Table of Contents

Review Procedures and Reporting by Peer Reviewer & Importance of AQMM in Peer Review

Peer Review – A Tool to Improve Quality

Peer review is a cornerstone initiative of the Institute of Chartered Accountants of India (ICAI) aimed at enhancing the quality and reliability of professional services rendered by Chartered Accountants. It involves the independent evaluation of a professional's work by fellow members of the profession, ensuring adherence to prescribed standards and fostering a culture of continuous improvement.

Role of the Peer Review Board

To ensure the effective implementation of the peer review mechanism, ICAI has constituted the Peer Review Board (PRB). The PRB is entrusted with:

-

Overseeing the peer review framework,

-

Selecting practice units for review,

-

Assigning qualified peer reviewers,

-

Evaluating peer review reports, and

-

Recommending corrective actions where required.

Summary on Review Procedures and Reporting by Peer Reviewer and the Importance of AQMM in Peer Review, based on the document provided from the ICAI's Peer Review manual

1. Review Procedures by Peer Reviewer—Key Objectives and Coverage

Peer Review is a structured process that ensures compliance with assurance, quality, and ethical standards. The procedures involve both off-site and on-site components. Peer Review is not an audit but a quality assurance mechanism aimed at:

- Evaluating the design and effectiveness of systems and procedures adopted by CA firms.

- Ensuring compliance with technical, ethical, and professional standards.

- Improving the overall quality of assurance services.

- Governed by Peer Review Guidelines 2022. Mandatory for various classes of Practice Units (PUs), including firms auditing listed entities, banks, and insurance companies.

II. Review Procedures by Peer Reviewer (RE)

A. Pre-Visit & Off-Site Review

Off-site Procedures

- Evaluation of Form 1:

- Includes the Application and Questionnaire (Parts A, B, C).

- Part A: Profile of the Practice Unit (PU) with Annexures listing assurance services.

- Part B: Based on SQC 1, covering quality control aspects (leadership, ethics, HR, client acceptance, etc.).

- Part C: Audit Quality Maturity Model (AQMM) self-evaluation scores.

- Initial Steps:

- Reviewer sends Form 6 to seek additional information if needed.

- Reviewer issues Form 5 to notify about sample selection and proposed dates of visit.

- Reviewer researches PU’s public presence (website, social media) to validate compliance and activities.

B. On-site Procedures- On-Site Review (Up to 6 Days)

- Day 1 Visit:

- Verification of documentation for assurance engagements.

- Interaction with audit staff and article assistants.

- Review of internal records, quality control documentation, and infrastructure.

- Day 1: Office inspection, discussion with team, document verification.

- Day 2-5: Sample file reviews, compliance with standards, human resource records, internal controls.

- Day 6: Finalization of observations, scoring, and documentation.

- Form 1 Review: Includes firm profile, SQC 1 compliance, and AQMM scores.

- Form 5: Reviewer informs PU about sample selection and proposed visit.

- Form 6: Used to seek additional information.

- Review public domain presence (PU website, regulatory reports, etc.).

III. Reporting by Peer Reviewer

Reporting by Peer Reviewer

- Form 9 is used for final submission of the Peer Review Report by the Reviewer to the Peer Review Board (PRB).

- Must include a compliance checklist and supporting annexures.

- Reviewer must maintain confidentiality and adhere to the declaration signed via Form 2.

- Gross negligence, such as breach of confidentiality or bias, can lead to disqualification of the reviewer.

- Key Documents:

- Form 9: Final report submission along with:

- Annexure I (Engagements, sample selection)

- Annexure II (Observations on systems, procedures)

- Annexure III (AQMM Score Evaluation)

- MRL (Management Representation Letter) if needed.

- All documentation must be retained for minimum 18 months.

- Form 9: Final report submission along with:

Types of Reports:

- Clean Report

- Qualified Report (if deficiencies not rectified)

- Preliminary Report (if major issues found during review)

IV. Importance of AQMM (Audit Quality Maturity Model) in Peer Review

AQMM plays a critical role in evaluating a firm’s audit quality maturity. It is part of Part C of Form 1 and assesses the following dimensions:

What is the Audit Quality Maturity Model ?

