Table of Contents

- Complete Overview Peer Review Process

- Purpose Of The Peer Review Process

- Objectives Of Peer Review

- Peer Review Process Overview

- Overview On Classification & Applicability Of Peer Review

- Stage I: Planning Stage :

- Stage Ii: Execution Stage :

- Stage Iii: Reporting Stage :

- Documents To Be Submitted By The Reviewer Post-completion:

- Consequences For Level-i Pu Not Applying For Peer Review

- Conclusion:

Complete Overview Peer Review Process

Purpose of the Peer Review Process

The peer review process is a quality assurance initiative undertaken by ICAI to maintain and enhance the quality of assurance services provided by chartered accountants. It ensures that firms adhere to technical, professional, and ethical standards.

Objectives of Peer Review

- Ensure Compliance: Verify whether the firm has complied with applicable accounting, auditing, and other professional standards.

- Promote Quality: Encourage and promote quality in the performance of assurance services.

- System Review: Evaluate the quality control systems established by the firm.

- Guidance and Education: Provide constructive feedback and suggestions for improvement.

- The process is governed by: Statement on Peer Review (Revised) issued by ICAI. And Provisions of the Chartered Accountants Act, 1949, and regulations framed thereunder.

Who is covered under Peer Review : The following firms are mandatorily subject to peer review:

- Auditors of listed entities.

- Firms undertaking audits of large entities such as:

- Banks, insurance companies, and NBFCs.

- Entities with net worth or turnover above a threshold prescribed by ICAI.

- Firms issuing certificates under various statutory provisions.

Others may voluntarily opt for peer review to showcase their commitment to quality.

Peer Review Process Overview

- Application / Selection: Firms apply or are selected based on ICAI criteria.

- Appointment of Reviewer: A trained and empaneled peer reviewer is appointed.

- Execution of Review: The reviewer examines the firm's systems, documentation, procedures, and a sample of assurance engagements.

- Reviewer’s Report: A report is submitted to the Peer Review Board. Give Final Decision about firm and Based on the findings, ICAI may Issue a clean report or Suggest improvements or Recommend corrective actions.

- Peer Review is conducted once every three years (revised norms may change this based on risk and size). Firms with major non-compliances may be subject to follow-up reviews.

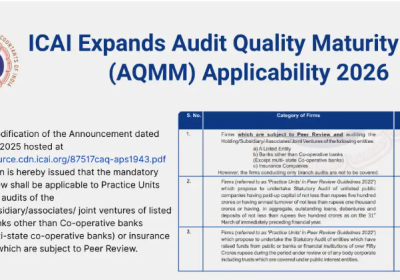

Overview on Classification & Applicability of Peer Review

Level I PUs – Mandatory Peer Review Once Every 3 Years : These include PUs that conduct Central statutory audits of banks, public financial institutions, insurance companies, PSUs, listed entities, large fund-raising entities (₹50 crore+), or entities with ₹500 crore+ net worth, etc.

Level II PUs – Peer Review Every 4 Years: These include:

- Statutory/Internal/Concurrent/System/Tax audits of bank branches, RRBs, NBFCs.

- Audit of entities with net worth > ₹5 crore or turnover > ₹50 crore.

- Other assurance services not covered under Level I.

Level III PUs – Peer Review Every 5 Years : These are residual PUs providing limited assurance services not covered under Level I or II. Voluntary Peer Review:

- A PU not selected for review may apply suo moto to the Board.

- A client (auditee) may also request a peer review of its auditor.

- Both requests must be acted upon within 30 days by the Board.

Dynamic Movement Between Levels: If a PU moves up to Level I (e.g., secures audit of a listed company), it must undergo peer review once every 3 years from that point. The PU must inform the Peer Review Board of this change. Peer Review process conducted by the Peer Review Board of ICAI. The Peer Review process conducted by the Peer Review Board of ICAI is designed to ensure quality assurance in the work of Chartered Accountants. This process is conducted in three main stages:

Stage I: Planning Stage :

This is the preparatory phase, involving identification, assignment, and preliminary exchange of information.

Key Steps taken by Peer Reviewer :

- Application Submission: The Practice Unit (PU) submits a Declaration/Application form for voluntary Peer Review.

- Peer Reviewer Panel Formation: The Board maintains a city-wise panel of trained reviewers. Three names are provided to the PU, who selects one reviewer.

- Appointment & Acceptance:

- The Board issues a Letter of Appointment to the selected reviewer.

- Reviewer submits Acceptance & Declaration of Confidentiality.

- Reviewer may take assistance of one qualified assistant, whose confidentiality declaration is also required.

- Initial Documents Shared: PU sends duly filled Questionnaire for the relevant 3-year period directly to the Reviewer. Reviewer uses this to select the sample of assurance engagements.

- Timelines: The entire Peer Review process is to be completed in 90 days.

