Table of Contents

Declaration format in relation to Section 194Q, 206AB & 206CCA of the Income Tax Act 1961.

As you may be aware, the Finance Act of 2021 added section 194Q to the Income Tax Act of 1961, effective July 1, 2021, imposing 0.1 percent TDS on purchases of goods. Buyers with a total revenue of more than INR 10 crores in the previous year are required to deduct TDS on purchases above Rs. 50 lakhs.

In addition, Sec 206AB has been created, which applies a higher rate of TDS if the seller has not submitted an income tax return for the previous two years. It increases the compliance burden, and as a result, everyone is required to make disclosures in order to comply with it. The declaration format is given for everyone's convenience.

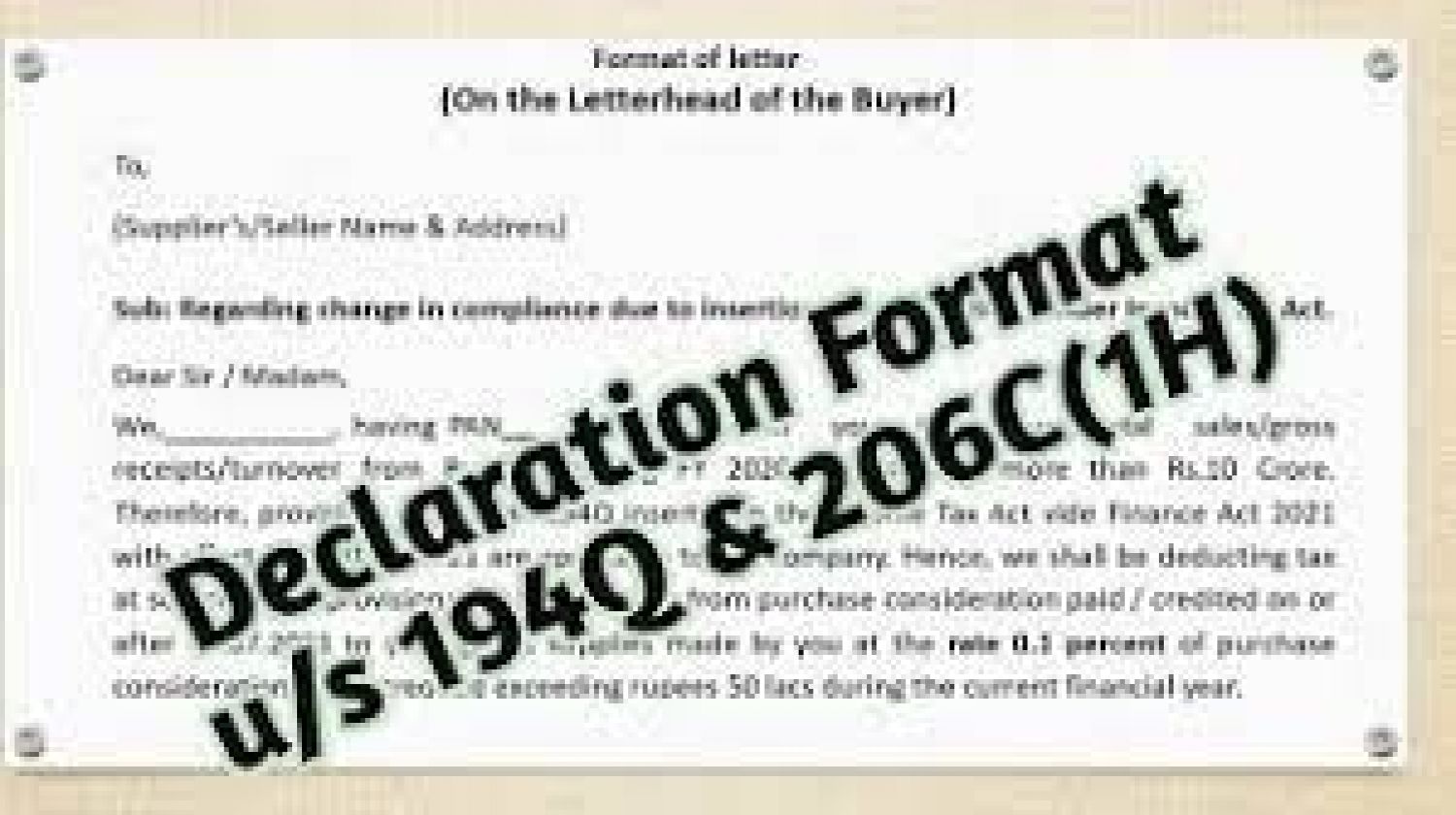

(On the Letterhead of the Buyer)

To,

(Supplier’s/Seller Name & Address)

Sub: Regarding change in compliance due to insertion of new sections under Income Tax Act. Deduction of TDS u/s 194Q and non-applicability of TCS u/s 206C (1H) of Income Tax Act.

