Table of Contents

Why Reporting Bank Balance as on 31st March 2026 Matters

Reporting the bank balance as of 31st March 2026 has become a critical compliance requirement for taxpayers in India, particularly from Assessment Year 2026 2027 onward. This disclosure directly impacts tax transparency, scrutiny risk, and the ability to justify financial transactions for FY 2025‑26. (Applicable from AY 2026‑27 | Especially Relevant for ITR 4 Filers).

Important Update for AY 2026 2027 - New Mandatory Requirement under ITR 4 (Sugam)

From Assessment Year 2026‑27, a new mandatory disclosure has been introduced in ITR 4. Income tax department required to reporting of the bank balance as on 31st March 2026: Taxpayers filing ITR‑4 are now required to mandatorily disclose the bank balance held as at the end of the financial year. With enhanced data analytics and expanded reporting requirements, the Income Tax Department now places greater reliance on year‑end bank balances to assess income consistency and detect potential mismatches.

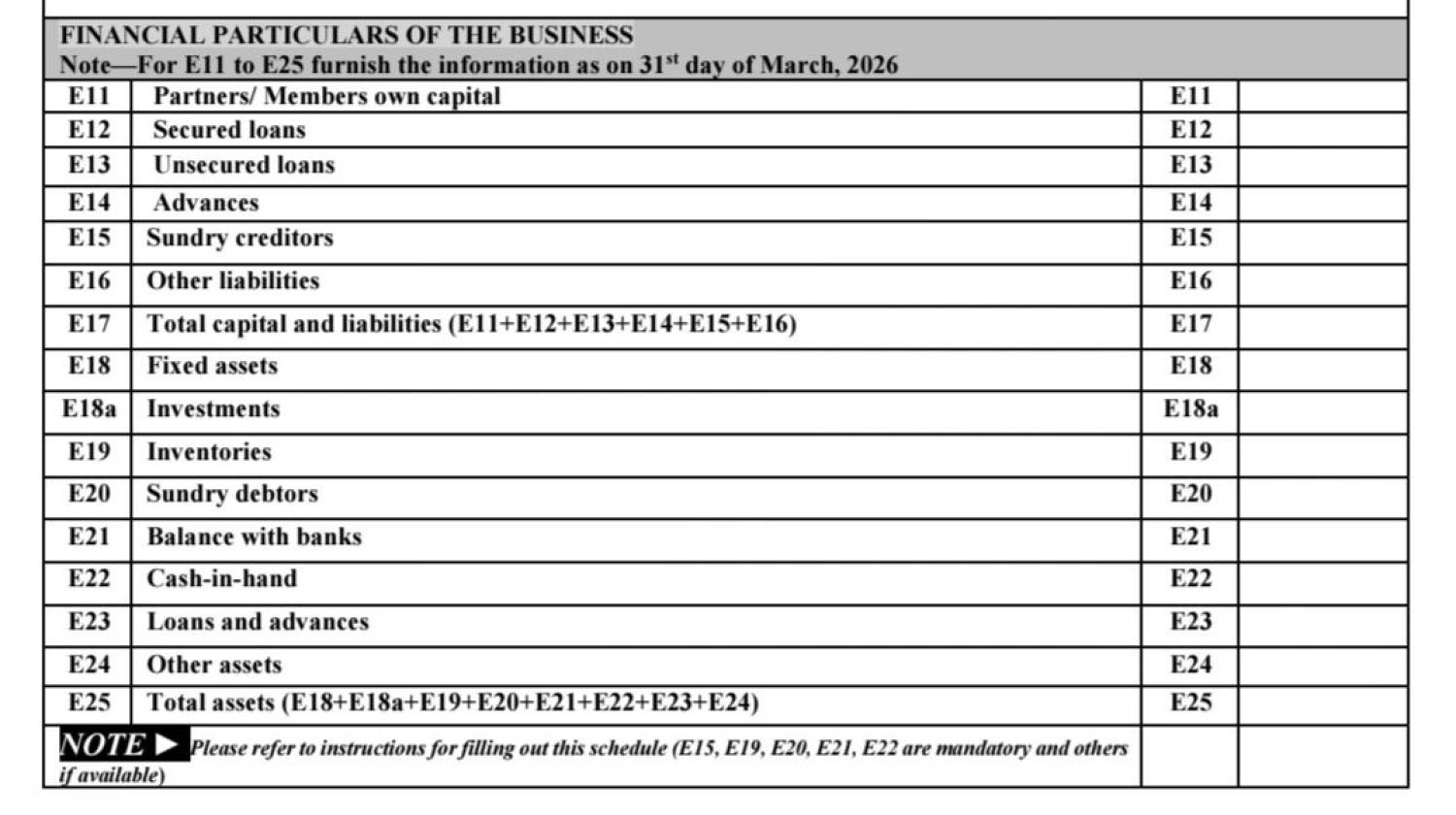

Earlier Position before FY 2026-27: Up to the previous assessment year, only the following details were mandatorily reportable in ITR 4:

- Sundry creditors

- Sundry debtors

- Inventories

- Cash‑in‑hand

There was no compulsory disclosure of bank balance.

Why Reporting of Bank Balance as on 31st March 2026 Matters for Taxpayer?

Reporting of Bank Balance as on 31st March 2026 Matters for Enhances financial transparency, Aligns presumptive taxation returns with data‑driven compliance, Helps the tax authorities reconcile cash flows and deposits and reduces inconsistencies with AIS / bank‑reported information. Even taxpayers opting for presumptive taxation must now Maintain year‑end bank balance details, Ensure consistency with bank statements and AIS data, Presumptive taxation simplifies income computation, not disclosure.

Key Reasons Why Reporting Bank Balance Is Important

- Mandatory Disclosure & Transparency: From FY 2025 26, taxpayers—especially those filing ITR‑4 (Sugam)—are required to mandatorily disclose the closing balance of operational bank accounts as on 31st March 2026. Presumptive taxation simplifies income computation not financial disclosure.

