Table of Contents

- Key Update: Itr-3 Excel Utility Released For Ay 2026-27

- Income Tax Update | Itr-3 Utility Released

- Who Should File Itr-3?

- How To Use The Itr-3 Excel Utility?

- Important Itr Forms At A Glance

- Itr-3 For F&o Traders – Ay 2026-27

- Key Changes Highlighted For Ay 2026-27

- Ai-based Tax Scrutiny

- Major Change For F&o And Intraday Traders

- Important For F&o Traders

- How To Calculate F&o Turnover

- Common Mistakes Made By F&o Traders

- Important Records To Maintain

- Loss Set-off Rules

- Due Date For Ay 2026-27

- Practical Checklist Before Filing Itr-3

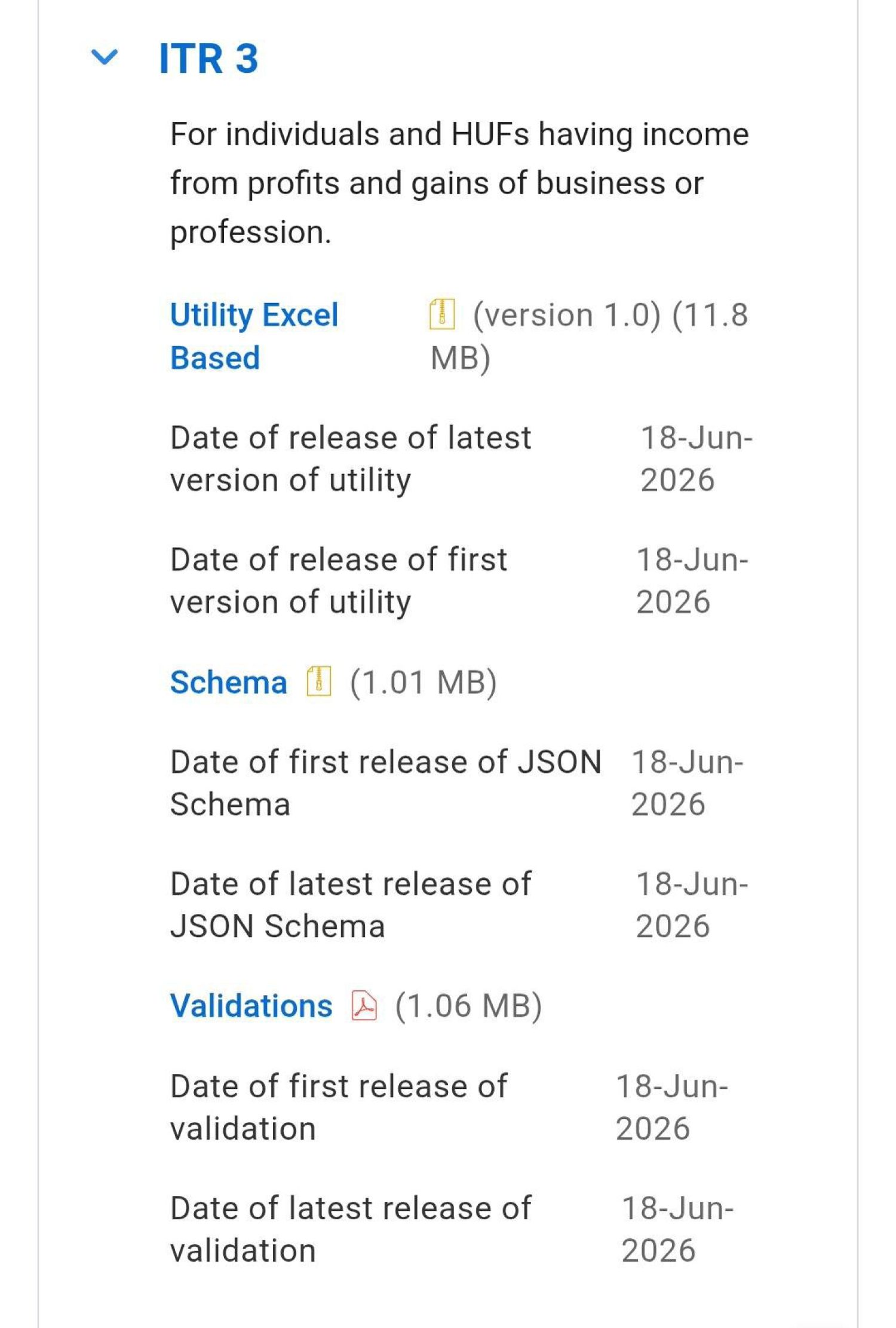

Key Update: ITR-3 Excel Utility Released for AY 2026-27

The Income Tax Department has released the Offline & Excel Utility for ITR-3 for AY 2026-27. ITR-3 is applicable to individuals and HUFs having income from profits and gains of a business or profession. Excel Utility Version: 1.0, Release Date: 18 June 2026, Offline filing utility now available. The due date for filing ITR-3 in non-audit cases is 31 August 2026. Taxpayers and professionals can now start preparing and filing returns using the released utility. Tax professionals, business owners, and other eligible taxpayers should start compiling financial information and complete their return filing well before the due date to avoid last-minute issues.

