Table of Contents

Must Know Significant changes in ITR Form for FY 2025-26

Changes in Latest ITR Forms for FY 2026–27

| FORM | APPLICABLE TO | KEY AMENDMENTS / CHANGES |

|---|---|---|

| ITR-1 (Sahaj) | Resident individuals (Salary, 1 house property, other sources, agri income up to ₹5,000) | • Up to 2 house properties allowed (earlier 1) • LTCG u/s 112A up to ₹1.25 lakh allowed • New field: Secondary / Additional Address • Revised capital gains schedules |

| ITR-2 | Individuals / HUF not eligible for ITR-1 (e.g., foreign assets, more than 2 house properties, director in company) | • Revised capital gains schedules • Additional disclosures for foreign assets & trusts (Schedule FA) • New field: Secondary / Additional Address |

| ITR-3 | Individuals / HUF having income from business or profession | • Enhanced disclosure of F&O transactions • Detailed reporting for trading income • Revised capital gains schedules • Disclosure of buyback losses • New field: Secondary / Additional Address |

| ITR-4 (Sugam) | Presumptive income cases (Sections 44AD, 44ADA, 44AE) | • LTCG u/s 112A up to ₹1.25 lakh allowed • Mandatory disclosure of bank balances • New field: Secondary / Additional Address |

| ITR-5 | Firms, LLPs, AOPs, BOIs | • Revised capital gains schedules • Alignment with new I-T Act provisions (2025 updates) |

| ITR-6 | Companies (excluding those claiming exemption u/s 11) | • Revised schedules for share capital, indebtedness, tax incentives • Enhanced disclosures for transactions & related parties |

| ITR-7 | Persons including companies claiming exemption u/s 11 (trusts, political parties, research institutions, etc.) | • Revised schedules for income, application, accumulation • Enhanced disclosures for foreign contributions & assets |

Notable Schedules Strengthened

- Schedule CG (Capital Gains)

- Schedule FA (Foreign Assets)

- Schedule AL (Assets & Liabilities)

- Schedule BP (Business/Profession)

- Schedule 80GGA / 80GGC (Donations)

ITR Return Forms

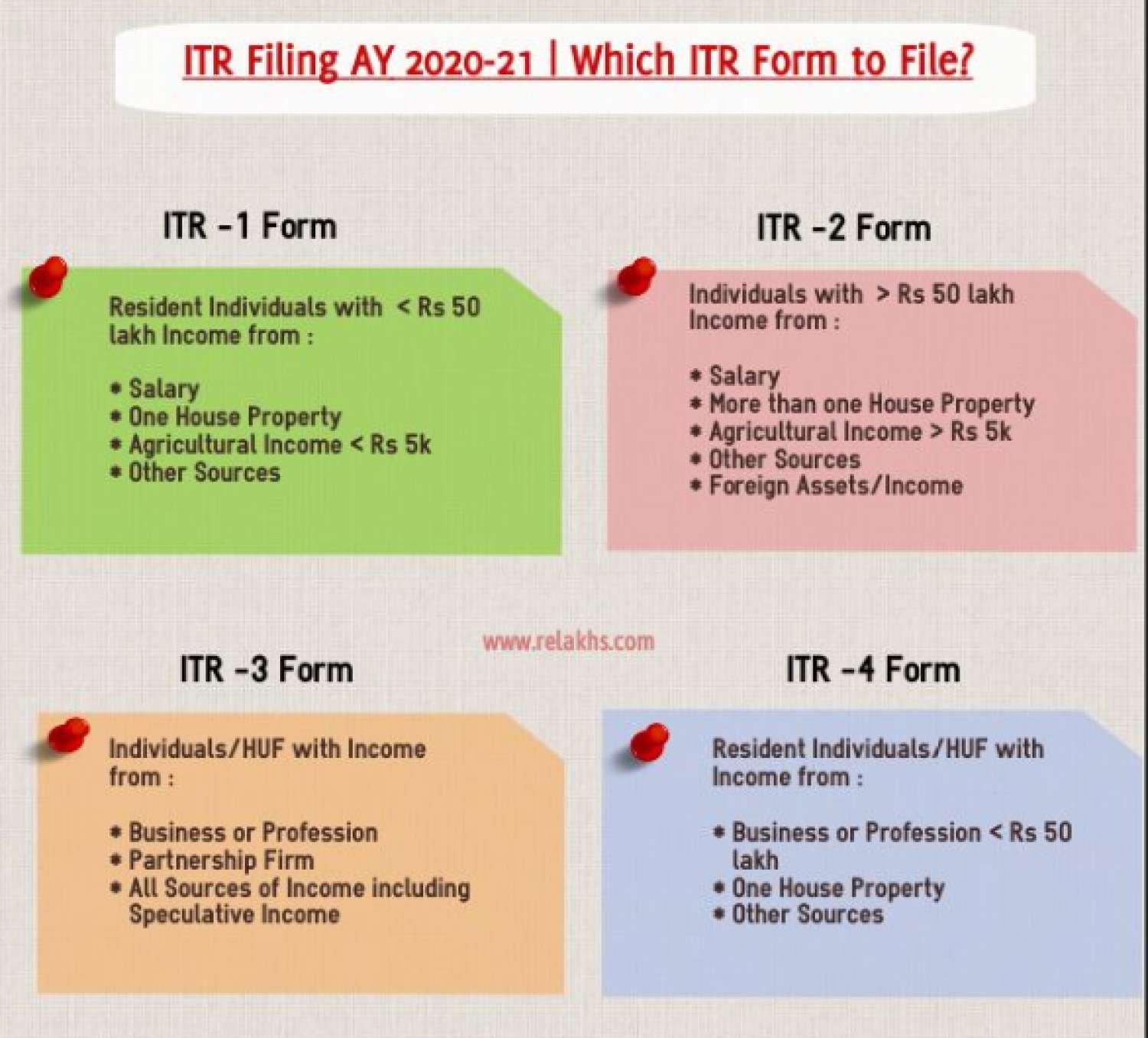

|

Sr. No. |

ITR Forms |

Instruction for Filing ITR Forms |

Description |

|

1. |

To be filed by resident individuals having total income up to ? 50 lakhs from following sources :

|

||

|

2. |

For Individuals and HUFs not having income from profits and gains of business or profession |

||

|

3. |

To be filed by Individuals and HUFs having income from profits and gains from business or profession |

||

|

4. |

For Individuals, HUFs and Firms (other than LLP) being a resident having total income up to Rs. 50 lakhs and having income from business and profession which is computed under sections 44AD, 44ADA or 44AE |

||

|

5. |

For firms, LLP, AOPs, BOIs, Artificial juridical Person, Estate of deceased, estate of insolvent, business trust and investment fund. |

||

|

6. |

For Companies other than companies claiming exemption under section 11. |

||

|

7. |

For persons including companies required to furnish returns under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) or section 139(4E) or section 139(4F) |