- Income Justification & Scrutiny Risk: The Income Tax Department uses advanced analytics to compare declared income, bank deposits during the year, and closing bank balances. A disproportionately high bank balance as on 31st March 2026, not backed by disclosed income or explained sources, may trigger scrutiny and be treated as unexplained money under Section 69A.

- Unexplained Cash Deposits & High Tax Exposure: Banks report high-value transactions to the department under Statement of Financial Transactions: savings account cash deposits exceeding INR 10 lakh in a year and Current account cash deposits exceeding INR 50 lakh

- AIS / TIS Reconciliation to Avoid Notices: Bank balances and transactions flow into Annual Information Statement and Tax Information Statement. Early reconciliation significantly reduces notice risk.

- Transition to the New Income Tax Act, 2025: With the Income Tax Act, 2025 coming into effect from 1st April 2026, accurate closure and reporting of FY 2025‑26 become even more critical.

- Multiple Bank Accounts Under One Permanent Account Number: The department tracks all bank accounts linked to a permanent account number across banks. Reporting all accounts ensures aggregate transaction visibility and elimination of fund‑splitting strategies to evade thresholds. Unreported accounts can themselves become a red flag.

Best Practices for Taxpayers

Year‑end bank balance disclosure is no longer a formality. It is a key data point for income validation, scrutiny selection, and compliance under the evolving tax regime. Accurate reporting today prevents costly explanations tomorrow. Following are Best Practices for Taxpayers:

- Maintain bank statements and justification documents (inheritance, gifts, past savings, loans, etc.) for at least 7 years

- Reconcile AIS and TIS before filing the ITR

- Track cash deposits and transfers periodically, not just at year‑end

- Ensure consistency between income declared, cash‑in‑hand, and bank balances