The Audit Quality Maturity Model is a self-evaluation tool developed by ICAI to assess and enhance audit quality maturity levels of firms.

AQMM Levels

AQMM Sections and Scoring

- Section 1 – Practice Management Operations (Max: 280 points)

- Section 2 – Human Resources Management (Max: 240 points)

- Section 3 – Strategic/Functional Management (Max: 80 points)

- Total Score: 600 points

|

Score per Section |

Level |

Interpretation |

|---|---|---|

|

Up to 25% |

Level 1 |

Nascent firm needing improvement |

|

25%-50% |

Level 2 |

Some progress, needs tuning |

|

50%-75% |

Level 3 |

Substantial progress |

|

75%+ |

Level 4 |

Mature audit quality controls |

Note: The lowest scoring section determines the overall level.

Scoring Framework (Total: 600 points)

|

Section |

Area |

Max Score |

% |

|---|---|---|---|

|

1 |

Practice Management - Operations |

280 |

46.67% |

|

2 |

Human Resources Management |

240 |

40.00% |

|

3 |

Strategic/Functional Management |

80 |

13.33% |

Why AQMM Matters

- Encourages continuous improvement in audit quality.

- Helps assess readiness and maturity in delivering assurance services.

- Adds objectivity to Peer Review via a scoring mechanism.

- Directly linked to compliance with technical, ethical, and professional standards.

Why AQMM is Crucial

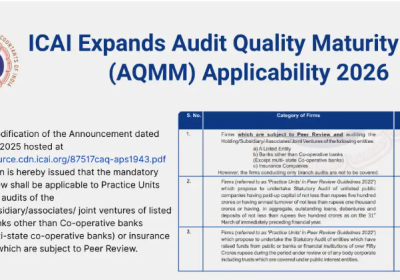

- Mandatory from 1st April 2023 for firms auditing:

- Listed entities

- Banks (excluding co-op/multi-state co-op)

- Insurance companies

- Helps reviewers assess:

- Operational efficiency

- Use of technology

- Staff training & infrastructure

- Provides basis for recommendations to improve audit quality and firm maturity.

What Peer Review Is Not

- Not an audit or investigation.

- Not meant for fault-finding.

- Not a full review of all engagements—only selected samples.

- Not for client interaction or document collection from clients.

Significance and Benefits

The peer review mechanism provides multiple benefits:

-

Enhancement of quality in professional services,

-

Early identification of gaps in compliance and systems,

-

Opportunity for self-improvement and learning,

-

Boosts client confidence by reinforcing commitment to quality,

-

Upholds ICAI’s reputation and ensures consistency in professional practices.

Conclusion

The Peer Review Program of ICAI is a robust quality assurance tool that reinforces professional excellence among Chartered Accountants. It fosters transparency, accountability, and continuous development in the profession. By embracing the peer review process, practitioners not only align with ICAI’s standards but also contribute to the collective integrity and credibility of the accounting fraternity in India. The Peer Review process is systematic and comprises the following steps:

-

Selection of Practice Units

Firms or individuals are selected for peer review based on parameters such as size, complexity, and nature of services rendered (especially attest functions). -

Appointment of Peer Reviewer

A qualified and empanelled peer reviewer is assigned to conduct the review of the selected practice unit. -

On-site Review

The peer reviewer visits the office of the practice unit to examine:-

Internal control systems and quality control policies,

-

Compliance with professional standards,

-

Documentation and execution of attest functions,

-

Client files and other relevant records.

-

-

Reporting and Feedback

Following the visit, the peer reviewer submits a detailed report highlighting:-

Observations,

-

Areas of improvement,

-

Recommendations for remedial actions (if any).

The PRB reviews this report and may direct the practice unit to take corrective measures if deviations from prescribed standards are observed.

-

The Peer Review process is both evaluative and developmental. The peer review process, strengthened by AQMM, is a proactive quality enhancement tool. While the reviewer ensures the PU is compliant, the process also encourages better practices through AQMM. Documentation, transparency, and following ICAI guidelines are critical for a smooth review process and favorable outcome. It helps firms benchmark against best practices and provides the ICAI with insights into the maturity and preparedness of its members.