Table of Contents

RECOGNITION OF TAXABLE INCOME IN INDIA

NRIs are required to tax on any sought of income, being earned in India. Thus, as an NRI, one must pay tax in respect of following income -

• Income earned or received in India.

• Salary received or is expected to be received from the services rendered in India.

• Income that's directly or indirectly received in India.

• Income from a house property located in India, like rented property.

• All capital gains in India like on mutual funds, equities and bonds.

• Interest income arising on account of FDs or savings accounts made in India.

• Interest income earned on account of Non-Resident Ordinary accounts.

• Income arising on account of business, being conducted or controlled in India.

• any sought of gift, being received from a relative, in India worth more than Rs. 50,000.

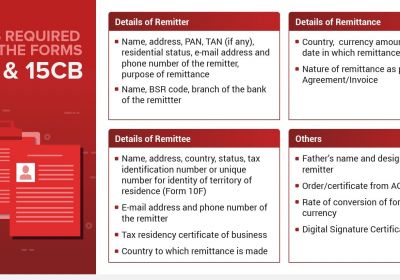

Non residence income taxpayers with No Permanent Account N​umber are exempted from compulsory online filing of Form 10F till 31/03/2023. Such category of Non residence income taxpayers may make statutory compliance of online income tax filing Form 10F till 31st March 2023 in manual form as was done before

STRATEGY FOR NRI BY RJA TAX EXPERT

Claim most of your deductions

As an NRI, you can’t claim many of the essential deductions available to resident Indians. For example, an NRI is ineligible to claim deduction under Section 80C in respect of contribution made to PPF or the National Savings Certificates. Apart from this, an NRI is also not entitled to claim deductions in respect of medical insurance and expenses. However, NRIs can invest within the National Pension System (NPS) in India and apply for tax deductions related to it.

NRIs can claim deductions in respect of contributions made towards NPS and the same shall be provided under Section 80CCD (1). A deduction of up to Rs. 1.5 lakh are often claimed. you'll claim an extra deduction of Rs. 50,000 on top of the Rs. 1.5 lakh deduction limit. Now in order to qualify for such an extra deduction, a person is required to exhaust their limit of Rs. 1.5 lakh by making investment in some other eligible options. Additional investments within the National Pension System is utilized to use for an extra deduction of Rs. 50,000.

Get a PAN card in India

A PAN or Permanent Account Number is employed to spot taxpayers in India. Resident Indians yet as NRIs need a Permanent Account Number to assert income tax refunds. Income earned above a specific threshold shall be taxed at source in India. Just in case you fail to supply your PAN number once you invest in India; you'll need to pay higher tax at the source amount. Procuring a Permanent Account number will facilitate you avoid higher or additional tax at the source.

Make the most of provisions

NRIs can significantly reduce their tax liability, by claiming the advantage of income tax provisions in respect of long-term assets, being purchased using foreign currency. On selling or transferring foreign assets, you may make profits or losses. Even though, the NRI is ineligible to deduct their capital gains on the sale or transfer of foreign assets, the same would be entitled to claim certain exemptions under Section 115F of Income Tax Act. Also, one can also convert their profit from sale of foreign assets, into the shares of any Indian company, or can also deposit the same into an Indian bank, or make any amount of contriution to NSC.

Claim home loan interest

NRIs can get tax deductions related to their Indian property. They will claim deductions on property taxes still as on interest and principal of their home loan in India. Therefore investing in properties in India could be a profitable proposition for NRIs. NRIs are also required to pay capital gains tax in respect of profit made from the sale of property situated in Indian. It's advisable to limit the amount of capital gains you create during a year to remain in an exceedingly lower income tax bracket.

Maintain your NRI status

Tax liability is set by the income and residential status of a private. If your residential status changes, your liabilities will change in India. Foreign income of NRIs isn't taxable in India. However, if their residential status isn't clear, their foreign income are often taxed in India. Hence, so as to avoid being trapped within the web of tax affairs, make your NRI status is simple. For this, one is required to plan their Indian visits in a way so that their NRI status remains clear.

NRI INVESTMENT IN INDIAN MARKET

NRIs can invest within the Indian securities market by purchasing shares through the Portfolio Investment Scheme (PIS) of the RBI. NRI investors are also eligible to make investment in government securities, debentures, listed non-convertible debentures, etc. and the same be made on repatriation and non-repatriation basis. However, it is to be noted that NRI investment in India’s equity shares, mutual funds, etc. shall be subject to certain restrictions/ conditions, being provided under the Foreign Exchange Management Act, 1999. Dividend income as well as the capital gains, being earned by NRIs, from the Indian listed shares and Equity Oriented Schemes, are also subject to taxation in India. NRI capital gains tax on shares depends upon the kind of instrument and also the period that they're held before the sale.

