Table of Contents

Guide on Mandatory GST Forms – Due Dates, Late Fees & Penalties

Goods and Services Tax compliance is non-negotiable. Missing deadlines can lead to late fees, interest, ITC blockage, notices, and even cancellation of Goods and Services Tax registration. Goods and Services Tax Taxpayer Always reconcile GSTR-2B before filing GSTR-3B to avoid ITC mismatches and Maintain a GST compliance calendar for stress-free compliance. We should remember that

- Late filing = Late fee + Interest + ITC blockage

- Interest is mandatory (cannot be waived)

- Continuous defaults may lead to Goods and Services Tax cancellation

Use this must-follow GST compliance checklist.

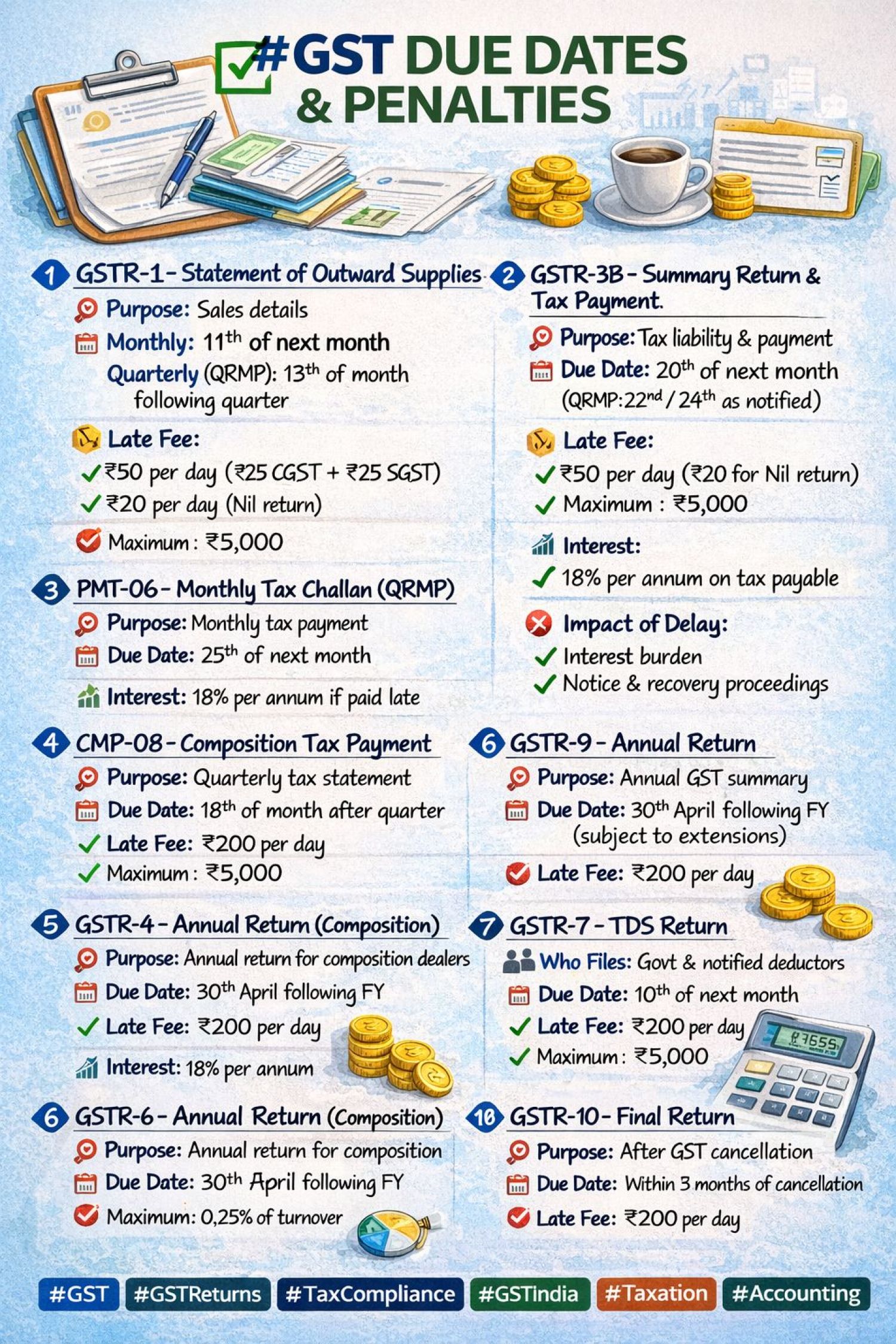

GSTR-1 – Outward Supplies

- Purpose: Reporting sales

- Due Dates: Monthly: 11th of next month and for QRMP: 13th of the month following the quarter

- Late Fee: INR 50/day (INR 25 CGST + INR 25 SGST) and INR 20/day for Nil return subject to Maximum: INR 5,000

- Impact of Delay: Buyer’s ITC blocked and Poor compliance rating for Goods and Services Tax taxpayer

GSTR-3B – Summary Return & Tax Payment

- Purpose: Tax payment + summary return

- Due Dates: Monthly: 20th of next month and in case of QRMP: 22nd / 24th (state-wise)

- Late Fee: INR 50/day and INR 20/day for Nil return subject to Maximum: INR 5,000

- Interest: 18% p.a. on delayed tax

- Impact: Interest cost and Notices & recovery proceedings to Goods and Services Tax taxpayer

PMT-06 – Monthly Tax Challan (QRMP)

- Purpose: Monthly tax deposit

- Due Date: 25th of next month

- Interest: 18% p.a. if delayed

CMP-08 – Composition Scheme Statement

- Purpose: Quarterly tax payment

- Due Date: 18th of month after quarter

- Late Fee: INR 200/day subject to Maximum: INR 5,000

- Interest: 18% p.a.

GSTR-4 – Annual Return (Composition Dealers)

- Purpose: Annual return

- Due Date: 30th April following FY

- Late Fee: INR 200/day subject to Maximum: INR 5,000

GSTR-9 – Annual GST Return

- Purpose: Complete annual Goods and Services Tax summary

- Due Date: 31st December following FY (subject to extensions)

- Late Fee: INR 200/day subject to Maximum: 0.25% of turnover

- Impact: Department scrutiny and Possible Goods and Services Tax notices to Goods and Services Tax taxpayer

GSTR-9C – Reconciliation Statement

- Purpose: Reconciliation of books vs GST returns

- Due Date: Same as GSTR-9

- Applicability: Above prescribed turnover limit

- Penalty Exposure: Up to INR 2 lakh in case of non-compliance

GSTR-7 – TDS Return

- Filed By: Government & notified deductors

Due Date: 10th of next month - Late Fee: INR 200/day subject to Maximum: INR 5,000

- Interest: 18% p.a.

GSTR-8 – TCS Return (E-Commerce)

- Filed By: E-commerce operators

- Due Date: 10th of next month

- Late Fee: INR 200/day subject to Maximum: INR 5,000

GSTR-10 – Final Return

- Purpose: After Goods and Services Tax registration cancellation

- Due Date: Within 3 months of cancellation

- Late Fee: INR 200/day subject to Maximum: INR 5,000