Table of Contents

A Practical Guide to goods and services tax Law Para 5(e) Compliance

GST Tax Rate & ITC Implications under Para 5(e)

Paragraph 5(e) of Schedule II (agreeing to tolerate an act, refraining from an act, or doing an act ) was once one of the most litigated provisions under goods and services tax law. That uncertainty is now largely settled. Thanks to Central Board of Indirect Taxes and Customs Circulars 178/10/2022‑GST, 102/21/2019‑GST, and 186/18/2022‑GST, the tax position is clearer than ever. The key test today is intent.

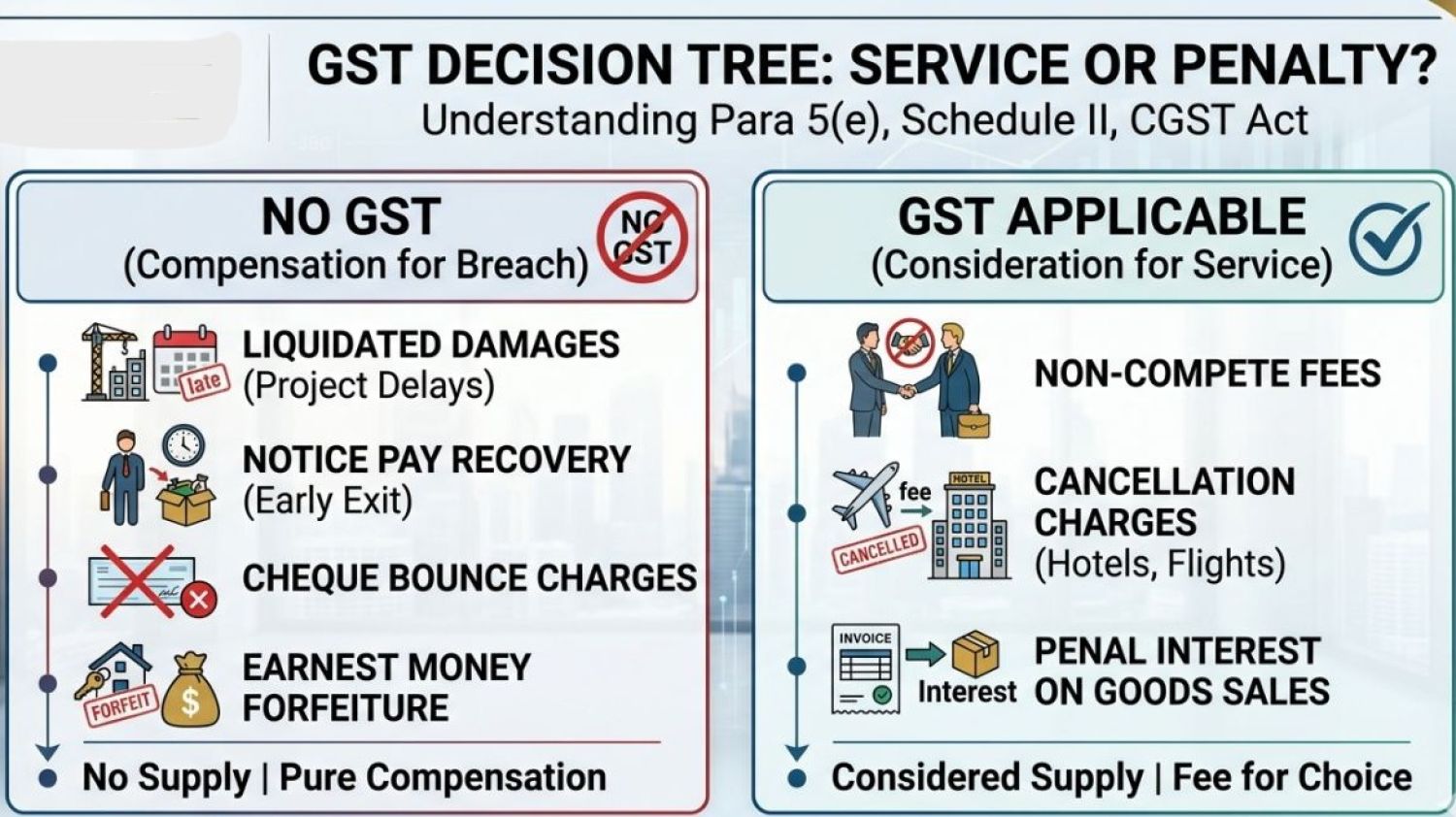

NO GST Compensation for Breach (No Supply): These amounts are not consideration for a service.

