Table of Contents

- Icai: Widening Scope Of Mandatory Applicability Of Aqmm V2.0

- Revised Applicability Of Aqmm V 2.0: Three Categories Of Practice Units:

- Key Takeaways For Chartered Accountants Audit firms

- Why This Applicability Of Audit Quality Maturity Model (aqmm V2.0) Matters :

- Mandatory Applicability Of Audit Quality Maturity Model (aqmm V2.0) Is Not Covered:

- Conclusion

ICAI: Widening Scope of Mandatory Applicability of AQMM v2.0

The Institute of Chartered Accountants of India has issued an important update expanding the scope of mandatory applicability of the Audit Quality Maturity Model (AQMM) Version 2.0. Previously, the Audit Quality Maturity Model (AQMM v2.0) was mandatory only for firms (practice units) auditing listed entities, banks (other than cooperative banks, except multi-state cooperative banks), and insurance companies. Branch auditors (practice units) were excluded. The Institute of Chartered Accountants of India has now widened the mandatory applicability of the Audit Quality Maturity Model (AQMM v2.0) to cover more categories of Chartered Accountants firms in a phased manner. This announcement partially modifies the earlier clarification dated 11 August 2025.

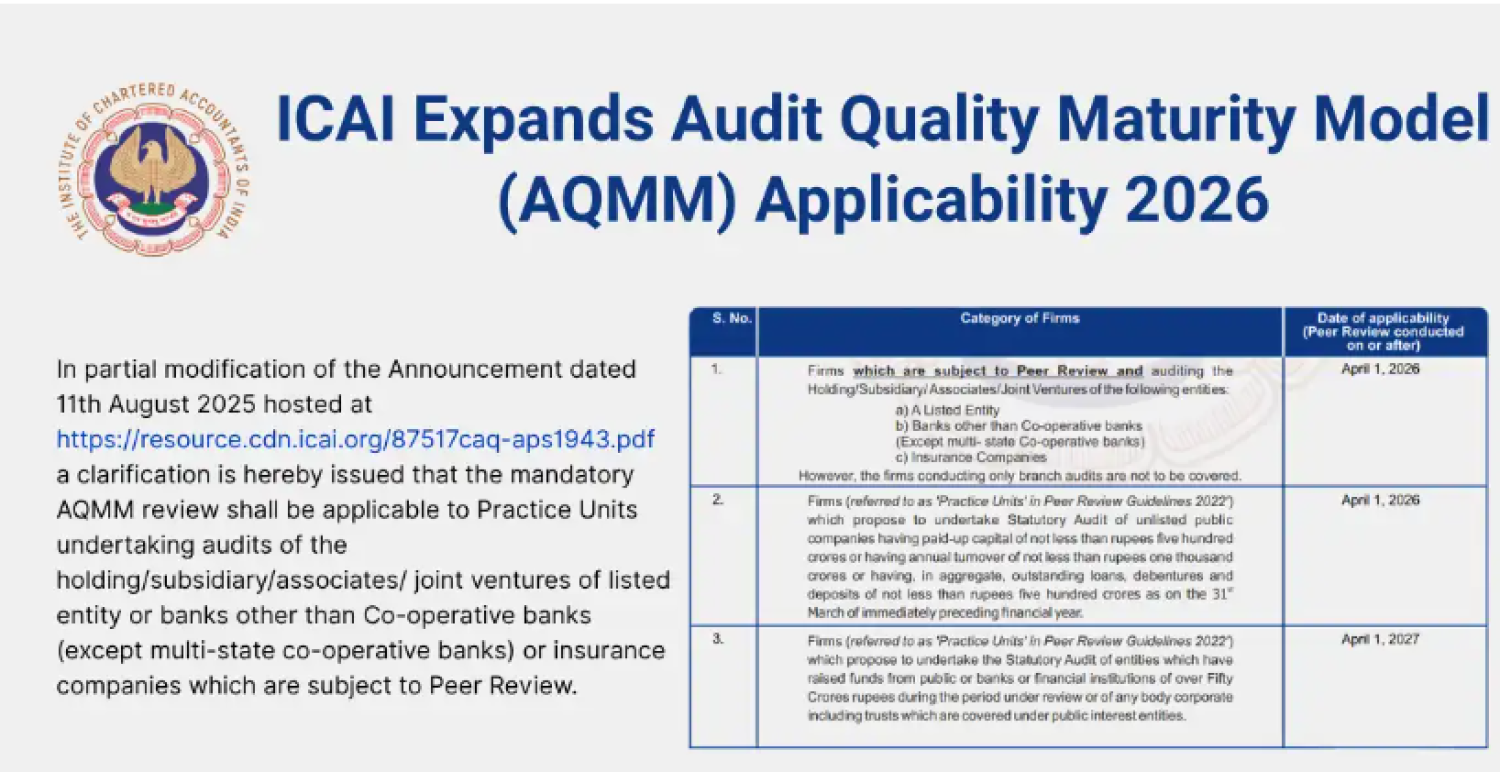

Revised applicability of AQMM v 2.0: three categories of practice units:

The revised applicability now includes three categories:

- Category 1 (Effective: Peer Review conducted on or after 1 April 2026) : Chartered Accountant Firms (Practice Units) subject to Peer Review and undertaking audits of Holding companies, subsidiaries, associates, or joint ventures of Listed entities; Banks (other than co‑operative banks, except multi‑state co‑operative banks); and Insurance companies. Branch audit–only firms remain excluded. (Reference:)

- Category 2 (Effective: Peer Review conducted on or after 1 April 2026) : Chartered Accountants Firms (Practice Units) proposing to undertake statutory audits of large unlisted public companies, defined as those meeting any of the following thresholds Paid‑up capital ≥ INR 500 crore, Annual turnover ≥ INR 1,000 crore and Total outstanding loans, debentures, and deposits ≥ INR 500 crore (as on 31 March of the preceding financial year) (Reference:)

- Category 3 (Effective: Peer Review conducted on or after 1 April 2027) : Chartered Accountants Firms (Practice Units) proposing to undertake statutory audits of Entities that have raised public or bank/financial institution funds exceeding INR 50 crore during the period under review OR Anybody corporate (including trusts) falling under the definition of Public Interest Entities (PIEs) (Reference:)

Key Takeaways for Chartered Accountants Audit Firms

- Mandatory Audit Quality Maturity Model (AQMM) adoption significantly expanded: Firms (Practice Units) auditing even related entities (holding/subsidiary/JV/associate) of listed/banking/insurance companies now fall under mandatory coverage.

- Large unlisted companies now within scope: This brings chartered accountants' audit firms (practice units) serving major unlisted public companies into mandatory Audit Quality Maturity Model (AQMM) compliance.

- Publicly funded entities included the following: From April 2027, firms auditing entities raising funds >INR 50 crore or other PIEs will need Audit Quality Maturity Model (AQMM) compliance.

- Alignment with Peer Review timelines: Applicability is linked directly to Peer Review cycles, ensuring structured phase‑in.

Why This Applicability of Audit Quality Maturity Model (AQMM v2.0) Matters :

The Audit Quality Maturity Model (AQMM v2.0) evaluates the maturity of quality processes in audit-chartered accountant firms. And mandatory application for a wider set of chartered accountant firms (practice units) means Higher quality and documentation standards, greater regulatory oversight, and stronger public trust in audits and chartered accountant firms (practice units) must begin preparation well before their peer review cycle. Categories Live Now Categories 1 & 2 are already mandatory from April 1, 2026.

-

INR 500 Cr Capital / Debt Threshold: Requirement for Category 2 firms auditing unlisted public companies.

-

INR 1,000 Cr Turnover Threshold: Annual turnover trigger for Category 2 applicability.

-

April 1, 2027 – Category 3 Deadline: CA firms auditing PIEs or entities with >INR 50 crore in fundraising have until April 2027.

Mandatory Applicability of Audit Quality Maturity Model (AQMM v2.0) Is NOT Covered:

Applicability is triggered by the relationship of the entity with the listed parent, not by whether the audited entity is listed. Branch auditors are expressly excluded across all categories. It refers to firms falling under the Peer Review Guidelines 2022, i.e., those required or assigned to undergo peer review. PIEs fall under Category 3, mandatory from April 1, 2027. It is a partial modification. Category 1 has been newly added, and applicability dates have been revised. Chartered Accountant Firms (Practice Units) conducting only branch audits remain excluded.

-

Branch Auditors: Firms conducting only branch audits (even of banks, insurers, and listed companies) are explicitly excluded across all categories.

-

Co‑operative Banks: All co‑operative banks remain excluded except multi‑state co‑operative banks, which are included.

Conclusion

The Institute of Chartered Accountants of India clarification brings definitive guidance on the mandatory adoption of AQMM 2.0, representing a major shift in India’s audit quality regime. Peer‑reviewed firms must now proactively strengthen systems, controls, and documentation to comply with the enhanced framework. CA Audit Firms Should now begin internal readiness assessments, map existing quality management systems against AQMM 2.0 requirements, and train audit teams on updated expectations. Prepare documentation and evidence for peer review and implement corrective and preventive measures well before April 2026. AQMM 2.0 evaluates firms on parameters such as leadership responsibilities, risk assessment, human resource policies, engagement performance, and monitoring mechanisms.