Table of Contents

- Tds On Payments To Non Residents Income Tax Act, 2025 W.e.f 1.04. 2026

- Structural Shift In Law: Replacement Of Section 195 income Tax Act, 2025

- Tax Deducted At Source Applicability Under The Income Tax Act, 2025

- Double Taxation Avoidance Agreement Benefit For Nri Of The Income Tax Act, 2025

- Tax Deducted At Source Rates non Residents (indicative)

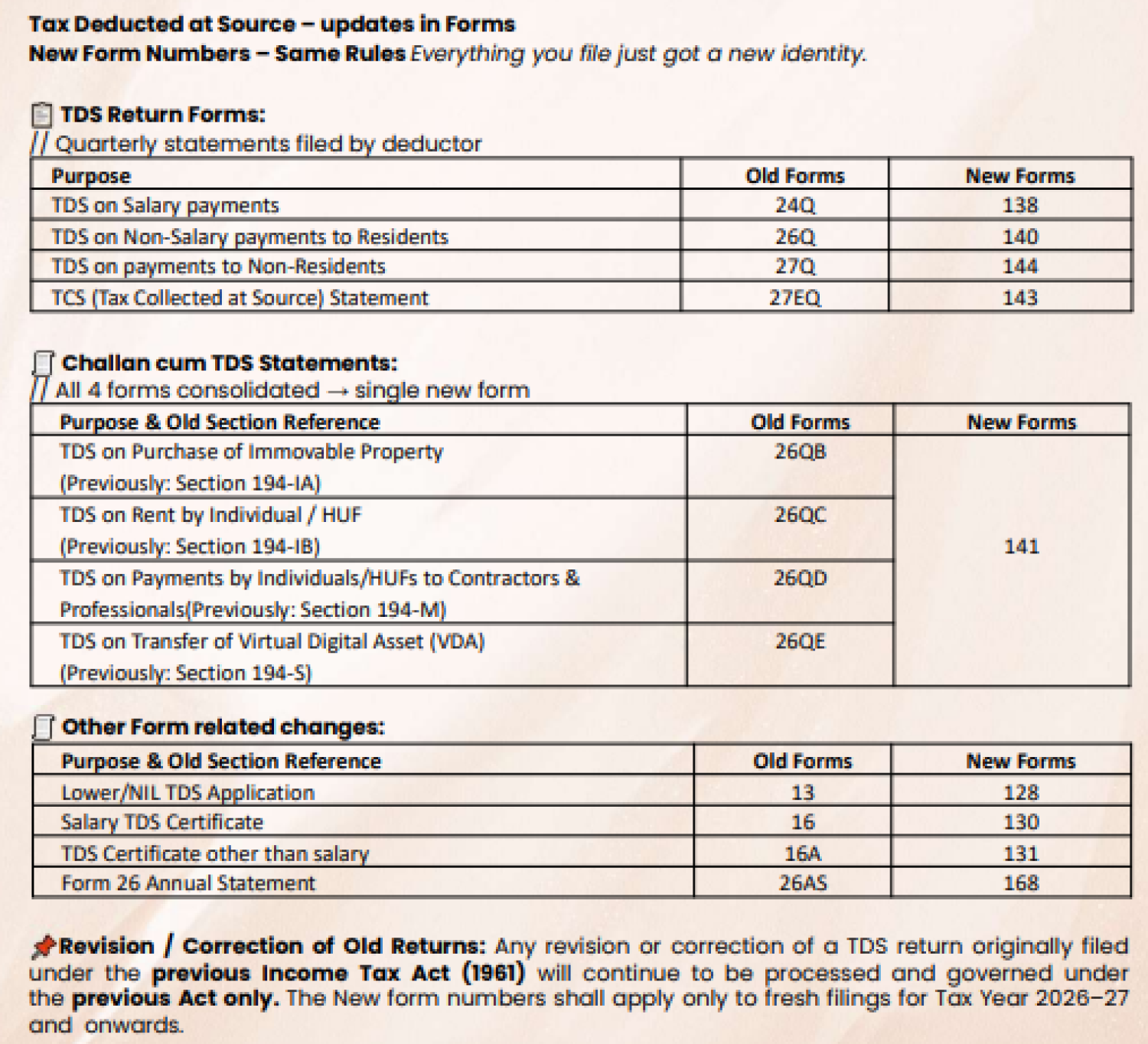

- New Regime Compliance Essentials: Forms & Returns Under The Income Tax Act, 2025

