Table of Contents

GST on Interest Income applicability Business Owner Must Know

Understanding Goods and Services Tax implications on interest income are crucial for businesses, professionals, and tax consultants. While many assume interest is completely exempt, the reality depends on the nature of the transaction. Interest income under Goods and Services Tax is one of the most misunderstood areas. Even though Goods and Services Tax generally exempts pure interest; it still affects registration, input tax credit reversal, invoicing, and taxability of certain charges. Below is a crisp but authoritative breakdown backed by updated 2025–26 references.

What is "interest" under GST? : Under Section 2(75) of the Central Goods and Services Tax Act, 2017, money is neither goods nor services. However, activities involving money, such as lending or deposit-taking, may qualify as financial services. GST applies only when there is a “supply” of goods or services. Under Goods and Services Tax, interest is the consideration charged for the use of money. “Money” itself is neither good nor a service, but the use of money can be a financial service. However, most interest is exempt due to specific notifications.

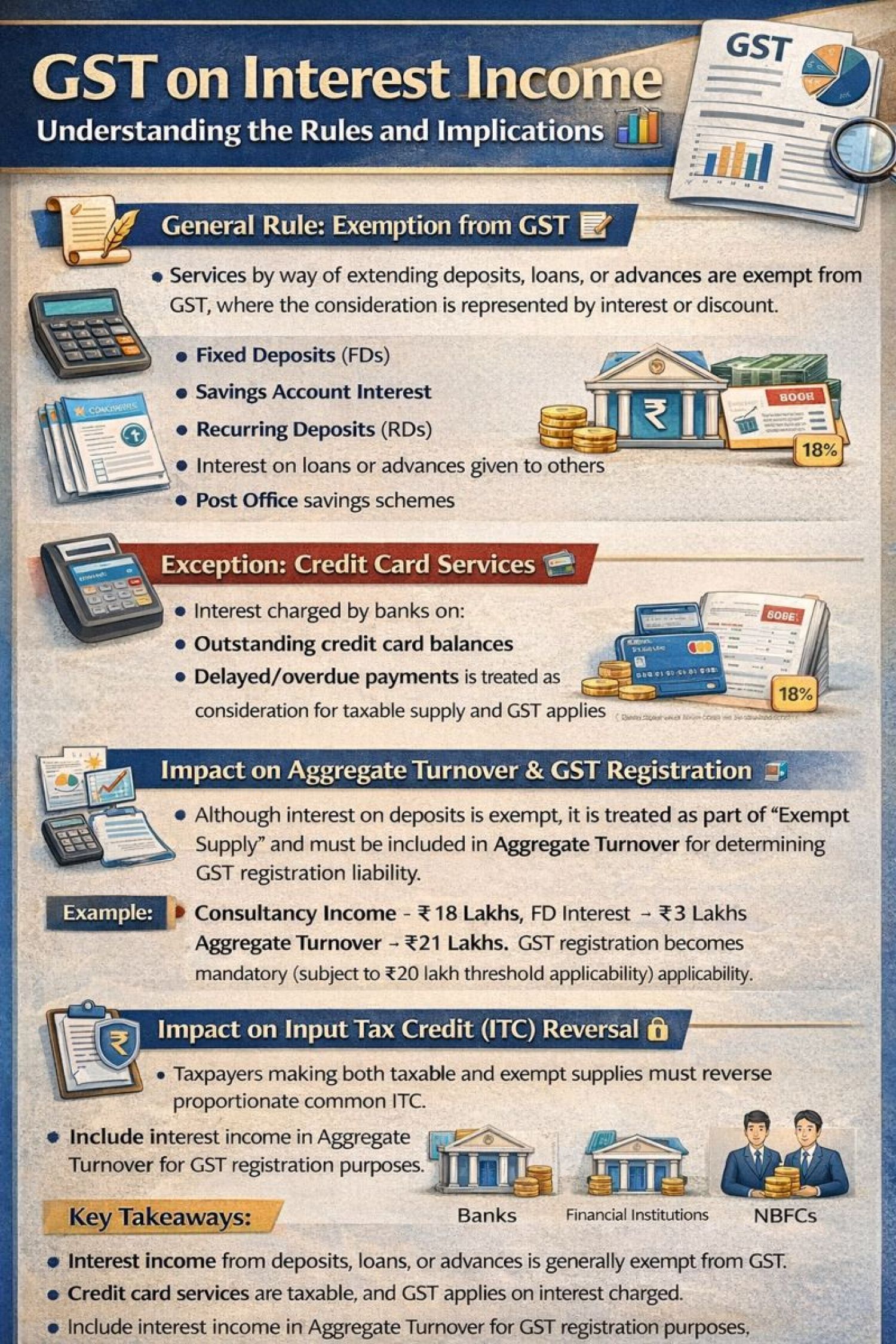

As per Goods and Services Tax law, interest on loans, deposits, or advances is exempt from Goods and Services Tax. This includes interest received from business loans, interest on unsecured loans, interest on deposits, and interest charged for delayed payment (if separately mentioned as interest). Covered under exemption notification relating to “services by way of extending deposits, loans, or advances where consideration is represented by way of interest.”. Only the interest portion is exempt. Any additional processing fees, documentation charges, or service charges are taxable.

