Table of Contents

Explained Simply: Form 10-IEA Requirement at a Glance

This blog explains when Form 10-IEA is required for taxpayers having business or professional income who wish to opt out of the new tax regime and switch to the old tax regime (OTR).

We have to understand the Important Rule for Form 10-IEA

Meaning of Terms

- OTR (Old Tax Regime)—Taxpayer claims deductions and exemptions such as Section 80C, Section 80D, HRA, Home Loan Interest, etc.

- NTR (New Tax Regime) – Lower tax rates with limited deductions/exemptions.

- Form 10-IEA – The prescribed form to exercise the option of switching from the New Tax Regime to the Old Tax Regime in specified cases.

For salaried taxpayers (no business income): No Form 10-IEA is generally required merely to choose between old and new tax regimes every year. The tax regime can be changed annually while filing the ITR.

For Business/Professional Taxpayers: Switching between regimes is restricted. Form 10-IEA becomes important when opting out of the New Tax Regime.

Form 10-IEA is required when: business or professional income exists (ITR-3/ITR-4 cases); the taxpayer wants to move from New Tax Regime to the old tax regime; or the option is being exercised for the first time after being covered by Section 115BAC.

Form 10-IEA is Not Required When: the taxpayer has only salary income and files ITR-1 or ITR-2, the taxpayer continues under the New Tax Regime, The Old Tax Regime option has already been validly exercised and continues without change.

For taxpayers having business or professional income, the choice of tax regime is not freely changeable every year. Therefore, before filing Form 10-IEA, evaluate the long-term tax impact, as opting out of the New Tax Regime may restrict future switching options u/s 115BAC.