Income Tax Update | ITR-3 Utility Released

The Income Tax Department has now made the Excel Utility for ITR-3 available on the e-filing portal for Assessment Year (AY) 2026-27 (Financial Year 2025-26). This enables taxpayers having business or professional income to prepare their returns offline and upload the generated JSON file on the portal.

Who Should File ITR-3?

ITR-3 is applicable to:

- Individuals and HUFs earning income from a business or profession.

- Proprietors maintaining books of accounts.

- Professionals such as Chartered Accountants, Doctors, Lawyers, Architects, Consultants, etc.

- Traders dealing in shares, derivatives, commodities, and other business activities.

- Partners receiving remuneration, interest, commission, etc., from partnership firms.

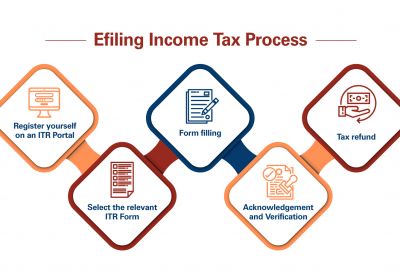

How to Use the ITR-3 Excel Utility?

- Log in to the Income Tax e-filing portal.

- Navigate to Downloads → Income Tax Returns.

- Download the latest ITR-3 Excel Utility for AY 2026-27.

- Fill in all required schedules and disclosures offline.

- Validate the data and generate the JSON file.

- Upload the JSON file on the portal.

- Complete verification through Aadhaar OTP, Net Banking, DSC, or other available methods.

