Table of Contents

Consolidation & Rationalisation of TDS Sections Provisions

The Income Tax Act, 2025, introduces a major structural rationalisation of Tax Deduction at Source provisions, aimed at improving clarity, ease of compliance, and administrative efficiency without altering the substantive tax framework. This reform does not impact taxability or rates of deduction but reorganises the law into a streamlined and more accessible format, replacing fragmented provisions with a coherent, table-driven framework. Overall, this change represents a significant step toward simplification without dilution, aligning tax administration with modern compliance practices.

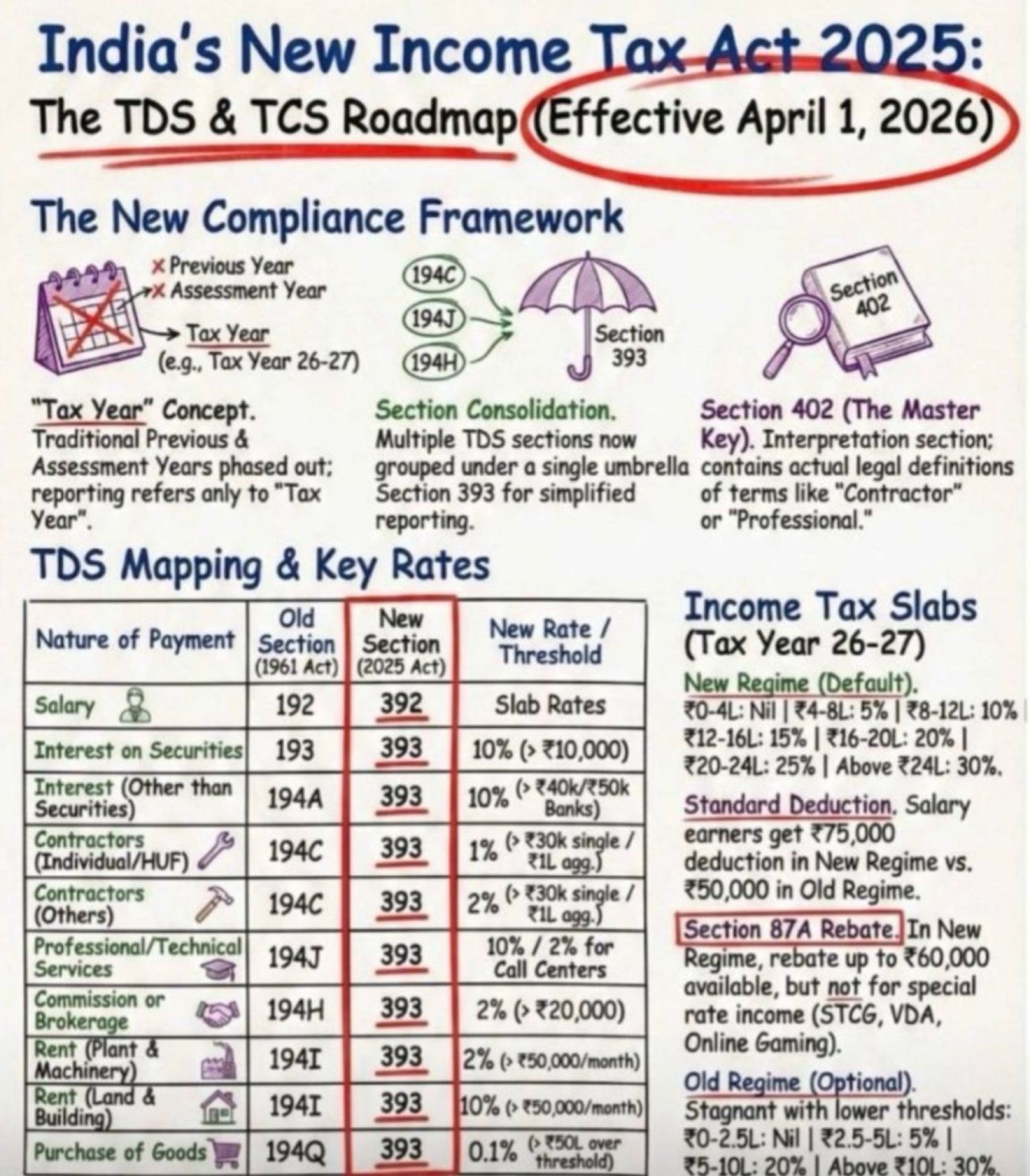

Consolidation of TDS Sections : The existing Tax Deduction at Source provisions contained in Sections 192 to 194T of the Income-Tax Act, 1961, have been consolidated into two comprehensive sections, replacing over 25 individual provisions:

- Section 392 – Applicable to income chargeable under the head “Salaries”

- Section 393 – Applicable to non-salary payments. Consolidating the fragmented 194‑series into a single charging provision (Section 393) is conceptually sound. Over the years, TDS compliance became less about withholding tax principles and more about section identification. This reform addresses that problem directly.

