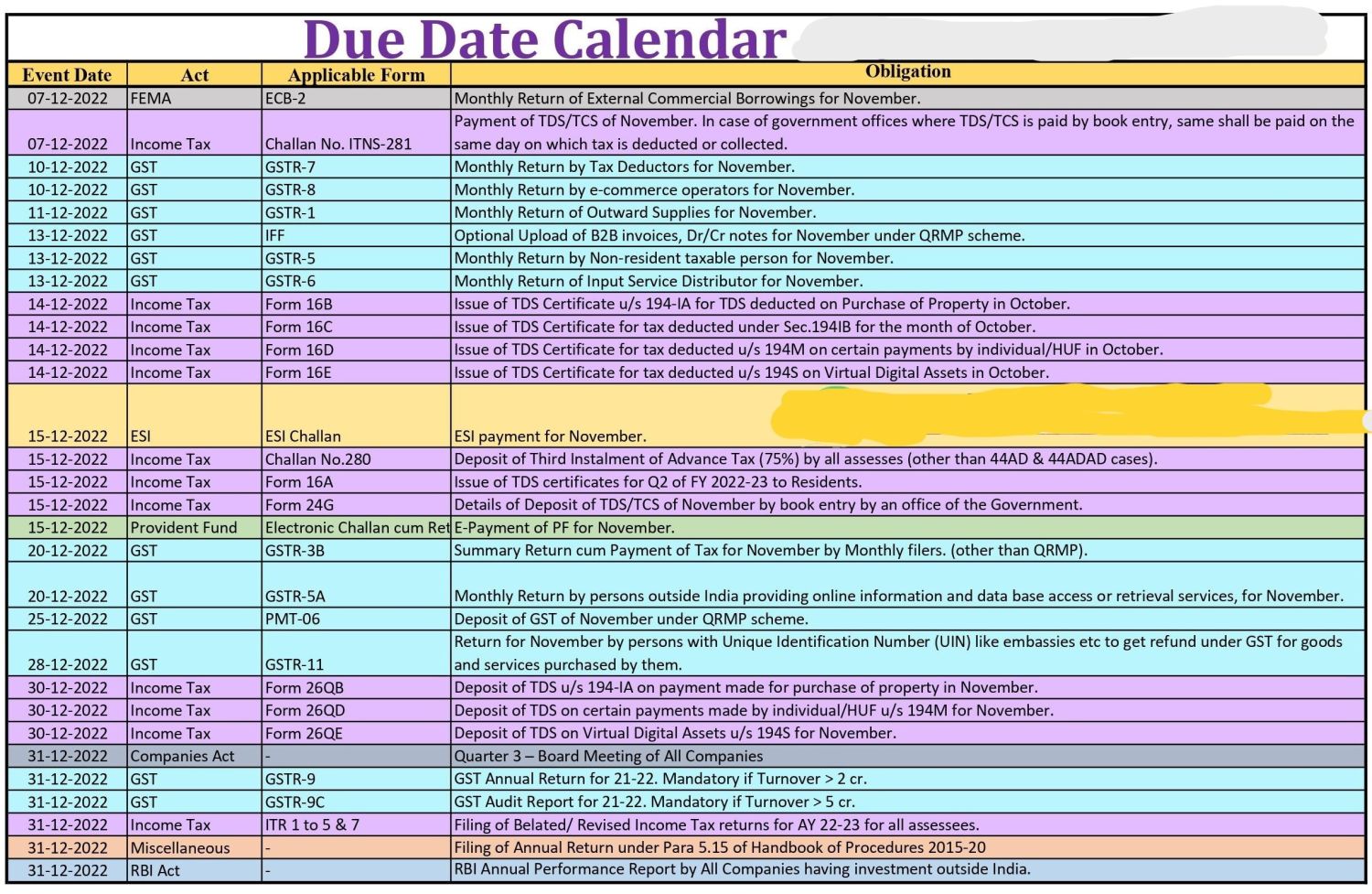

Table of Contents

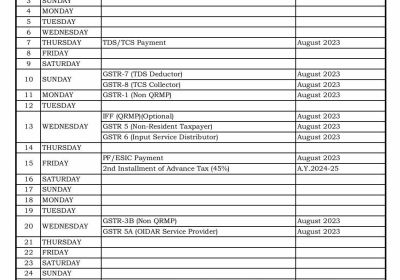

Tax and Statutory Compliance Calendar for December 2022

|

S. No. |

Statue |

Purpose |

Timeline & Compliance Period |

Due Date |

Compliance Details |

|

1 |

Income Tax |

Tax deducted at sources / Tax collected at source Liability Deposit |

November -2022 |

7-December-2022 |

Timeline of depositing Tax deducted at sources / Tax collected at source liabilities under the Income Tax Act, 1961 for the previous month. |

|

2 |

Income Tax |

Form 24G |

November -22 |

15-December-2022 |

Timeline for furnishing of form 24G by an office of the government where Tax deducted at sources / Tax collected at source for the month of November 2022 has been paid without the production of a challan |

|

3 |

Income Tax |

Advance Tax |

November -22 |

15-December-2022 |

​The third installment of advance tax for the AY 2023-24. |

|

4 |

Income Tax |

TDS Certificate |

Nov-22 |

15-December-2022 |

Timelinefor issue of TDS Certificate for tax deducted under sections 194-IA, 194-IB, and 194M in the month of October 2022. |