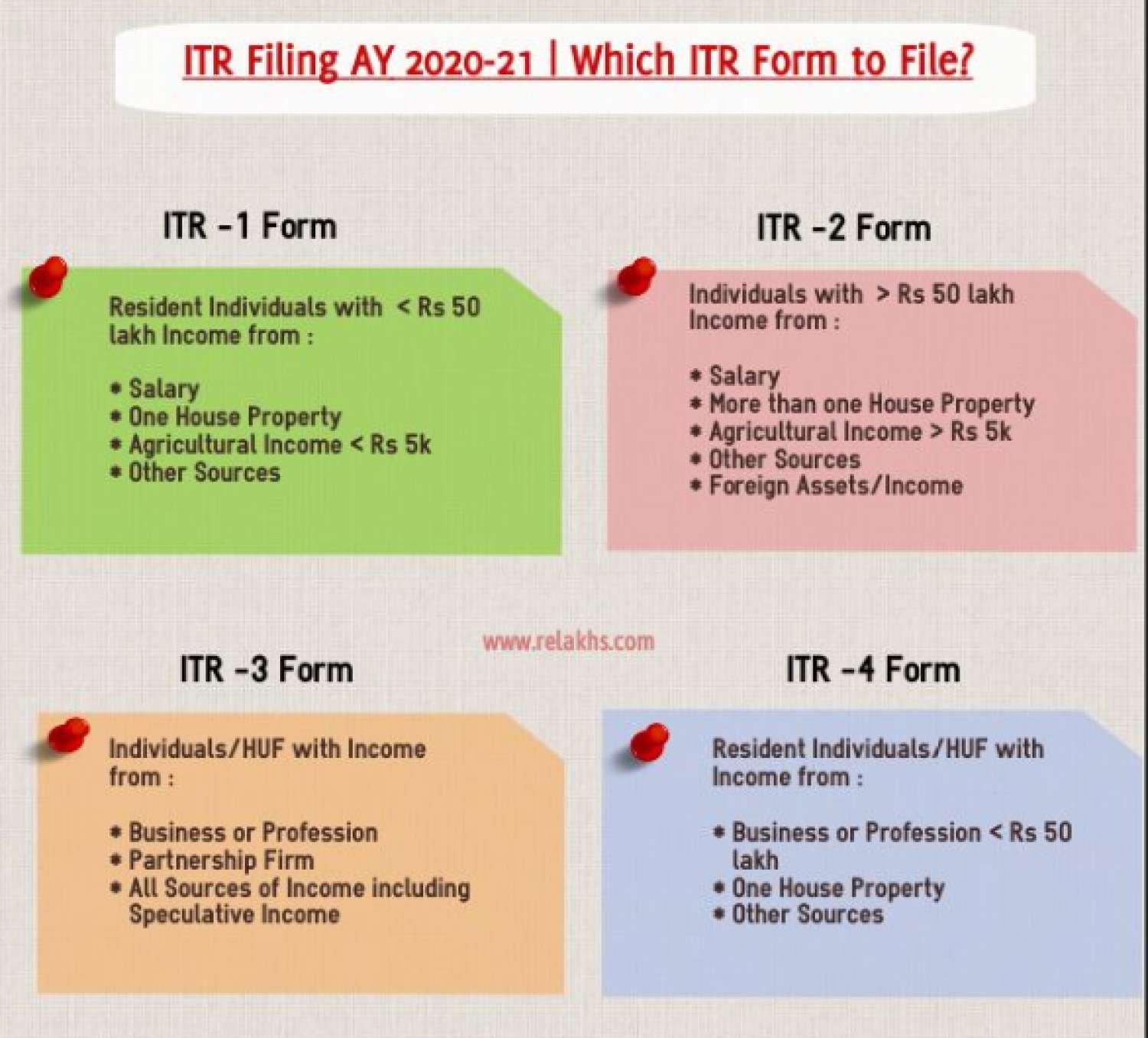

Important ITR Forms at a Glance

| ITR Form | Applicable To |

|---|---|

| ITR-1 (Sahaj) | Resident individuals with income up to ₹50 lakh from salary, one house property, and other sources |

| ITR-2 | Individuals/HUFs without business income |

| ITR-3 | Individuals/HUFs having business or professional income |

| ITR-4 (Sugam) | Presumptive taxation under Sections 44AD, 44ADA, or 44AE |

| ITR-5 | Firms, LLPs, AOPs, BOIs, etc. |

ITR-3 for F&O Traders – AY 2026-27

For taxpayers engaged in Futures & Options (F&O) trading, ITR-3 is generally the applicable return form because F&O income is treated as non-speculative business income under the Income Tax Act.

Key Changes Highlighted for AY 2026-27

1. Separate Disclosure of F&O and Intraday Transactions

- F&O turnover must be reported separately.

- Intraday trading should not be clubbed with F&O transactions.

2. F&O Income = Non-Speculative Business Income

Report F&O profit or loss under Profits & Gains from Business or Profession (PGBP)

Examples:

- Equity Futures

- Stock Futures

- Index Futures

- Options Trading

3. Intraday Trading = Speculative Income

Intraday equity trading profits/losses must be disclosed separately as: Speculative Business Income

This is different from F&O income.

