Table of Contents

Is ELSS Better Than PPF For My Tax Savings Goal?

The Annual Tax-Saving Dilemma

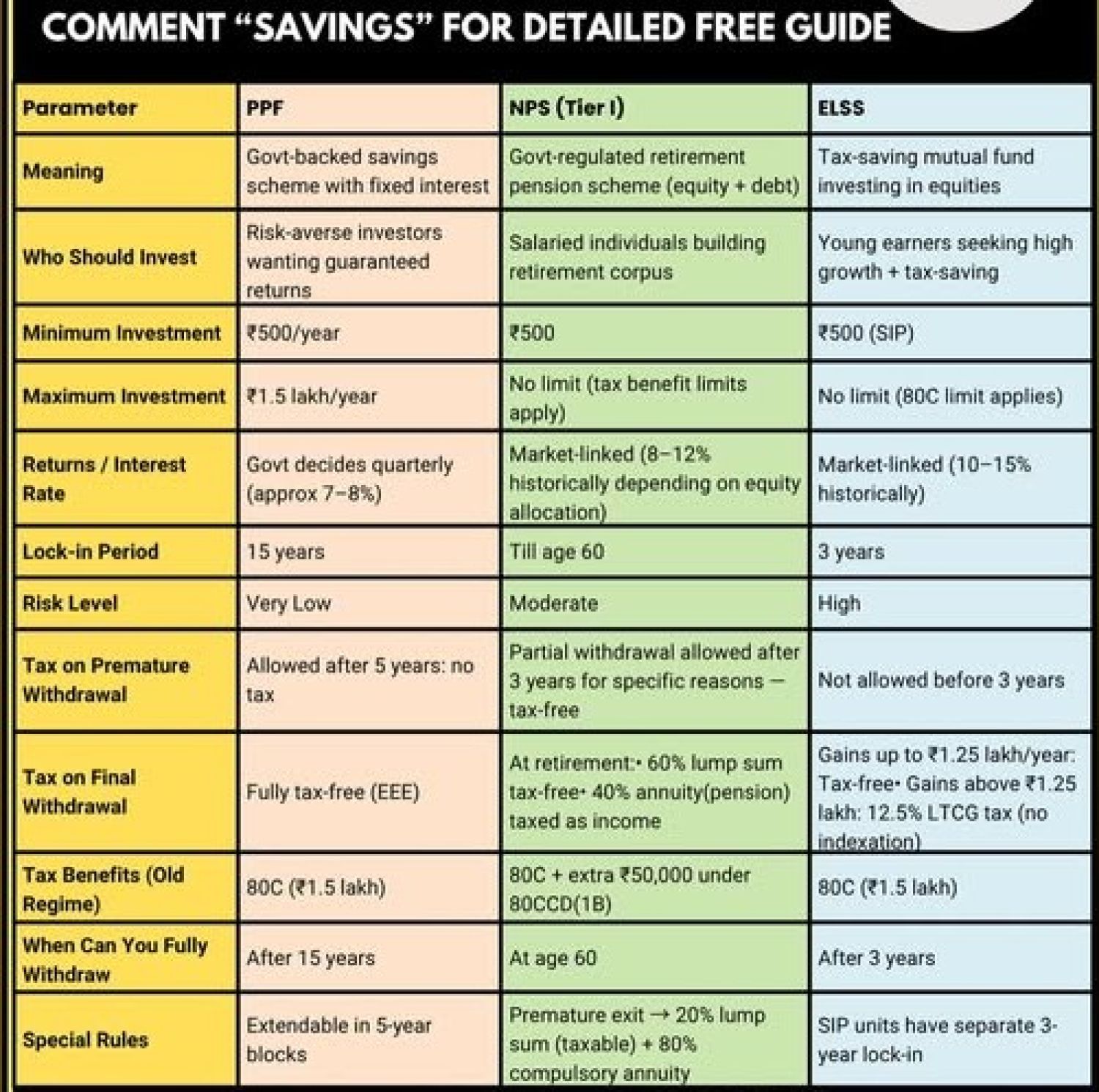

Every financial year, paid people and self employed workers face the same question when trying to claim expenses under Section 80C of the Income Tax Act. The Public Provident Fund and Equity Linked Savings Plans are the two choices that are most commonly compared. The similarities mostly stop there, but both permit a withdrawal of up to 1.5 lakh rupees every fiscal year. While elss mutual funds deal mostly in stock markets and have a far shorter lock-in time of only three years, PPF is a government-backed fixed income vehicle with a fifteen-year lock-in period. An individual's risk tolerance, business timeline, and financial goals all play a part in making the best choice. Although there isn't a single right answer, learning the trade-offs allows buyers to make a choice that truly fits their case.

Returns and Risk: The Core Difference

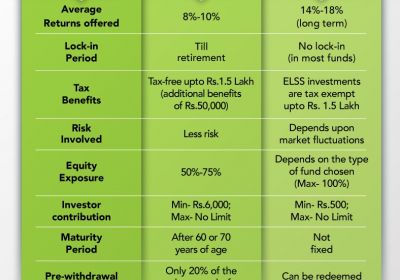

Currently, PPF gives a set interest rate that is changed by the government every three months. Conservative buyers find it appealing because it offers guaranteed gains with little exposure to market swings. But over the last ten years, PPF profits have been falling and frequently fall short of inflation by a large amount. In comparison, experienced fund managers handle ELSS funds, which invest across market capitalisations and actively choose stocks based on market potential and study. Although there is no guarantee of profits, well-managed ELSS funds have generally beaten PPF in terms of long-term financial prospects. The trade-off is clear. Each individual must choose where they fall on the range of greater chance and increased doubt.

Liquidity and Lock In Periods

The fact that ELSS has the shortest lock-in length of any Section 80C qualifying instrument—three years—is one of the best reasons in its favour. PPF locks money away for fifteen years, with partial withdrawal allowed only after the seventh year. The three-year lock-in of ELSS provides significantly more freedom for younger workers who might need access to their cash within a reasonable period. There is no escape load when the lock-in time ends, and units can be reclaimed without limit. This cash benefit is especially important for people who are just starting out financially and can face unexpected costs or possibilities that call for quick access to money.

Starting the Investment Journey

It's simple to get started with an Equity Linked Savings Scheme mutual fund investment. After finishing a one-time KYC verification, an investor can select between a lump amount donation and a regular investment plan. SIPs make it possible for people to begin with as little as 500 rupees per month, making them cheap even for those just starting out in their jobs. Platforms like Choice offer access to over two thousand five hundred fund schemes along with expert rated recommendations, goal specific planning tools, and comprehensive performance analysis. For both beginner and seasoned buyers, these tools simplify the choosing process.

So Which One Should Someone Choose?

To be honest, it depends. For someone who cannot take any risk and wants total capital safety, PPF remains a reasonable choice. However, the Equity Linked Savings Scheme offers an appealing mix of tax efficiency, wealth development potential, and liquidity for investors with a five-year or longer time frame who are at ease with market-linked returns. Rather of considering the decision as either/or, many financial advisors actually advise applying both tools in proportion to one's risk capacity. The goal is not to pick a winner but to build a tax-saving strategy that genuinely serves long-term financial wellbeing.