Interest on Delayed Payment—Taxable or Exempt? : This is where confusion arises. U/s 15(2)(d) of the Central Goods and Services Tax Act, 2017, interest or late fees for delayed payment of consideration is included in the value of supply. If interest is charged for delayed payment of a taxable supply, GST applies on such interest. And If it is interest on a loan transaction, it remains exempt. Therefore, late payment charges related to the sale of goods/services are taxable, and interest on loans given is exempt. So we can say that pure interest is exempt from Goods and Services Tax. If not exempt, it would attract 18% Goods and Services Tax (standard rate)

Interest Income—Fully Exempt from GST (Major Rule) : As per Notification 12/2017 CTR, Entry 27, the following are exempt from FD/RD interest, savings account interest, interest on loans or advances (including intercompany loans), and interest from post office schemes. Because these are pure time-value-of-money transactions and not considered “supply” for GST purposes.

Interest on Income Tax Refund—Goods and Services Tax ? Interest received from the Income Tax Department (e.g., u/s 244A of the Income Tax Act) is Not a supply, not consideration for any service and Therefore Not liable to Goods and Services Tax.

When Interest IS Taxable (18% GST) : Credit Card Interest & Charges—Taxable: Interest on outstanding credit card dues & late payment charges attract 18% GST.

Penalties/penal charges by banks/financiers: RBI’s 2025 guidelines replaced “penal interest” with penal charges. CBIC clarified these are treated as charges for breach of contract and thus taxable under Goods and Services Tax .

Penal Interest—GST Applicability: Penal interest follows the same principle

- Penal interest linked to loan repayment → Exempt

- Penal charges for breach of contract (not in nature of interest) → Taxable

The classification depends on whether the amount is compensatory (interest) or consideration for a separate supply.

Interest on Late Payment of Invoice: Interest charged by a supplier for delayed payment of invoice value is taxable, because it forms part of “value of supply” u/s 15(2)(d).

GST Registration Impact—Biggest Trap for Businesses! Even though interest is exempt, it counts in aggregate turnover for GST registration purposes. Example: Consultancy Income: INR 18 lakh and FD Interest: INR 3 lakh. Total Turnover = 21 lakh → GST registration becomes mandatory (threshold INR 20 lakh). This is where many small taxpayers get caught.

BUT ITC Reversal is NOT Required for Most Taxpayers: For ordinary businesses, exempt interest income is NOT counted as exempt supply for ITC reversal purposes under Rule 42/43. Meaning taxpayers include it for the turnover threshold. But you do not reverse ITC because of it. ITC Reversal is NOT required for most taxpayers having exceptions like banks/NBFCs; they must reverse ITC proportionately (common credit rules apply).

Impact on ITC (Input Tax Credit) : Even though interest income may be exempt If a business earns exempt interest income regularly (like NBFCs or financing companies), ITC reversal under Rule 42 may apply. For companies earning incidental interest (e.g., FD interest), proportionate reversal may be required. This becomes important during GST audits and annual return reconciliation.

Special Cases in case of GST on Interest Income

- Intercompany Loans: Interest is exempt (notification confirmation + AAR rulings).

- Interest from partnership capital: Generally exempt (pure interest), though treatment for registration thresholds may have differing opinions. (Recent expert opinions suggest it may not count for threshold; ref. 2024 expert clarification.)

- Delayed EMI & Financial Penalties: EMI interest is exempt, but charges/penalties may be taxable depending on nature—RBI’s 2025 framework clarifies penal charges separately, making them taxable.

Key Takeaways for Business Owners

- No GST on FD/RD interest, savings interest, loan/advance interest, inter-company loan interest, and EMI interest (pure interest).

- GST @ 18% will be levied on credit card interest/late fees, penal charges per RBI 2025 rules, interest for late payment of invoices, and charges ancillary to lending (processing fee, foreclosure charges, etc.).

- GST Registration in case Interest income included for threshold and May force GST registration even if the taxable supply is small

- ITC Rules: Interest income ignored for exempt‑supply ITC reversal (for most businesses) and Banks/NBFCs must reverse ITC proportionally

Exempt vs Taxable Components

|

Exempt Components |

Taxable Components |

|---|---|

|

Interest on loans |

Credit card interest |

|

Savings account interest |

Late payment charges |

|

Fixed deposit interest |

Penalties linked to supply |

|

Inter-company loan interest |

No-cost EMI (embedded interest) |

|

NBFC loan interest |

Loan processing fees |

Practical Examples

|

Scenario |

GST Applicable? |

|---|---|

|

Interest on business loan given |

No |

|

Interest on FD |

No |

|

Late payment interest on sale invoice |

Yes |

|

Processing fees on loan |

Yes |

|

Penal interest on EMI delay (loan) |

No |

Key Principle to remember: If the nature is pure lending, it is exempt. And If it involves service or an additional charge, GST applies. And nce interest income is exempt. Businesses may need proportionate ITC reversal (Rule 42). Important for NBFCs and companies earning substantial exempt income. GST applies on processing fees, documentation charges, and other service elements.