|

4 |

Income Tax |

TDS Certificate |

Nov-22 |

15-December-2022 |

Timelinefor issue of TDS Certificate for tax deducted under section 194S in the month of October 2022. Note: Applicable in case of a specified person as mentioned under section 194S. |

|

5 |

Income Tax |

Income tax Form 3BB |

November -22 |

15-December-2022 |

D​ue date for the furnishing statement in Form no. 3BB by a stock exchange in respect of transactions in which client codes have been modified after registering in the system for the month of November 2022. |

|

6 |

Income Tax |

Income tax return |

FY 2021-22 |

31-December-2022 |

​Filing of revised/ belated Income tax return for the AY 2022-2023 for all assessees (provided assessment has not been completed before December 31, 2022). |

|

7 |

Income Tax |

Tax deducted at sources Challan cum Statement |

November 2022 |

30-December-2022 |

Timelinefor furnishing of challan-cum-statement in respect of tax deducted under section 194-IA, 194-IB, 194-M, in the month of November 2022. |

|

8 |

Income Tax |

Income Tax Form No. 3CEAD |

FY 2021-22 |

30-December-2022 |

​Furnishing of the report in Form No. 3CEAD for a reporting accounting year (assuming reporting accounting year is January 1, 2021, to December 31, 2021) by a constituent entity, resident in India, in respect of the international group of which it is a constituent if the parent entity is not obliged to file report under section 286(2) or the parent entity is a resident of a country with which India does not have an agreement for the exchange of the report, etc. |

|

9 |

Income Tax |

Tax deducted at sources Challan cum Statement |

November -22 |

30-December-2022 |

​Timelinefor furnishing of challan-cum-statement in respect of tax deducted under section 194S in the month of November 2022. Note: Applicable in the case of the specified person as mentioned under section 194S. |

|

10 |

Company Law |

Board Meeting |

FY 2022-23 |

31-December-2022 |

Quarter 3rd Board meeting for all companies on or before 31st Dec2022. |

|

11 |

Labour Law |

Provident Fund / ESI |

November 2022 |

15-December-2022 |

Timeline for payment of Provident fund and ESI contribution for the previous month. |

|

12 |

Goods and services Tax |

GSTR - 3B |

November -22 |

20-December-2022 |

1. Goods and services Tax Filing of returns by a registered person with aggregate turnover exceeding Rs 5 Crores during the preceding year. 2. Registered person, with aggregate turnover of less than Rs 5 Crores during the preceding year, opted for monthly filing of returns under Quarterly Returns with Monthly Payment. |

|

13 |

Goods and services Tax |

GSTR -5 |

November -22 |

20-December-2022 |

GSTR-5 is to be filed by a Non-Resident Taxable Person for the previous month. |

|

14 |

Goods and services Tax |

GSTR -5A |

November -22 |

20-December-2022 |

GSTR-5A is to be filed by Online Information Database Access and Retrieval services Service Providers for the previous month. |

|

15 |

Goods and services Tax |

PMT-06 (Payment of Tax) |

Nov-22 |

25-December-2022 |

Timelineof payment of Goods and services Tax liability by the registered person whose aggregate turnover was less than Rs 5 Crores during the preceding year and who has opted for quarterly filing of return. |

|

16 |

Goods and services Tax |

GSTR-9 |

2021-22 |

31-December-2022 |

GSTR-9 is the annual return required to be filed by every person whose aggregate turnover was more than Rs 2 Crores during the preceding year. |

|

17 |

Goods and services Tax |

GSTR-9C |

2021-22 |

31-December-2022 |

GSTR-9C is the annual return required to be filed by every person whose aggregate turnover was more than Rs 5 Crores during the preceding year. |

|

18 |

Goods and services Tax |

GSTR-7- TDS return under GST |

November -2022 |

10-December-2022 |

GSTR 7 is a return to be filed by the persons who is required to deduct TDS under GST. |

|

19 |

Goods and services Tax |

GSTR-8- TCS return under GST |

November -2022 |

10-December-2022 |

GSTR-8 is a return to be filed by the e-commerce operators who are required to deduct TCS under GST. |

|

20 |

Goods and services Tax |

GSTR-1 |

November -2022 |

11-December-2022 |

"1. GST Filing of returns by a registered person with aggregate turnover exceeding Rs 5 Crores during the preceding year.

|

|

21 |

Goods and services Tax |

IFF (Invoice Furnishing Facility) |

November -22 |

13-December-2022 |

GSTR-1 of a registered person with turnover less than Rs 5 Crores during the preceding year and who has opted for quarterly filing of return under Quarterly Returns with Monthly Payment . |

|

22 |

Goods and services Tax |

GSTR -6 |

November -22 |

13-December-2022 |

Timelinefor filing return by Input Service Distributors. |

*Note 1: Opting for Quarterly Returns with Monthly Payment Scheme- Timeline for filling GSTR - 3B with Annual Turnover up to INR 5 Crore in State A Group (Chhattisgarh, Maharashtra, Karnataka, Goa, Kerala, ,Madhya Pradesh, Gujarat, Daman & Diu, and Dadra & Nagar Haveli, Puducherry, Andaman, and the Nicobar Islands,Tamil Nadu, Telangana, Andhra Pradesh, Lakshadweep).

**Note 2: Opting for Quarterly Returns with Monthly Payment Scheme- Timeline for filling GSTR - 3B with Annual Turnover up to INR 5 Crore in State B Group (Himachal Pradesh, Punjab, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand, Odisha, Jammu and Kashmir, Ladakh, Chandigarh, Delhi).