Table of Contents

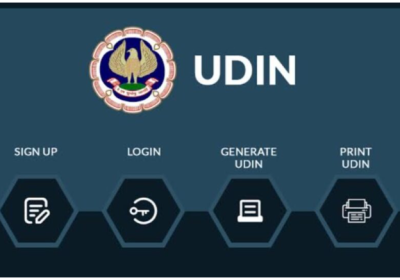

Big Changes in Checklist & Reporting Enhancements in ICAI UDIN System/Portal for Tax Audits

New Checklist & Reporting Enhancements under ICAI UDIN System

ICAI has made key updates introduced by the Institute of Chartered Accountants of India in the Unique Document Identification Number system to strengthen compliance and ensure proper reporting in tax audit assignments. This enables better tracking and helps ensure adherence to audit limits prescribed by the Institute of Chartered Accountants of India.

These updates are aimed at improving transparency, accountability, and compliance discipline in tax audit reporting. Members are advised to exercise due diligence while generating a unique document identification number to avoid discrepancies.

Key Updates in ICAI UDIN portal

Following Key Updates from The Institute of Chartered Accountants of India Unique Document Identification Number System for Checklist & Reporting Enhancements related under ICAI UDIN portal

- New Checklist for Section 44AB(e) Selection: A mandatory checklist has been introduced while selecting Section 44AB(e) during Unique Document Identification Number generation

- Objective: The objective of this change is to ensure strict applicability of Section 44AB(e), prevent incorrect use of presumptive taxation clauses, and avoid misuse of the 60 tax audit assignment limit under other clauses.

- Additional Fields in UDIN Particulars: For cases where the presumptive taxation scheme is NOT applicable, new details must be reported. Whether the audit report is original or revised, If revised, mention the UDIN of the original TAR, then the nature of the assignment under the head office and branch (separate UDIN required where applicable).

- A new monitoring feature now displays: Whether the Tax Audit Report is original or revised. If revised, the unique document identification number of the original tax audit report must be provided. Nature of Assignment: Head Office and Branch (separate unique document identification number required where applicable).

- New UDIN Dashboard Feature: A dedicated Unique Document Identification Number Quota Monitoring Dashboard has been introduced showing Total Tax Audit Count and Remaining Tax Audit Count.

What This Means for Chartered Accountants:

These updates clearly signal: Tighter the Institute of Chartered Accountants of India monitoring, Improved transparency in audit assignments and Stronger compliance control over tax audits. Professionals must exercise greater accuracy while selecting clauses and ensure proper reporting to avoid non-compliance risks. A step forward towards a more transparent and accountable Tax Audit ecosystem.

In summary, under the UDIN Dashboard:

The Institute of Chartered Accountants of India has rolled out major updates in the UDIN portal specifically impacting tax audit reports, bringing in tighter compliance and better monitoring mechanisms. To ensure correct applicability of Section 44AB(e), which prevents misuse of the 60 tax audit limit under other clauses. For cases where the presumptive taxation scheme is not applicable, the following details are now required & added features like Total Tax Audit Count, Remaining Tax Audit Count, & UDIN Quota Count Section