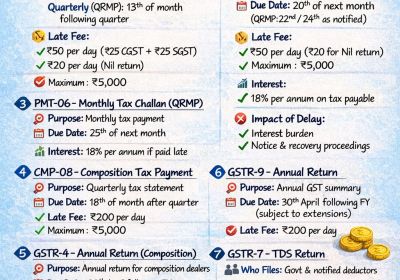

Table of Contents

- Physical Submission Of Gst Appeal Documents: Is It Necessary?

- Case Scenarios For Gst Appeal Submission

- Case I: Order Appealed Against Is Uploaded On Gst Portal

- Case Ii: Order Appealed Against Is Not Uploaded On Gst Portal

- Practical Recommendation:

- In Summary On Submission Of Gst Appeal Documents:

- New Update In Gst Appellate Tribunal

Physical Submission of GST Appeal Documents: Is It Necessary?

In the context of filing an appeal under GST, there is often confusion about whether a physical submission of the appeal documents is required after the online submission on the GST portal. Compliance with GST appeal procedures can be efficiently managed through electronic submissions. While physical submission is not required when the order is available on the portal, it is necessary to submit a self-certified copy of the order physically within seven days when the order is not uploaded online. This approach ensures adherence to legal requirements and maintains the efficiency of the appeal process.

Case Scenarios for GST Appeal Submission

- The necessity of physical submission depends on specific circumstances outlined under Rule 108(3) of the Central Goods and Services Tax Rules.

- Section 107 of the CGST Act, 2017 pertains to the appeals to the Appellate Authority. It does not explicitly specify whether the filing mode must be electronic or manual. Current Scenario there is no notification mandating manual filing of appeals. Therefore, the default mode for filing appeals, including Form GST APL-01, is electronic.

- Manual Submission Requirement:

- Applicable only when the order is not available on the common portal. In such cases, a self-certified copy of the order must be submitted within seven days of filing Form GST APL-01.

- The self-certification of the order should be done by the taxpayer, not by departmental officers.

KPMG India (P.) Ltd. v. Jt. Commissioner of State Tax (Appeals) [2023]:

- Ruling: The Punjab & Haryana High Court ruled that filing an appeal along with a digitally uploaded order on the common portal complies with Rule 108 of the CGST Rules, 2017. Appeals should not be dismissed if the order is uploaded electronically, reinforcing the validity of the electronic submission process.

Case I: Order Appealed Against is Uploaded on GST Portal

- Procedure: File the appeal online in Form GST APL-01. Receive a provisional acknowledgment online. A final acknowledgment in Form GST APL-02, indicating the appeal number, will be issued online.

- Requirement: No legal obligation to submit physical documents if the order is available on the portal.

- Rule 108(3) states that if the order being appealed against is available and uploaded on the GST portal, The appellant files the appeal in Form APL-01 online. A provisional acknowledgment is issued on the portal upon online filing. Within a few days, a final acknowledgment in Form APL-02, indicating the appeal number, is issued online by the authority.

Case II: Order Appealed Against is Not Uploaded on GST Portal

- File the appeal online in Form GST APL-01. Submit a self-certified copy of the order within seven days of filing Form GST APL-01. Receive the final acknowledgment in Form GST APL-02 online.

- Requirement: Mandatory to submit a self-certified copy of the order physically. Submission of manual Form GST APL-01 and relevant annexures may also be required. Physical submission of the self-certified copy of the order is required within seven days. Physical submission of the entire appeal document is not mandated, only the self-certified copy of the order.

- Proviso to Rule 108(3) states that if the order being appealed against is not available or uploaded on the GST portal, the following steps are necessary: The appellant files the appeal in Form APL-01 online. The appellant must submit a self-certified copy of the order being appealed within seven days from the date of online filing. After submitting the self-certified copy, a final acknowledgment in Form APL-02, indicating the appeal number, is issued online.

Practical Recommendation:

- For smooth processing and to avoid delays: Even when not legally required, consider submitting physical documents in addition to electronic submissions for comprehensive compliance. Ensure all necessary documents are accurately filed to facilitate timely issuance of the final acknowledgment (Form GST APL-02).

- The appeal is considered officially filed only when the final acknowledgment (Form APL-02) indicating the appeal number is issued.

- For practical reasons and to expedite the issuance of the final acknowledgment, it is advisable to physically submit all appeal documents after the online submission, especially if the documents are extensive and difficult to upload on the GST portal

In Summary on Submission of GST Appeal Documents:

Case I - Order Appealed Against is Uploaded on GST Portal: No physical submission is needed if the order is uploaded on the portal.

Case II—Order Appealed Against is Not Uploaded on GST Portal: Physical submission of a self-certified copy of the order is required if the order is not uploaded on the portal.

New update in GST Appellate Tribunal

- No Requirement of Physical Filing: Filing of physical documents is not required before GSTAT benches. And existing rules mandating physical filing are outdated and require revision. Which Impact that Move towards complete digitization of appellate process and Reduces procedural burden and paperwork

- Relaxation in Certification of Orders: There is no requirement to obtain certified copies of orders (OIO/OIA) from GST authorities. And self-certified copies are sufficient for appellate filing. Which impact eliminates delays in obtaining certified copies and facilitates faster filing of appeals.

- Possible Amnesty for Time-Barred Appeals :

- GSTAT has recommended the government consider amnesty scheme for Cases where first appeal was dismissed on limitation grounds

- GSTAT may Entertain such appeals and dispose of them through speaking orders

- Impact of Possible Amnesty for Time-Barred Appeals is significant relief for taxpayers who missed appeal timelines and an opportunity to revive genuine cases.

- Minimal Documentation for GSTAT Appeals: Only the following documents are considered essential: Show Cause Notice (SCN), Order-in-Original (OIO), Order-in-Appeal (OIA), Statement of Facts, Grounds of Appeal that Impact Simplifies Litigation. Reduces unnecessary documentation and encourages efficient and focused submissions.

- Relaxation in Translation Affidavits: No need for translation affidavits to be attested to by any government authority; Translation affidavits are required only if the bench is not comfortable with Hindi. Certification can be self-certified or counsel-certified, and that impact reduces procedural rigidity and enhances flexibility in language usage.

- GSTAT is moving towards ease of litigation, a digital-first approach, reduced procedural compliance, and faster dispute resolution. Which focus on substance over form, avoid unnecessary procedural delays, and prepare concise and well-structured appeals.

- The GSTAT is signaling a progressive, taxpayer-friendly approach, emphasizing simplification, efficiency, and reduction of procedural bottlenecks. If implemented effectively, these measures will significantly improve the GST litigation ecosystem in India.

Rajput Jain and Associates recommendation:

For practical purposes, submit all documents physically after online submission to ensure timely processing and acknowledgment. even in cases where it is not legally required. This helps in obtaining the final acknowledgment (Form APL-02) at the earliest. This approach is particularly useful when the submission involves numerous pages, as uploading large documents can be cumbersome on the GST portal.

For GST Audit Assistance, Departmental Notices, Refunds, Litigation & GST Health Check, you may position your advisory like this We provide end-to-end GST support, including litigation strategy, appellate drafting, audit reviews, refund optimization, and compliance health checks to ensure robust risk management and regulatory alignment.