4. Buyback Capital Loss Disclosure

A dedicated disclosure field has been introduced for reporting capital losses arising from buyback-related transactions.

5. GST Turnover Reconciliation

If GST registration exists, turnover disclosed in GST Returns, Books of Accounts, ITR-3, should be properly reconciled to avoid scrutiny.

AI-Based Tax Scrutiny

The Income Tax Department increasingly uses data analytics and AI tools to compare AIS (Annual Information Statement), TIS (Taxpayer Information Summary), Form 26AS, Broker Trade Reports, TDS Data, GST Returns, Bank Transactions, Books of Accounts and Even small mismatches may result in notices or scrutiny.

Major Change for F&O and Intraday Traders

For AY 2026-27, the revised ITR-3 requires:

- Separate reporting of futures & options turnover.

- Separate disclosure of F&O income/profit or loss.

- Reporting under Schedule Part A – Trading Account.

- Similar reporting requirements for intraday trading activities.

The objective is to improve transparency and enable better tracking of derivative transactions.

Important for F&O Traders

Many taxpayers incorrectly file ITR-4 for F&O transactions. Since F&O income is generally treated as non-speculative business income, such taxpayers are usually required to file ITR-3, subject to the applicable provisions of the Income-tax Act.Failure to provide the newly prescribed turnover and income details may result in the return being treated as defective and could lead to notices from the Income Tax Department.

How to Calculate F&O Turnover

For F&O transactions, turnover is not the contract value.

Absolute Turnover Method

Turnover =

- Sum of all favorable differences (profits)

- Sum of all unfavorable differences (losses)

Example

| Trade | Profit/(Loss) |

|---|---|

| Trade 1 | ₹40,000 |

| Trade 2 | (₹25,000) |

| Trade 3 | ₹15,000 |

Turnover = ₹40,000 + ₹25,000 + ₹15,000

Total Turnover = ₹80,000

Incorrect turnover calculation may affect Tax Audit applicability, Presumptive taxation eligibility and Compliance reporting

Common Mistakes Made by F&O Traders

-

Reporting F&O Income as Capital Gains

-

F&O income is generally business income, not capital gains.

-

Using Net Profit as Turnover

-

Turnover should be calculated using the absolute profit/loss method.

-

Reporting Intraday Income as Capital Gains

-

Intraday equity trading is speculative business income.

-

Filing ITR-2 Instead of ITR-3

-

Active F&O traders normally need to file ITR-3.

-

Ignoring AIS/TIS Reconciliation

-

Broker statements should match with AIS, TIS, Form 26AS, and Books of accounts.

Important Records to Maintain

- Maintain separate records for F&O Trading, Intraday Trading, Delivery-Based Equity Investments, Buyback Transactions and Freelance/Business Income (if any)

-

Reconcile Periodically Broker Ledger, Trade Summary, Contract Notes, Bank Statement, AIS/TIS, Form 26AS and GST Returns (if applicable)

Loss Set-off Rules

F&O Loss (Non-Speculative)

Can be set off against:

- Business Income

- Salary (not allowed)

- Capital Gains (not allowed directly)

Can be carried forward for 8 assessment years subject to timely filing of return.

Intraday Loss (Speculative)

Can be set off only against: Speculative Income

Carry forward allowed for 4 assessment years.

Due Date for AY 2026-27

Generally, for non-audit cases, the due date is 31 July 2026.

- 31 August 2026 – Non-audit cases filing ITR-3.

- 31 October 2026 – Cases requiring tax audit.

Practical Checklist Before Filing ITR-3

- Form 26AS

- Annual Information Statement (AIS)

- Taxpayer Information Summary (TIS)

- Form 16/Form 16A

- Profit & Loss Account and Balance Sheet

- Bank statements

- Capital gains statements

- F&O turnover and profit/loss computation

- Details of deductions and exemptions claimed

Taxpayers filing ITR-3 should carefully reconcile their books, AIS, TDS credits, and trading data before submission to avoid defective return notices and processing delays.