- The introduction of Section 402 (Interpretation & Definitions) is particularly important. Litigation around “contract for work vs contract for service”, professional vs technical, etc., has historically been a major pain point. A centralised definition framework can materially reduce ambiguity if drafted tightly and consistently applied.

- While the section numbering and structure have changed, the underlying principles, scope, and applicability of Tax Deduction at Source remain intact.

Structured Framework under Section 393 : To enhance usability, Section 393 adopts a table-based framework, categorising payments into three distinct tables

- Table A – Payments to Residents

- Table B – Payments to Non-Residents

- Table C – Payments applicable to Any Person

Each table clearly specifies the nature of income, applicable monetary threshold, person responsible for deduction, and rate of tax deduction at source. This tabular approach simplifies interpretation and reduces dependency on cross-referencing multiple provisions.

Continuity of Lower / Nil Deduction Certificates: To ensure a smooth transition, the Act provides that certificates issued under Section 197, which are valid beyond 31 March 2026, shall continue to remain valid under the new provisions. And No fresh application is required for such certificates merely due to renumbering or restructuring of Tax Deduction at Source sections. This is a crucial compliance relief for taxpayers and deductors alike.

System and Compliance Readiness : Given the change in section numbering, it is essential for organisations to update ERP systems (SAP, Oracle, Tally, etc.), Modify Tax Deduction at Source computation logic and compliance software, and align return preparation tools and control frameworks. Early system readiness will be critical to avoid reporting mismatches, system validation errors, and compliance lapses.

The reform strongly points toward transaction-level reporting discipline. With Unified TDS (Section 393),, Rationalised TCS (Section 394), higher rates on luxury and discretionary spending, and a strong linkage with LRS and cross-border flows. the law is clearly designed to improve data coherence across TDS–TCS–AIS–26AS and strengthen risk-based analytics rather than rate tinkering. Those who treat this merely as a “renumbering exercise” will struggle. Those who rebuild their master data and rules engines around ‘nature of payment’ will benefit.

ITR Due Dates under the Income Tax Act, 2025

Key Benefits Emphasized in the Update: A longer correction window (4 years vs. earlier limits) encourages voluntary compliance, reduces last‑minute filing stress, and provides a structured cost curve for delayed corrections. This framework strengthens the philosophy of “tax certainty with accountability” under ITA 2025. At a Glance – Section Renumbering Highlighted as below

|

Category of Taxpayer |

Due Date |

Old Section (ITA 1961) |

New Section (ITA 2025) |

|

Individual / HUF / AOP / BOI (Non‑audit) |

31 July following the Tax Year |

139(1) |

263(1)(c) |

|

Business / Profession / Partners (Non‑audit) |

31 August |

139(1) |

263(1)(c) |

|

Businesses / Firms (Tax Audit) |

31 October |

139(1) |

263(1)(c) |

|

Companies (Domestic / Foreign) |

31 October |

139(1) |

263(1)(c) |

|

Transfer Pricing Cases |

30 November |

139(1) |

263(1)(c) |

|

Belated Return |

31 December |

139(4) |

263(4) |

|

Revised Return |

31 March |

139(5) |

263(5) |

While dates remain largely unchanged, sections are fully renumbered under the Income Tax Act, 2025 — a critical compliance shift for drafting, representation, and education.

Late Fees (Post 31 December) :

Late fees continue to apply if return is filed after 31 December of the tax year:

|

Total Income |

Late Fee |

|

≤ INR 5,00,000 |

INR 1,000 |

|

> INR 5,00,000 |

INR 5,000 |

Practically relevant for belated vs updated return decision‑making.

Updated Return (ITR UN / ITR U Equivalent)

Extended Window: Up to 48 months from the end of the Tax Year and (Section 139(8A) → New Section 263(6)) and Additional Tax Slab Structure

|

Filing Timeline (from end of TY) |

Additional Tax |

|

Within 12 months |

25% |

|

Within 24 months |

50% |

|

Within 36 months |

60% |

|

Within 48 months |

70% |

Section references will change training material, submissions, and templates must be updated. The ITR‑U strategy becomes more nuanced cost vs risk analysis over 48 months. 31 December as a fee trigger and a 48-month horizon as a last compliance resort, not a default

Conclusion : The rationalisation of Tax Deduction at Source provisions under the Income Tax Act, 2025, is structural rather than substantive in nature. Importantly, tax deduction at Source rates, monetary thresholds, Due dates for deposit and return filing, interest and penalty provisions, and computation methodology.

Consolidation will simplify the law but not the first year of compliance. This is a structural reform, not a rate reform. Its success will depend on Quality of implementation rules, CBDT’s willingness to issue timely clarifications, and how quickly ecosystems (ERPs, TRACES, TIN, and payroll engines) adapt. Strategic Takeaway for Tax & Finance Teams

|

Time Horizon |

Impact Assessment |

|

Short term (FY 2026–27) |

Higher operational effort, retraining, reconfiguration |

|

Medium term |

Reduced interpretational disputes |

|

Long term |

Cleaner audits, better analytics, simpler law navigation |