – tax liability, Input Tax Credit claimed, tax payment

- Frequency: Monthly / Quarterly (Quarterly Return Filing and Monthly Payment)

- Due date: 20th of next month (varied slightly under Quarterly Return Filing and Monthly Payment)

GSTR 2B

- Nature: Auto generated (not filed by taxpayer)

- Purpose: Shows eligible Input Tax Credit based on supplier filings

- Frequency: Monthly

- Generated on: 14th of next month

- Very important: Input Tax Credit should be claimed only as per GSTR‑2B

GSTR 9 (Annual Return)

- Filed by: Regular taxpayers

- Purpose: Annual summary of all Goods and Services Tax returns

- Frequency: Yearly

- Due date: 31st December of next financial year

- Optional for taxpayers with turnover up to INR 2 crore

GSTR 9C (Reconciliation Statement)

- Filed by: Taxpayers with turnover above INR 2 crore

- Purpose: Reconciliation between Goods and Services Tax returns & financial statements

- Audit requirement: Goods and Services Tax audit by a CA/CMA is not mandatory now and Self‑certified reconciliation

- Due date: 31st December

- Filed along with GSTR 9

- Goods and Services Tax audit requirement Current Position: Earlier, a mandatory GST audit applied if turnover exceeded INR 2 crore. However, now abolished. The current requirement is to self-certify GSTR‑9C; there is no compulsory Chartered Accountant and Cost and Management Accountant audit under Goods and Services. Tax law and departmental audits can still be conducted.

CMP 08

- Filed by: Composition scheme taxpayers

- Purpose: Quarterly tax payment declaration

- Frequency: Quarterly

- Due date: 18th of the month following the quarter

Key GST Compliance Requirements

To remain fully compliant, a business must obtain Goods and Services Tax registration (if applicable), issue proper Goods and Services Tax invoices, file returns on time (GSTR 1, GSTR 3B, etc.), then pay GST within due dates, reconcile input tax credit with GSTR 2B, maintain proper books of accounts, respond to Goods and Services Tax notices, file annual return & 9C (if applicable), and preserve records for 72 months (6 years).

Goods and Services Tax Return Filing Process

- Collect all sales & purchase invoices

- Prepare and file GSTR 1 (sales data)

- Verify purchases & Input Tax Credit using GSTR 2B

- Compute tax liability

- Pay Goods and Services Tax

- File GSTR 3B

- Filing GSTR 1 before GSTR 3B ensures accurate input tax credit reporting for recipients.

Input Tax Credit Time Limit:

ITC can be claimed up to the earlier of 30th November of the next financial year OR the date of filing GSTR‑9 (Annual Return). Applicable to Inputs (goods & services), capital goods, and the reverse charge mechanism (RCM).

Late Fee & Interest

Late Fee : INR 50 per day (INR 25 CGST + INR 25 SGST) and INR 20 per day for NIL returns. The maximum cap is INR 5,000 (normal return) and INR 2,000 (NIL return), and also interest will be applicable, i.e., 18% per annum on delayed payment of tax, and that is to be calculated from the due date till the payment date.

Penalties under Goods and Services Tax

- Wrong or excess ITC → Tax + 18% interest

- Non‑payment / short payment → Tax + interest

- Fraud / suppression → Heavy penalty + prosecution

- Non‑filing of returns → Late fee + penalty + blocking of e‑way bills