Stage II: Execution Stage :

This involves the actual on-site review, system understanding, and sampling for evaluation.

Key Steps:

- On-site Visit: Conducted by mutual consent; should not exceed 7 working days.

- Initial Meeting: Reviewer verifies questionnaire responses. Gains understanding of internal controls and systems of the PU.

- Compliance Review of 5 General Controls:

- Independence

- Maintenance of professional skills

- Outside consultation

- Staff supervision & development

- Office administration

- Sample Selection & Refinement:

- Based on the client list and questionnaire. Must include:

- Client with highest turnover

- At least one Public Ltd. Company (if available)

- At least one tender-based audit

- Variety of assurance services (e.g. Statutory, Internal, Tax, etc.)

- Based on the client list and questionnaire. Must include:

- Review Approach:

- Compliance Approach: Evaluate 6 key controls such as audit record management, internal control evaluation, audit conclusion, etc.

- Substantive Approach: Detailed review based on checklist from Peer Review Manual (para 4.19).

- Branch Offices: Branches with an assurance turnover of > ₹25 lakh must be visited. Others can be centrally reviewed at Head Office.

- Restrictions: Reviewer cannot visit or contact clients of PU. No extracts or copies from client files may be made.

Stage III: Reporting Stage :

This phase documents the findings and results in issuance of the Peer Review Certificate. Key Steps:

- Report Types:

- Clean Report: If no significant issues are found.

- Qualified Report: If major irregularities exist.

- Preliminary Report: If deficiencies require PU clarification.

- Practice Unit Response: PU must respond to preliminary report within 10 days.

- Final Report Submission : Reviewer discusses findings with PU. And Submits final report to the Peer Review Board after considering PU’s response.

- Board's Decision: If satisfied, Peer Review Certificate is issued. If not satisfied. Recommendations or Follow-up Review may be ordered (after 6 months or 1 year).

- Follow-up Reviews: Conducted by a different reviewer than the original one (for orders after April 2009). PU must pay fees to original reviewer if report was qualified.

Documents to be Submitted by the Reviewer Post-Completion:

- Final Report: Must be submitted using individual reviewer’s letterhead and stationery only. Should include Annexure I. Download format

- Annexure II (Mandatory for Level I & II firms only) : Download format

- List of Samples Selected : Must include:

- Basis of sample selection

- At least one sample of tendering services, if applicable

- Engagement with the highest turnover

- At least one Public Limited Company, if such an assignment exists

- Minimum Sample Size:

- Level 1: 08

- Level 2: 05

- Level 3: 03

- Newly established firms: Minimum 5 for 3-year validity; <5 leads to 1-year validity

- If the above minimum is not met, 100% selection is mandatory, and validity is limited to 1 year.

- Preliminary Report, if issued : Along with: PU’s point-wise response/submissions and Reviewer's comments/verification on PU’s responses

- Basis of Conclusion : Detailed justification for the opinion/conclusion reached in the Final Report.

- Completed Peer Review Questionnaire : As submitted by the PU. Download Questionnaire Reviewer must specifically address Parts B, questions 2(j) to 2(s) and provide PU’s explanations if those responses are affirmative.

- Submission Timelines : The Final Report and annexures should be submitted within 10 days of completion of the review (i.e., by Day 90 of the peer review schedule).

- Other Notes: A copy of the Final Report along with Annexure I & II must also be sent to the Practice Unit. Reasons for any delay in submission must be documented.

The Reviewer must not challenge Practice Unit’s professional judgment unless it clearly contradicts a technical standard. The Reviewer should ensure that the review process followed the Illustrative Time Schedule issued by the PRB. The Peer Review Certificate will be issued by PRB only after confirming receipt of Peer Review Fees and Board approval. The Peer Review process conducted by the Peer Review Board of ICAI is designed to ensure quality assurance in the work of Chartered Accountants.

Consequences for Level-I PU Not Applying for Peer Review

1. Mandatory Requirement Filing of declaration and undergoing Peer Review by Practice Units falling under Level-I is mandatory as per the Statement on Peer Review issued by the ICAI.

2. Non-Compliance is Misconduct : Non-compliance amounts to Professional Misconduct or Other Misconduct. Professional Misconduct as defined under Section 21 (Professional Misconduct) and Section 22 (Other Misconduct) of the Chartered Accountants Act, 1949. This could lead to disciplinary action by the ICAI, which may include inquiry, penalties, or suspension of practice.

Conclusion:

All PUs are not subjected to mandatory peer review immediately. Only those meeting the criteria under Level I, II, or III are covered in phased and periodic cycles. Others may undergo voluntary review or be reviewed upon client request or random selection by the Board. The Peer Review process is a significant initiative of ICAI to uphold the credibility and quality of the profession. It benefits not only regulators and users of financial statements but also enhances the professional stature of the practicing firm.