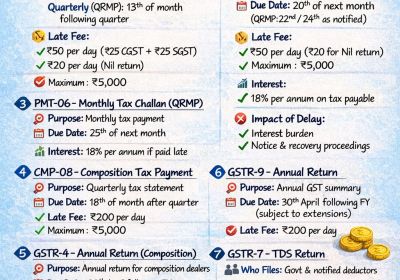

Table of Contents

- Gst On Commercial Rent From Unregistered Landlord—rcm Position

- When Does Rcm Apply?

- Important Gst Update On Commercial Rent (effective Immediately)

- Who Pays Gst Now?

- Domestic Rcm Prevails

- Gst Tax Liability Shift

- Applicable Gst Rate

- Liability Shifts From Landlord → Tenant

- Compliance Checklist For The Tenant

- What Taxpayers/businesses Should Do Immediately

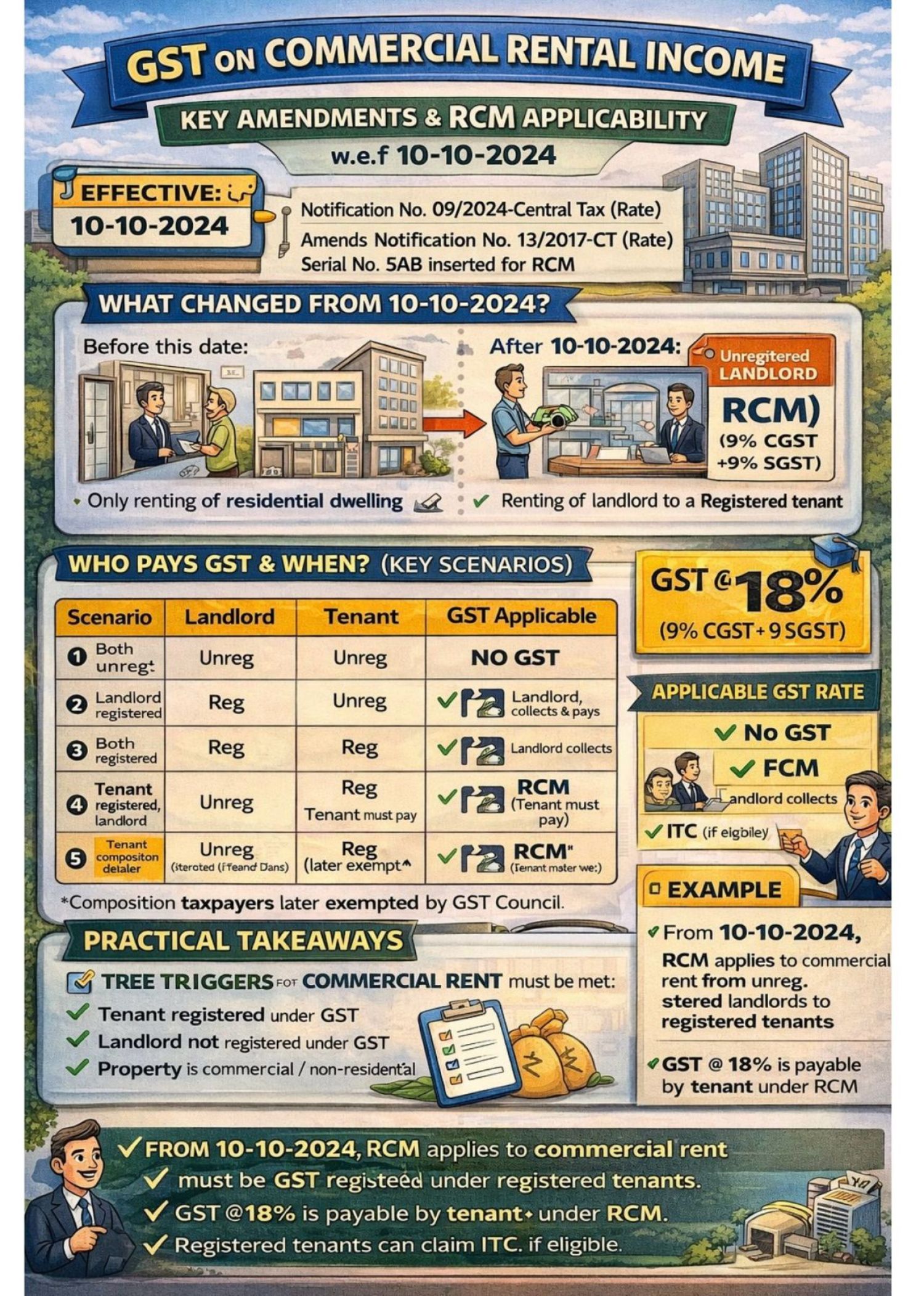

GST on Commercial Rent from Unregistered Landlord—RCM Position

When Does RCM Apply?

GST under the Reverse Charge Mechanism (RCM) applies when the property is commercial, the tenant is a registered person, and the landlord is unregistered. Renting of immovable property (other than residential dwelling for personal use) In such cases, GST @18% must be paid by the registered tenant under RCM. RCM Applicable w.e.f. 10‑10‑2024 A major change has been notified regarding GST on commercial rent, effective 10 October 2024..This is notified under Notification No. 09/2024–Central Tax (Rate) (as amended).