Understanding the few Cases via example are explained here under

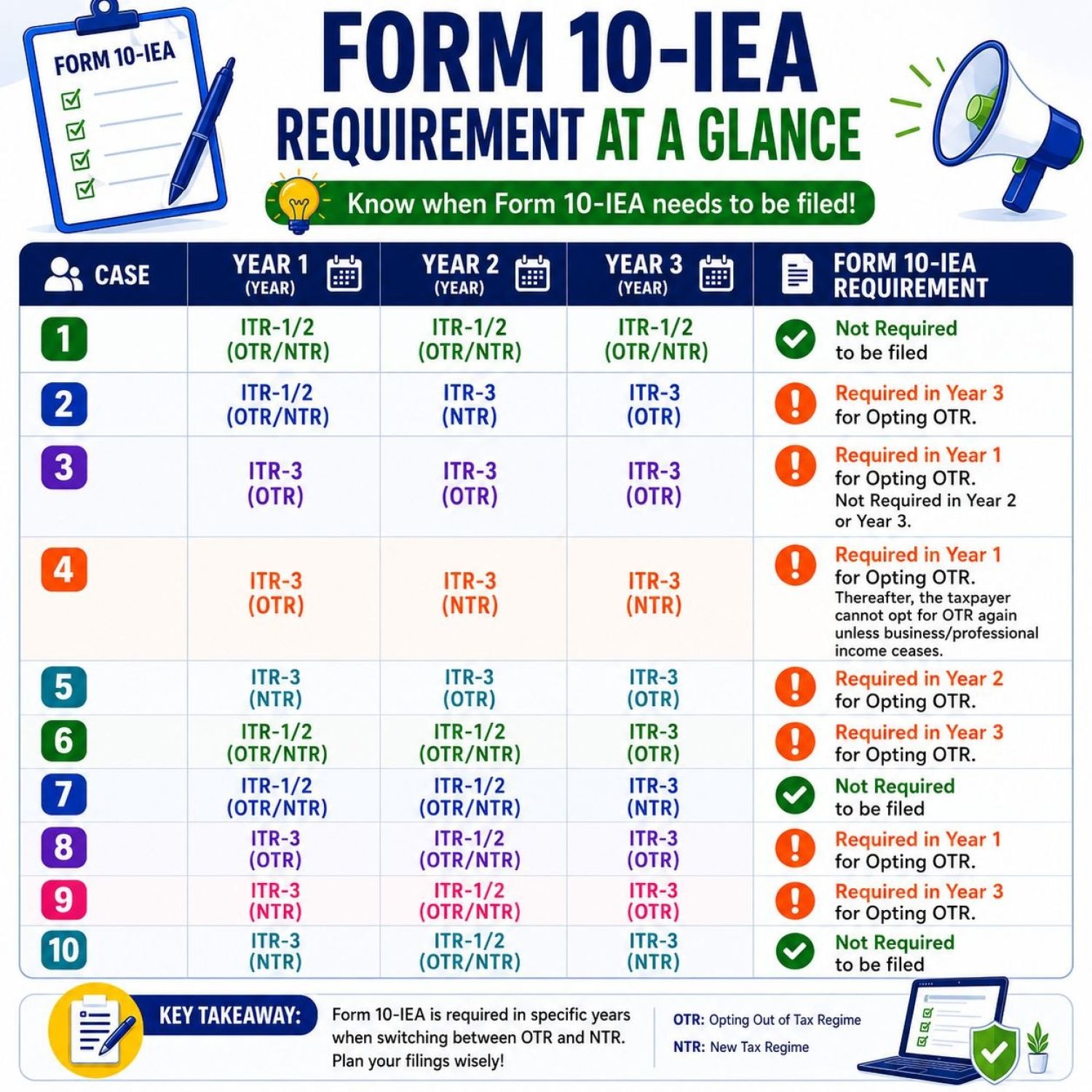

Case 1

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-1/2 |

ITR-1/2 |

ITR-1/2 |

- Form 10-IEA: Not Required. The taxpayer is filing ITR-1 or ITR-2 in all three years, which generally indicates that there is no business or professional income. Such taxpayers are permitted to choose between the Old Tax Regime (OTR) and the New Tax Regime (NTR) every year while filing their Income-tax Return.

- Since the taxpayer does not have business or professional income, the restrictions relating to switching between tax regimes under Section 115BAC do not apply. Therefore, there is no requirement to file Form 10-IEA for opting for either the Old Tax Regime or the New Tax Regime

Case 2

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-1/2 |

ITR-3 (NTR) |

ITR-3 (OTR) |

- Form 10-IEA: Required in Year 3. The Reason of this case is In Year 1, the taxpayer files ITR-1/ITR-2, indicating that there is no business or professional income. In Year 2, the taxpayer starts earning business or professional income and files ITR-3 under the New Tax Regime (NTR). In Year 3, the taxpayer wishes to switch from the New Tax Regime (NTR) to the Old Tax Regime (OTR) while continuing to have business or professional income and filing ITR-3.

- Since taxpayers having business or professional income are subject to special provisions under Section 115BAC, they cannot freely switch between tax regimes every year. Therefore, to opt out of the New Tax Regime and choose the Old Tax Regime, the taxpayer must file Form 10-IEA on or before the due date prescribed for filing the return.

- Whenever a taxpayer having business or professional income wishes to switch from the New Tax Regime to the Old Tax Regime, Form 10-IEA must be filed. Merely selecting the Old Tax Regime in the ITR is not sufficient.

Case 3

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-3 (OTR) |

ITR-3 (OTR) |

ITR-3 (OTR) |

- Form 10-IEA: Required Only in Year 1. The reason of this case. The taxpayer has business or professional income in all three years and files ITR-3.

- In Year 1, the taxpayer opts for the Old Tax Regime (OTR) by exercising the option to opt out of the default New Tax Regime through Form 10-IEA. Once this option is validly exercised and the taxpayer continues under the Old Tax Regime in subsequent years, there is no requirement to file Form 10-IEA again every year

Case 4

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-3 (OTR) |

ITR-3 (NTR) |

ITR-3 (NTR) |

- Form 10-IEA: Required in Year 1. The reason of this case reason. The taxpayer has business or professional income throughout the three years and files ITR-3 in each year.

- In Year 1, the taxpayer opts for the Old Tax Regime (OTR). Since the New Tax Regime is the default regime under Section 115BAC, the taxpayer is required to file Form 10-IEA to exercise the option of being taxed under the Old Tax Regime.