They arise only because a party has breached a contract, and the payment merely compensates the aggrieved party for loss or inconvenience. Typical examples include the following:

- Liquidated Damages : Compensation for delay or non‑performance in construction, EPC, or supply contracts.

- Notice Pay Recovery : Amount recovered from an employee who exits without serving the contractual notice period.

- Cheque Bounce Charges: Penal recovery triggered due to dishonor of payment, not for any agreed facility.

- Forfeiture of Earnest Money / Security Deposit : Retention of deposit due to failure to conclude a transaction.

goods and services Tax Law Position: These are treated as “No Supply” because there is no intention to provide a service of tolerance—only enforcement of contractual discipline.

GST APPLICABLE — Consideration for a Service: Here, the situation is fundamentally different.

The payment is pre‑agreed, intentional, and made in exchange for a facility or a choice.

Common instances include:

- Non‑Compete Fees: A conscious agreement where one party is paid to refrain from competing.

- Cancellation Charges (Hotels / Airlines / Events) : Charges levied to manage blocked inventory or capacity, not merely to penalize.

- Penal Interest on Sale of Goods: Additional interest charged for delayed payment of sales invoices. Taxable at the same GST rate as the underlying goods.

Goods and services tax position: These payments qualify as consideration for a taxable service under Para 5(e).

- GST Tax Rate: The services are generally classified under SAC 9997, attracting a GST rate of 18%.

- Reversal of ITC: If the consideration for these services is not paid, or if they are exempt, ITC reversal may be necessary.

- Proper documentation and identification of such transactions in contracts are crucial for compliance to avoid disputes regarding penalty-related payments.

How to Manage Para 5(e) Compliance Smartly - Best Practices to Avoid Disputes

Draft Contracts Carefully: Use words like "penalty," “liquidated damages," and "compensation for breach." Avoid language suggesting a “fee for tolerance” or optional behavior. Intent flows from drafting.

Contractual Documentation

- Clearly distinguish between compensation for breach vs. agreed toleration/optional facility

- Use explicit breach language such as "Penalty," "Damages," and “Compensation for non‑performance."

Accounting Treatment: Separate GL codes for contractual damages, cancellation income, and non-compete receipts. Mixed treatment is a red flag in audits.

Documentation Is the Real Defense (CBIC View) : CBIC has repeatedly emphasized that classification depends on intention and documentation, not labels alone.

Applicable Tax Rate: Where Para 5(e) services are held taxable, they are generally classified under SAC 9997. (“Other services”, including agreeing to tolerate an act/refrain from an act).

GST Rate: 18% (9% CGST + 9% SGST or 18% IGST) :

This applies to non‑compete arrangements, cancellation / retention charges treated as consideration, and penal interest linked to taxable outward supplies. Reversal of Input Tax Credit (ITC) – Key Considerations ITC implications often get ignored in Para 5(e) cases and later become audit triggers.

Nonpayment of consideration: If consideration for a taxable Para 5(e) service is not paid within 180 days from the invoice date. ITC reversal is required under Section 16(2) (ITC can be reclaimed upon subsequent payment.)

Exempt or Non‑Supply Transactions : If amounts received are compensation for breach, liquidated damages, or penalty recoveries (no supply).

ITC attributable to such receipts may need reversal. under Rule 42 / Rule 43, if common credits are involved. This becomes critical where a contract has both taxable and non‑taxable components and damages are substantial (infrastructure, EPC, and PSU contracts).

Invoicing Discipline Invoice the Right Way :

- Penalty / damages → Commercial Debit Note (No GST)

- Para 5(e) taxable services → Tax Invoice with SAC 9997

- Damages / penalties → Commercial Debit Note (No GST).

- Non‑compete / cancellation / toleration services → Tax invoice with GST. Documentation decides taxability.

Remember the interest distinction (Circular 102) under goods and services tax law :

- Penal interest on loans or advances → goods and services tax Exempt

- Penal interest on delayed sale consideration → goods and services tax Taxable

- The nature of the transaction matters more than the name.

The rule of thumb under goods and services tax law :

If the money compensates for a loss caused by breach → goods and services tax free.

If the money is paid for a negotiated choice or facility → goods and services tax applies. Or simply put

Compensation = No GST

Consideration = GST

Final Practitioner Rule- GST Tax Rate & ITC Implications under Para 5(e)

|

Nature of Receipt |

GST |

ITC Impact |

|

Compensation for breach |

No GST |

Possible ITC reversal |

|

Liquidated damages |

No GST |

Possible ITC reversal |

|

Non‑compete fees |

18% |

ITC eligible |

|

Cancellation charges |

18% |

ITC eligible |

|

Penal interest on loans |

Exempt |

ITC reversal rules apply |

|

Penal interest on sales |

Same rate as goods |

ITC eligible |