Earlier, RCM applied only on renting of residential dwellings for specific cases. From 10‑10‑2024, RCM also applies when a registered tenant takes a commercial property on rent from an unregistered landlord. That means the tenant must pay GST at 18% (9% CGST + 9% SGST) under the Reverse Charge Mechanism.

Important GST Update on Commercial Rent (Effective Immediately)

A significant change has been introduced regarding GST applicability on commercial rental income. If a registered tenant takes a commercial property on rent from an unregistered landlord, GST at 18% must now be paid by the tenant under the Reverse Charge Mechanism (RCM).

- RCM applies to commercial rent when the landlord is unregistered.

- GST liability shifts from landlord → to → tenant

- Registered tenants can claim ITC, subject to eligibility

- Noncompliance may lead to notices, interest, and penalties

This RCM GST-applicable amendment aims to ensure better reporting and compliance for commercial rental transactions. In many cases, the GST paid under RCM is revenue‑neutral, as tenants can usually avail Input Tax Credit. While cash flow timing may be impacted, the overall tax cost often remains unchanged.

Who Pays GST Now?

| Landlord | Tenant | GST Implication |

|---|---|---|

| Unreg. | Unreg. | No GST |

| Unreg. | Reg. | RCM applicable (tenant pays GST) |

| Reg. | Unreg. | Landlord pays GST (FCM) |

| Reg. | Reg. | The landlord collects GST (FCM) |

| Unreg. | Reg. (for commercial property) | RCM at 18% |

Composition suppliers have been exempted separately by GST Council.

- If registered → they charge GST under forward charge.

- If unregistered → tenant must pay GST under RCM

Domestic RCM Prevails

Because: The property is in India. The property and tenant are in the same state and Place of Supply rules for immovable property always lead to location of the property. This aligns with Section 12(3), IGST Act—when both parties are in India and Section 13(4), IGST Act—when one party is outside India. Both point to the same result POS = location of the property . Therefore It is treated as an intrastate supply. Tenant pays CGST + SGST under RCM, then NOT IGST. This also aligns with GST’s destination-based taxation and avoids interstate tax complications.

GST Tax Liability Shift

|

Situation |

Who Pays GST? |

|---|---|

|

Landlord registered |

Landlord (Forward Charge) |

|

Landlord unregistered + Tenant registered |

Tenant (RCM) |

|

Tenant unregistered |

RCM does NOT apply |

Applicable GST Rate

- 18% GST (9% CGST + 9% SGST) → Payable by tenant under RCM

- No GST when both parties are unregistered

- Tenant must be registered under GST, Property must be commercial / non‑residential, GST @18% becomes tenant’s responsibility under RCM, Registered tenants can claim ITC (if eligible)

-

This change aims at better reporting and GST compliance in commercial rental transactions. While tenants must now handle the tax payment, the impact is generally revenue‑neutral because ITC can be claimed.

Liability shifts from landlord → tenant

- ITC Eligibility: Registered tenant can claim Input Tax Credit (ITC) if the property is used for business purposes, GST paid in cash under RCM, Proper documentation & self-invoice maintained, and it is Reflected in GSTR-3B

- ITC is not allowed if used for exempt supplies & used for personal purposes. In most business cases → revenue neutral, but a cash flow impact exists.

- Compliance Requirements for Tenant : If RCM is applicable, the tenant must raise a self-invoice, then pay GST in cash (cannot use ITC to pay RCM), report in GSTR-3B (Table 3.1(d)), and claim ITC in Table 4A. Maintain proper documentation

- Risk of Non-Compliance : Failure may result in interest at 18%, a penalty under Section 73/74, and a departmental notice along with an ITC denial. Even small rental values over time can create large tax and interest exposure.

Compliance Checklist for the Tenant

If the landlord is unregistered, issue a self-invoice, pay CGST + SGST in GSTR 3B, then claim ITC (if eligible), maintain the rent agreement and payment proofs, and keep landlord details for the audit trail. If landlord is registered, pay GST to landlord (forward charge) and Claim ITC normally

Conclusion: Even though the NRI landlord resides outside India, the service is not treated as an import for GST tax-type purposes because the property is located in India, then POS = location of property = same state. RCM under Notification 09/2024 overrides practical treatment. Hence, the tax is CGST + SGST

What Taxpayers/Businesses Should Do Immediately

The taxpayer must review all commercial rent agreements, then verify the landlord's GST registration status, amend accounting software for RCM tracking, start a monthly RCM compliance check, and maintain proper documentation. Impact of this change

- Mostly revenue neutral for fully taxable businesses

- Cash flow blockage until ITC claimed

- Increases compliance burden

- Requires landlord GST status verification

Businesses should do now: review rent agreements immediately; the taxpayer must check the GST registration status of landlords & tenants and Align accounting and compliance processes and also prevent future tax exposure due to oversight. Businesses must adapt quickly. Even a small noncompliance in commercial rent can result in significant future tax liabilities.