- In Year 2, the taxpayer decides to shift to the New Tax Regime (NTR). Once a taxpayer having business or professional income withdraws the option and moves to the New Tax Regime, the option to revert to the Old Tax Regime is generally lost. The taxpayer continues under the New Tax Regime in Year 3.

- For taxpayers having business or professional income, the option to opt out of the New Tax Regime and choose the Old Tax Regime can generally be exercised only once.

- Therefore, after opting for the Old Tax Regime and subsequently shifting back to the New Tax Regime, the taxpayer cannot ordinarily return to the Old Tax Regime in future years, unless the business or professional income ceases and the restrictions under Section 115BAC no longer apply.

- Form 10-IEA is required in Year 1 for opting for the Old Tax Regime. After shifting from the Old Tax Regime to the New Tax Regime, a taxpayer having business/professional income generally loses the option to switch back to the Old Tax Regime. Hence, taxpayers with business or professional income should carefully evaluate the long-term tax implications before changing their tax regime.

Case 5

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-3 (NTR) |

ITR-3 (OTR) |

ITR-3 (OTR) |

- Form 10-IEA: Required in Year 2. The Reason in this case, The taxpayer has business or professional income in all three years and files ITR-3 throughout.

- In Year 1, the taxpayer continues under the New Tax Regime (NTR), which is the default tax regime under Section 115BAC. Therefore, no Form 10-IEA is required.

- In Year 2, the taxpayer decides to move from the New Tax Regime to the Old Tax Regime (OTR) in order to claim deductions and exemptions available under the Income-tax Act, such as deductions under Sections 80C, 80D, interest on housing loan, etc. Since the taxpayer has business or professional income and is opting out of the default New Tax Regime, Form 10-IEA must be filed before the due date of filing the return.

- In Year 3, the taxpayer continues under the Old Tax Regime. As the option has already been exercised in Year 2, there is no requirement to file Form 10-IEA again.

Case 6

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-1/2 |

ITR-1/2 |

ITR-3 (OTR) |

- Form 10-IEA: Required in Year 3. The Reason of this case are mention here under:

- In Year 1 and Year 2, the taxpayer files ITR-1 or ITR-2, indicating that there is no business or professional income. During these years, the taxpayer is free to choose between the Old Tax Regime and the New Tax Regime every year without filing Form 10-IEA.

- In Year 3, the taxpayer starts earning business or professional income and therefore files ITR-3. At the same time, the taxpayer wishes to be taxed under the Old Tax Regime (OTR) and avail deductions and exemptions available under the Income-tax Act.

- Since the taxpayer now has business or professional income and is opting for the Old Tax Regime, Form 10-IEA must be filed in Year 3 before the due date prescribed for filing the return.

- No Form 10-IEA is required as long as the taxpayer files ITR-1/ITR-2 and does not have business or professional income.

- Once business or professional income begins and the taxpayer wants to opt for the Old Tax Regime, Form 10-IEA becomes mandatory.

- The requirement arises not merely because ITR-3 is filed, but because the taxpayer with business/professional income is choosing to be taxed under the Old Tax Regime.

Case 7

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-1/2 |

ITR-1/2 |

ITR-3 (NTR) |

Form 10-IEA: Not Required. The reason for this case.

In Year 1 and Year 2, the taxpayer files ITR-1/ITR-2, indicating there is no business or professional income.

In Year 3, the taxpayer starts earning business or professional income and files ITR-3. However, the taxpayer continues under the New Tax Regime (NTR), which is the default tax regime under Section 115BAC.

Since Form 10-IEA is primarily required when a taxpayer having business or professional income wishes to opt out of the New Tax Regime and choose the Old Tax Regime, no such form is required when the taxpayer continues under the New Tax Regime.

- Merely starting a business or professional activity and filing ITR-3 does not trigger the requirement to file Form 10-IEA.

- Form 10-IEA becomes relevant only when a taxpayer having business/professional income wishes to opt for the Old Tax Regime.

- If the taxpayer continues under the New Tax Regime, Form 10-IEA is not required, irrespective of whether business income has commenced.

Case 8

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-3 (OTR) |

ITR-1/2 |

ITR-3 (OTR) |

- Form 10-IEA: Required in Year 1. This is Reason of this case.