Dear Sir / Madam,

We, (name of buyer) , having PAN (PAN of buyer) hereby inform you that our total sales/gross receipts/turnover from Business during FY 2020-21 has been more than Rs.10 Crore.

Therefore, provisions of Section 194Q inserted in the Income Tax Act vide Finance Act 2021 with effect from 01.07.2021 are applicable to our company. Hence, we shall be deducting tax at source at per provisions of above section from purchase consideration paid/ credited on or after 01.07.2021 to you against supplies made by you at the rate 0.1 percent of purchase consideration paid / credited exceeding rupees 50 lacs during the current financial year.

Since, we are liable to deduct tax at source under section 194Q of the Act, you may ensure not to take any action to collect tax at source under section 206C (1H) of the Act w.e.f. 01.07.2021, in case provisions of section are applicable to you considering your amount of turnover and our purchases being of more than rupees 50 lacs.

You are also requested to intimate your Permanent Account Number. In case you fail to provide your PAN, tax will be deducted at a higher rate in terms of Section 206AA of the Act.

Further, you are also required to confirm that in your case amount of TDS/TCS was Rs.50,000/- or more in previous years relevant to Assessment Years 2019-20 and 2020-21 and you have filed your returns of income for these assessment years according to section 139(1), otherwise tax is required to be deducted at a higher rate in terms of Section 206AB of the Act.

Further, as per Rule 114AAA, higher of TDS/TCS will be applicable in case PAN and AADHAR is not linked. This is applicable only in case of Individual.

You may send to us your declaration in the enclosed draft on or before 25.06.2021 to enable us to take note of same and modify our accounting software accordingly. In case we do not receive your declaration by the above date, we will modify our software to deduct tax at the higher rate and it would be difficult for us to take corrective action to reduce the rate during the current financial year.

Further, we confirm that (name of buyer) has filed its Income Tax Return for the previous year 2018-19 & 2019-20. You may accordingly ensure that in case of applicability of Tax deduction u/s 194Q, TDS is deducted @ 0.1% on all purchases from us. The status of return of Income filed by (name of buyer) is as under: –

| Assessment year | Acknowledgement No. | Filing Date |

| AY 2019-20 | ||

| Assessment Year 2020-21 |

It's important to note that any financial loss that (name of buyer) suffers as a result of your non-compliance will have to be covered by you. As a result, we anticipate your active participation in the process.

Thanks,

For (name of buyer)

Authorized Signatory

Then The vendor will then confirm its details on the below format.

(On the letter head of the seller)

To,

(Buyer Name & Address)

Sub: Declaration / information for deduction of tax at source u/s 194Q of the income tax Act.

Dear Sir,

This is with reference to your letter dated requiring our declaration / information in regard to deduction of tax at source u/s 194Q of the Act. The information is being provided hereunder:

- Since your company is liable to deduct tax u/s 194Q of the Act, you may deduct the tax @0.1 % of sale consideration paid /credited by your company to us on the amount exceeding Rs.50 lacs during the current financial year. We also confirm that we will not take any action to collect tax at source under section 206C(1H) of the Act w.e.f. 01.07.2021.

- Permanent Account Number of our company is (PAN of seller) . Further, we have duly filed our returns of income for Assessment Years 2019-20 and 2020-21 as per the information given hereunder:

| Assessment year | Acknowledgement No. | Filing Date |

| AY 2019-20 | ||

| Assessment year 2020-21 |

Our PAN and AADHAR is linked. This is applicable only in case of Individual. Please keep the following information in mind & deduct TDS at the appropriate rate, taking into account the aforementioned information.

Thanks,

For (Seller Name)

Authorized Signatory

Popular Articles :