Table of Contents

- Itr-6 Complete Guide For Companies Filing Itr For Ay 2026-27 (fy 2025-26)

- Due Dates For Ay 2026-27

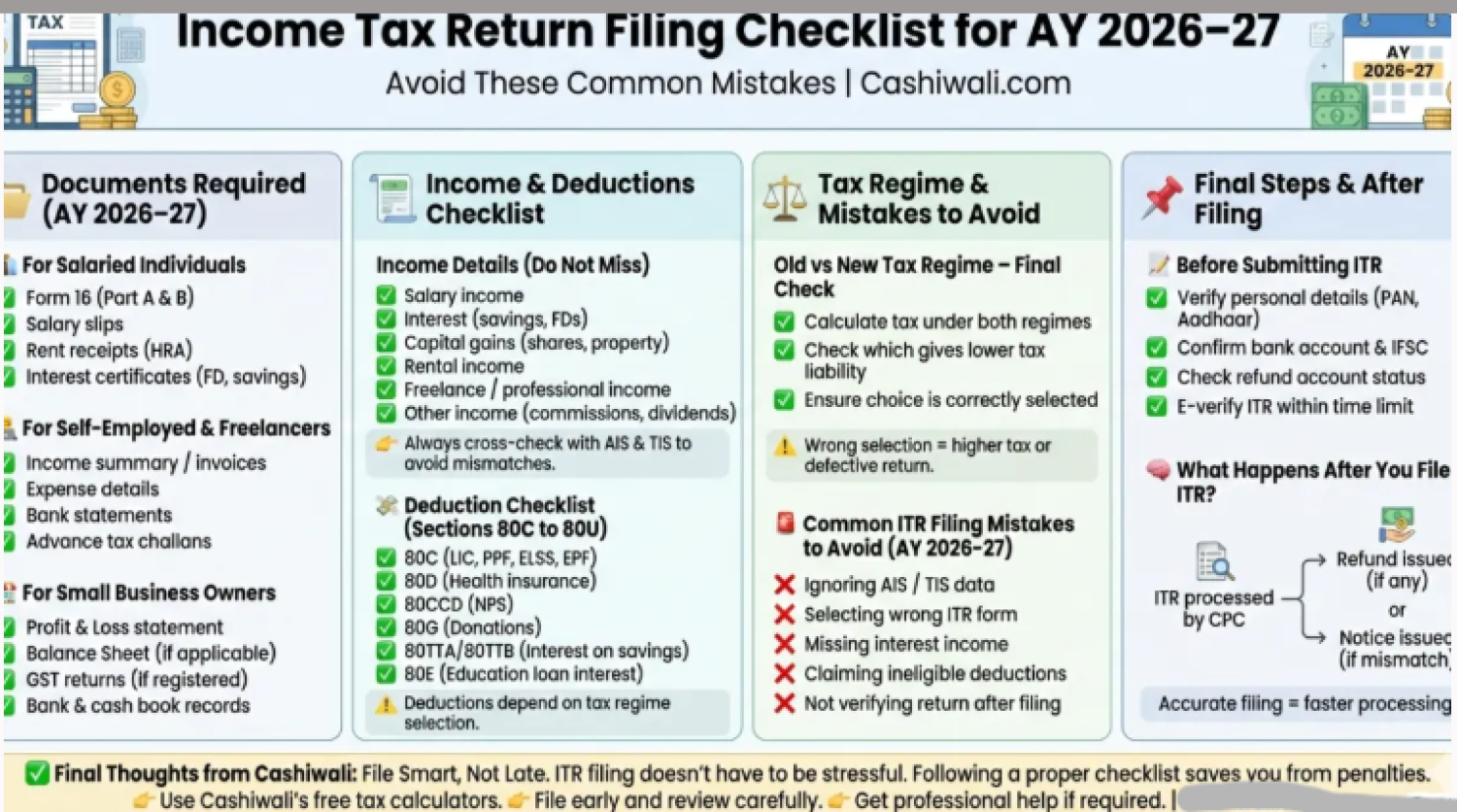

- Documents Required For Itr-6 Filing

- Itr-6 Filing Checklist

- What Are The Parts Of Itr 6

- Consequences Of Late Filing

- Mandatory Filing Method : Itr-6 Can Be Filed Only Through Electronic Mode. Filing Process