- Taxes Deducted At Source Due Dates Under The Income Tax Act, 2025

- Common Errors Or High Risk Areas Tds On Payments To Non‑residents After The Income Tax Act, 2025

- Property Transactions With Non Residents Under The Income Tax Act, 2025

TDS on Payments to Non Residents Income Tax Act, 2025 w.e.f 1.04. 2026

Structural Shift in Law: Replacement of Section 195 Income Tax Act, 2025

Under Section 393(2) of the Income Tax Act, 2025 replaces Section 195 of the Income-tax Act, 1961 for Tax deducted at source on non-resident payments. While rates remain largely similar, section references, forms, and compliance workflow are revamped. Under the Income Tax Act, 2025, non-resident Tax deducted at source is compliance-driven rather than rate-driven. Documentation, section accuracy, and timing will determine litigation risk. Key Features of Section 393(2) are as follows

Tax deducted at source Applicability Under the Income Tax Act, 2025

No minimum threshold for TDS on NRI : Tax deducted at source applicable from INR 1, unless specifically exempt. Moreover, TDS applies to any sum chargeable to tax paid or credited to a non-resident.

Double Taxation Avoidance Agreement Benefit for NRI of the Income Tax Act, 2025

The Double Taxation Avoidance Agreement rates can be applied only if all documents are obtained before payment i.e. Tax Residency Certificate, Form 10F, Proof of Beneficial Ownership etc In absence of complete documentation, domestic rates apply automatically. And Surcharge & Cess

- Surcharge + 4% Health & Education Cess applicable under domestic law.

- No surcharge/cess where Double Taxation Avoidance Agreement rate is applied, unless the treaty explicitly provides otherwise.

Tax deducted at source Rates Non Residents (Indicative)

|

Nature of Income |

Tax deducted at source Rate |

|

Salary |

As per slab rates (Section 392) |

|

Interest Income |

10% – 30% |

|

Capital Gains |

12.5% – 20% |

|

Rental Income |

30% on gross rental value |

|

Royalty & Technical Services |

10% – 20% |

|

Sportsman / Entertainer |

Flat 20% |

The final rate depends on the nature of income, Double Taxation Avoidance Agreement applicability, surcharge, and Cess.

New Regime Compliance Essentials: Forms & Returns under the Income Tax Act, 2025

- Income Tax Form 144 of the Income Tax Act, 2025 → replaces Income Tax Form 27Q

- Correct section codes of the Income Tax Act 2025 must be used

- Tax deducted-at-source Certificate: Issue new-format Tax-deducted-at-source certificates reflecting revised law and section references

Taxes deducted at source Due Dates under the Income Tax Act, 2025

- Tax deducted at source payment:

- On or before 7th of next month

- March deductions: 30th April

- Lower / Nil Tax deducted at source: Apply via Form 13

Common Errors or High Risk Areas TDS on Payments to Non‑Residents after the Income Tax Act, 2025

- Quoting old sections (e.g., Section 195)

- Non‑deduction assuming “non‑taxable” without Double Taxation Avoidance Agreement analysis

- Delay in Tax deducted at source deposit or income tax New Form 144 of the Income Tax Act, 2025 filing

- Ignoring surcharge & cess under domestic law

- Applying Double Taxation Avoidance Agreement without complete documentation

Property Transactions with Non Residents under the Income Tax Act, 2025

Tax deducted at source on gross consideration: Tax to be deducted on total sale value, not net capital gain. Compliance simplifications are mentioned here below:

- Permanent Account Number-based simplified process proposed from October 2026

- Until then, standard non-resident Tax deducted at source framework applies