Table of Contents

Key changes in Schedule-III of the Companies Act which is applicable from 1-april- 2021

- the MCA revised Schedule III of the Companies Act 2013 with the goal of increasing openness and giving users of financial statements more disclosures with effect from On March 24, 2021.

- These changes will be in effect as of 1 April 2021 and will therefore apply to the financial statements created for FY 2021–2022.

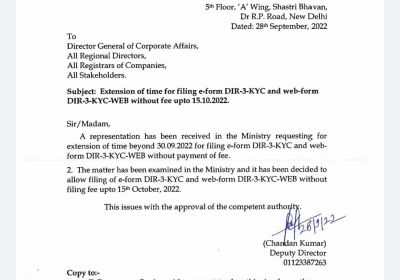

MCA issues clarification on “Compulsory companies to round off figures appearing in the Financial Statements”

- Schedule III of the Companies Act of 2013 has been amended, see According to their total income, companies are required to round off the figures in their financial statements under a Ministry of Corporate Affairs Notification dated March 24, 2021.

- However, if the companies provide correct figures in ROC E-forms ie. AOC-4, the same shall not be treated as incorrect certification by the Professionals..

FOR DIVISION-1- Accounting Standard - Complied Companies :

- Rounding off of the figures are now compulsory. Earlier it was optional

Schedule-III of the Companies Act For PART-I Balance Sheet

-

Few changes in Balance Sheet items.

-

Loans given to promotes, directors, KMP and related parties- Additional disclosure

-

In case borrowed funds from financial institution & banks not utilised for the prescribe purpose, then to disclose the details where the funds have been utilized.

-

Pending registration of charges and pending satisfaction of charges- Additional disclosure

-

If title deed of property not in company name then additional disclosure to be given.

-

Additional disclosure for – ageing wise analysis of intangible assets under development.

-

Details of benami properties held.

-

Additional disclosure in case of bank borrowings on the basis of security of current assets. To give detail whether the books are matched with the periodical details submitted to bank.

-

Ageing wise analysis discloser of Trade receivable is must to be disclosed.

-

Many financial ratios & Accounting - ( i.e around 10 ratios) to be disclosed along with denominator & numerator along with reason for variation with Last Year.

-

Ageing wise analysis discloser of trade payable is must to be disclosed.

-

Relationship with struck off companies -Additional disclosure

-

Ageing wise analysis discloser of capital WIP- Additional disclosures.

-

Various additional disclosures in case of utilization of borrowed funds and share premium etc.

-

willful defaulter Additional disclosures

-

Owners or Promotors holding In share capital schedule is must to be disclosed.

-

Additional disclosure for non-Compliance with No of layers of companies.

Schedule-III of the Companies Act - For PART-II - Profit & Loss Account

-

Various detailed disclosures for Corporate social responsibility.

-

Additional disclosure for undisclosed income surrendered during any search or survey under the income tax act.

-

Trade or investment details in any virtual currency and & crypto currency.