- Key Compliance Points And Common Errors

- Important Updates For Ay 2026-27

- Conclusion

ITR-6 Complete Guide for Companies Filing ITR for AY 2026-27 (FY 2025-26)

- ITR-6 is the income tax return form prescribed for companies registered in India to report their income, deductions, tax liability, and various financial disclosures under the Income Tax Act, 1961. This return form is applicable to companies that are not claiming exemption under Section 11 relating to income from property held for charitable or religious purposes. ITR-6 is one of the most detailed income tax return forms because companies are required to furnish extensive disclosures relating to financial statements, tax computations, audit details, deductions, related-party transactions, and regulatory compliances.

- The following entities are required to file ITR-6: Private Limited Companies, Public Limited Companies, One Person Companies (OPCs), Foreign Companies having taxable income in India, Companies earning income from Business or profession, Capital gains, House property, Other sources.

- The following entities cannot use ITR-6 Companies claiming exemption under Section 11 for charitable or religious purposes (required to file ITR-7), LLPs and Partnership Firms (required to file ITR-5), Individuals, Hindu Undivided Families (HUFs), Trusts, Associations of Persons (AOPs), Bodies of Individuals (BOIs), Political Parties

Due Dates for AY 2026-27

- Companies Subject to Audit- Due Date: 31 October 2026 : Applicable where audit is required under Section 44AB of the Income-tax Act, Companies Act audit provisions and Any other applicable law. Since most companies are mandatorily subject to statutory audit under the Companies Act, this due date applies in most cases.

- Companies Covered Under Transfer Pricing Provisions: Due Date: 30 November 2026 - Applicable where the company is required to furnish Form 3CEB and Transfer pricing report for international or specified domestic transactions

- Companies Not Requiring Tax Audit : Due Date: 15 September 2026: This generally applies only in limited situations because most companies are audited under corporate laws.

- Even dormant companies or companies with nil income are generally required to file an income tax return if they are registered under the Companies Act.

- Filing of income tax return is mandatory for companies irrespective of Profit or loss during the financial year, Business turnover, Business activity status. Failure to file may attract penalties and additional compliance consequences.

- ITR-6 is among the most comprehensive income tax return forms because it requires complete disclosure of a company’s financial and tax information.

Documents Required for ITR-6 Filing

Although physical documents are not attached with ITR-6, companies should maintain proper records and supporting documents.

A. Financial Documents: PAN of the Company, Audited Financial Statements, Balance Sheet, Profit & Loss Account, Cash Flow Statement, Notes to Accounts Books of Accounts and Bank Statements.

B. Tax Documents: Form 26AS, Annual Information Statement (AIS), Taxpayer Information Summary (TIS), TDS Certificates (Form 16A/16B/16C), Advance Tax Challans and Self-Assessment Tax Challans

C. Audit Documents: Form 3CA/3CB and Form 3CD, GST Reconciliation Statement (Form GSTR-9C), wherever applicable, Audit report acknowledgment and Details of auditor and audit report filing date

D. Other Supporting Documents :

- Form 10-IC under Section 115BAA

- Form 10-ID under Section 115BAB

- MAT computation working papers

- Transfer pricing documentation

- Capital gains computation statements

- ESOP/ESOS records

- ROC filings including AOC-4, MGT-7

- Previous year’s ITR acknowledgment and computation

Authentication Requirements

- Filing through Digital Signature Certificate (DSC) is mandatory

- Return must be verified by an authorized signatory

- An acknowledgment (ITR-V) is generated after filing

- E-verification must be completed within 30 days

Failure to verify the return within the prescribed period may render the return invalid.

ITR-6 Filing Checklist

Before filing ITR-6, ensure the following: like confirm eligibility to file ITR-6, Collect PAN, audited financial statements, Form 26AS, AIS and TIS, Reconcile books of accounts and tax records, Verify GST turnover and tax disclosures. Report all income sources accurately. Compute tax liability correctly, Pay outstanding advance tax or self-assessment tax, Upload audit report wherever applicable. Validate all schedules and disclosures, File the return before the due date and Complete e-verification within 30 days. Also, preserve records and supporting documents for at least six years.