CAPITAL GAIN TAX FOR AY 2021-22

Below is the classification of NRI tax liability based on the category of instruments and therefore the period that the NRI holds them before selling.

- Long-term capital gain made from the Indian listed shares as well as the equity oriented mutual funds.

- Short-term capital gain made from India listed shares, or the equity-oriented mutual funds.

- Long-term capital gain made from sale of some other assets.

- Short-term capital gain made from sale of some other assets.

Capital gains tax on NRI investors is applicable within the same way as resident investors.

- Indian listed equity shares as well as the equity-oriented mutual funds, being owned by an investor, for a period exceeding 12 months shall be considered as a long-term investment. Thus, the sale of such instruments, would be subject to tax @ 10%, where the amount of long-term capital gain exceeds Rs. 1 lakh. However, in case the long-term gain does not exceed Rs. 1 lakh, the whole amount of gain would be exempt from LTCG tax. The said rate would be available without the benefit of indexation.

- LTCG tax on other assets – where the investment is made in unlisted equity shares or securities of an Indian company, the same shall be categorized as long term assets, where the holding period exceeds 24 months. The gain on such asset be taxed @ 10% without the availability of indexation benefits.

- Debt-oriented mutual funds are required to be held for a more than 36 months, in order to be categorized as a long term capital assets. The liabilities on capital gains from the sale of such kind of funds is 20% after indexation.

- Sale of Indian equity shares or equity oriented mutual fund units shall be classified as short-term capital gains, where the same is sold before 12 months from the date of acquiring the same. Such a STCG would be subject to 15% tax rate. Also, the investor is required to pay STT on such transactions as well.

- Short-term capital gains tax on other assets - The securities (other than debt mutual funds) and shares of an Indian company that are sold in but 24 months qualify as short-term capital asset.

- The deb-oriented mutual funds held for fewer than 36 months are classified as short-term assets. Short-term capital gain tax applicable on this kind of asset is calculated as per the tax slab rates.

PAYMENT OF CAPITAL GAINS TAX

Health and education cess chargeable at the rate of 4% are applicable over and above the given income tax rates and surcharge. Unlike the resident Indians, NRI investors aren't eligible to learn from the fundamental exemption limit. It is provided that TDS shall be deducted @ 30% in respect of STCG on unlisted securities.

Thus, before making investment in the Indian market, NRIs are advised to consult market experts, so that the NRI is able to take well informed decisions. You'll get detailed investment firm advisory from experts at RJA. You can download RJA website from the Google to ask any questions associated with investment available market/ mutual funds, NRI account opening online and tax filing in India. To ask any questions associated with Mutual Funds, click on the button below. Also visit our blog and YouTube channel for more details.

FAQs on NRI Taxablity

Q.: Do NRIs have to pay advance tax?

If their liabilities exceeds Rs. 10,000 in an exceedingly financial year, NRIs need to pay advance tax. Under Section 234B and Section 234C, interest are applicable if you don’t pay your advance tax.

Q.: Is there any tax for NRI in India?

An NRI having income earned or accrued in India, shall be subject to income tax in India. However, the income, being earned outside India, shall not be subject to income tax in India. Interest earned on NRE and FCNR savings and glued deposit accounts is tax-free in India. However, interest income arising on account of NRO account would be taxable.

Q.: What is the taxation rate for NRIs?

NRI income tax rates are mentioned within the first table together with the NRI tax slabs.

Q.: When should an NRI file an taxation return in India?

Just like resident taxpayers, NRIs are also required to file their income tax return in India, provided their taxable income in India exceeds Rs. 2.5 lakh in a particular FY. The last date for filing of ITR would be 31st July of the relevant assessment year.

Q.: Is an NRI subject to capital gains tax if he sells his house property in India?

Yes, an NRI are going to be at risk of pay capital gains tax in India upon the sale of his flat. The customer would be required to deduct TDS on the amount of gains made by the NRI. On such a tracsation, TDS be deducted @ 20%.

Q.: Can NRI claim TDS refund?

Where an NRI files their ITR, after the expiry of 12 months in India, the same would be eligible to claim the amount of TDS deducted on their income. For this, they have to compute their income and liabilities, as per the slab rates applicable to them.

Q.: Is TDS applicable to NRIs?

Interest income accruing on account of NRE and FCNR accounts would be tax-free in India and hence no TDS will be deducted on the same. However, in case of interest earned in respect of NRO account, the same would be taxable in India and would be subject to TDS @ 30%.

HOW RJA HELP

Due to a sophisticated legal system, understanding tax slab for NRIs and other tax laws will be confusing and NRIs may miss claiming deductions and other benefits. At RJA, we understand this struggle. you'll be able to visit RJA website to attach with our NRI Tax Experts and obtain end-to-end assistance associated with NRI tax filing. RJA will facilitate your get a lower TDS Certificate. to get more details, visit our website or the YouTube channel.