- In Year 1, the taxpayer has business or professional income and files ITR-3 under the Old Tax Regime (OTR). Therefore, the taxpayer is required to file Form 10-IEA to exercise the option of opting out of the default New Tax Regime.

- In Year 2, the taxpayer files ITR-1/ITR-2, indicating that there is no business or professional income during that year. The taxpayer may have only salary, house property, capital gains, or other non-business income.

- In Year 3, business or professional income resumes and the taxpayer again files ITR-3 under the Old Tax Regime. Since the option to opt for the Old Tax Regime was already exercised in Year 1 through Form 10-IEA and there has been no switch to the New Tax Regime while having business income, a fresh Form 10-IEA is generally not required.

- Form 10-IEA was required only in Year 1 when the option for the Old Tax Regime was initially exercised.

- Initial filing of Form 10-IEA in Year 1 remains valid. A year without business/professional income does not by itself necessitate filing a fresh Form 10-IEA when business income resumes. Since the taxpayer continues under the Old Tax Regime and has not opted for the New Tax Regime during the business-income years, Form 10-IEA is required only once, i.e., in Year 1.

Case 9

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-3 (NTR) |

ITR-1/2 |

ITR-3 (OTR) |

- Form 10-IEA: Required in Year 3. The Reason of this case explain here under :

- In Year 1, the taxpayer has business or professional income and files ITR-3 under the New Tax Regime (NTR). Since the New Tax Regime is the default regime, no Form 10-IEA is required.

- In Year 2, the taxpayer files ITR-1/ITR-2, indicating that there is no business or professional income during the year. The taxpayer may have only salary income, house property income, capital gains, or other non-business income.

- In Year 3, business or professional income resumes and the taxpayer files ITR-3. The taxpayer now wishes to opt for the Old Tax Regime (OTR) to avail deductions and exemptions available under the Income-tax Act.

- Since this is the first year in which the taxpayer, while having business/professional income, is opting out of the default New Tax Regime and choosing the Old Tax Regime, Form 10-IEA must be filed in Year 3.

- Form 10-IEA is required in Year 3 before filing the return of income.

- No Form 10-IEA is required when the taxpayer with business income remains under the New Tax Regime. A year without business/professional income does not amount to exercising the option for the Old Tax Regime. When business income returns and the taxpayer wishes to shift from the New Tax Regime to the Old Tax Regime, Form 10-IEA becomes mandatory in the year of such switch. Therefore, in this case, Form 10-IEA is required in Year 3 because the taxpayer is opting for the Old Tax Regime after business/professional income resumes.

Case 10

|

Year 1 |

Year 2 |

Year 3 |

|

ITR-3 (NTR) |

ITR-1/2 |

ITR-3 (NTR) |

- Form 10-IEA: Not Required. Under reason of this case explain here under.

- In Year 1, the taxpayer has business or professional income and files ITR-3 under the New Tax Regime (NTR). Since the New Tax Regime is the default tax regime, filing of Form 10-IEA is not required.

- In Year 2, the taxpayer files ITR-1/ITR-2, indicating that there is no business or professional income during the year. The taxpayer may have only salary, house property, capital gains, or other non-business income.

- In Year 3, business or professional income resumes and the taxpayer files ITR-3. However, the taxpayer continues under the New Tax Regime (NTR) and does not seek to opt for the Old Tax Regime.

- Since Form 10-IEA is required only when a taxpayer having business or professional income intends to opt out of the default New Tax Regime and choose the Old Tax Regime, there is no requirement to file Form 10-IEA in this case.

- No Form 10-IEA is required in any of the years because the taxpayer never opts for the Old Tax Regime.

- The New Tax Regime is the default regime for taxpayers having business or professional income. Merely moving from ITR-1/ITR-2 to ITR-3 does not trigger Form 10-IEA compliance. Form 10-IEA becomes relevant only when the taxpayer wishes to opt for the Old Tax Regime. Where the taxpayer continues under the New Tax Regime throughout, Form 10-IEA is not required, regardless of whether business/professional income exists or resumes in a later year.