What are the parts of ITR 6

A. Part A – Financial Information: This section captures detailed financial statement disclosures including:

- Financial Statements- Balance Sheet, Profit and Loss Account, Manufacturing Account, Trading Account, Cash Flow Details and Notes to Accounts

- Additional Financial Information: Sundry debtors and creditors, Loans and Advances, Fixed assets details, Depreciation schedules and Quantitative details of inventory

B. Income Schedules: Companies are required to disclose income under different heads such as Income from Business or Profession, Capital Gains, Income from House Property and Income from Other Sources. The return also contains schedules for Deduction claims, MAT (Minimum Alternate Tax) computation, AMT provisions, international transactions, Transfer pricing disclosures, Tax liability computation and Tax payments and TDS/TCS claims.

C. Part B – Tax Computation: Part B contains Total income computation, Tax liability calculation, Interest calculation and Refund or tax payable details

D. Verification: The return must be Verified by the authorized signatory of the company and Filed using a valid Digital Signature Certificate (DSC)

Verification Compliance: Failure to E-Verify the return within the prescribed timeframe may render the return defective or invalid.

E False Reporting Risks: Providing inaccurate information can attract prosecution under Section 277, including Monetary penalties and Imprisonment in serious cases.

Consequences of Late Filing

Delayed filing of ITR-6 may result in

- Late filing fee under Section 234F up to INR 10,000

- Interest under Sections 234A, 234B and 234C

- Loss of certain carry-forward benefits

- Increased scrutiny risk

- Notices and penalty proceedings

Mandatory Filing Method : ITR-6 can be filed only through electronic mode. Filing Process

- Step 1: Prepare the Return: Download the ITR-6 utility from the Income Tax e-Filing Portal and Alternatively, use authorized tax filing software

- Step 2: Fill All Schedules: Complete all relevant disclosures including financial statements, Income schedules, Tax computation, MAT details and TDS/TCS schedules.

- Step 3: Validate and Generate JSON: Validate all schedules and generate the JSON file for upload

- Step 4: Upload Return; Upload the return through the e-Filing portal.

Key Compliance Points and Common Errors

- Accurate Income Reporting: Companies must disclose all sources of income, including business income, capital gains, dividend income, interest income, and Incidental income. Non-disclosure may lead to assessment proceedings and penalties.

- Financial Statement Consistency: Ensure consistency between Audited financial statements, GST returns, TDS returns, Income tax return disclosures. Any mismatch may trigger notices.

- Deduction Claims: Deduction claims should be supported by Proper invoices, Agreements, Audit reports, Eligibility documentation

Incorrect deduction claims may result in disallowances and penalties.

TDS Reconciliation: Cross-check tax credits with Form 26AS, AIS and TIS. Mismatched TDS claims are one of the most common reasons for processing adjustments.

Correct Return Form: Companies must file ITR-6 and LLPs must file ITR-5 and Wrong selection of return form may invalidate the filing.

Important Updates for AY 2026-27

- Capital Gains Reporting Changes: Capital gains must now be reported separately for transactions undertaken Before 23 July 2024 and On or after 23 July 2024. This change has been introduced due to amendments in capital gains taxation provisions.

- TDS Disclosure Enhancements: Taxpayers are now required to disclose Applicable TDS section codes and Nature of TDS claims. This aims to improve reconciliation and reduce mismatches.

- Additional Reporting Requirements: Enhanced disclosures have been introduced for home loan interest claimed under Section 24(b), Deductions and Exemptions and Specific Tax Regimes

- New Presumptive Taxation Provisions: The return incorporates provisions relating to:

- Section 44BBC: Presumptive taxation for cruise business operators.

- Presumptive Scheme for Certain Diamond Traders: Eligible businesses may compute income at 4% of gross receipts subject to prescribed conditions.

Conclusion

ITR-6 filing is a crucial annual compliance responsibility for companies operating in India. Since the form requires extensive financial disclosures, tax computations, reconciliations, and regulatory reporting, businesses should begin preparation well in advance of the due date. Accurate reporting, timely filing, proper reconciliation of tax credits, and maintenance of documentation can help companies:

- Avoid penalties and notices

- Reduce litigation risks

- Ensure smooth assessments

- Strengthen tax compliance

- Improve corporate governance standards

Given the complexities involved in corporate taxation and continuous regulatory changes, companies should carefully review disclosures, reconcile financial records, and seek professional guidance wherever required to ensure error-free filing of ITR-6 for AY 2026-27