Table of Contents

GST Notice Trap: Section 160(2) of the CGST Act and the Point of No Return

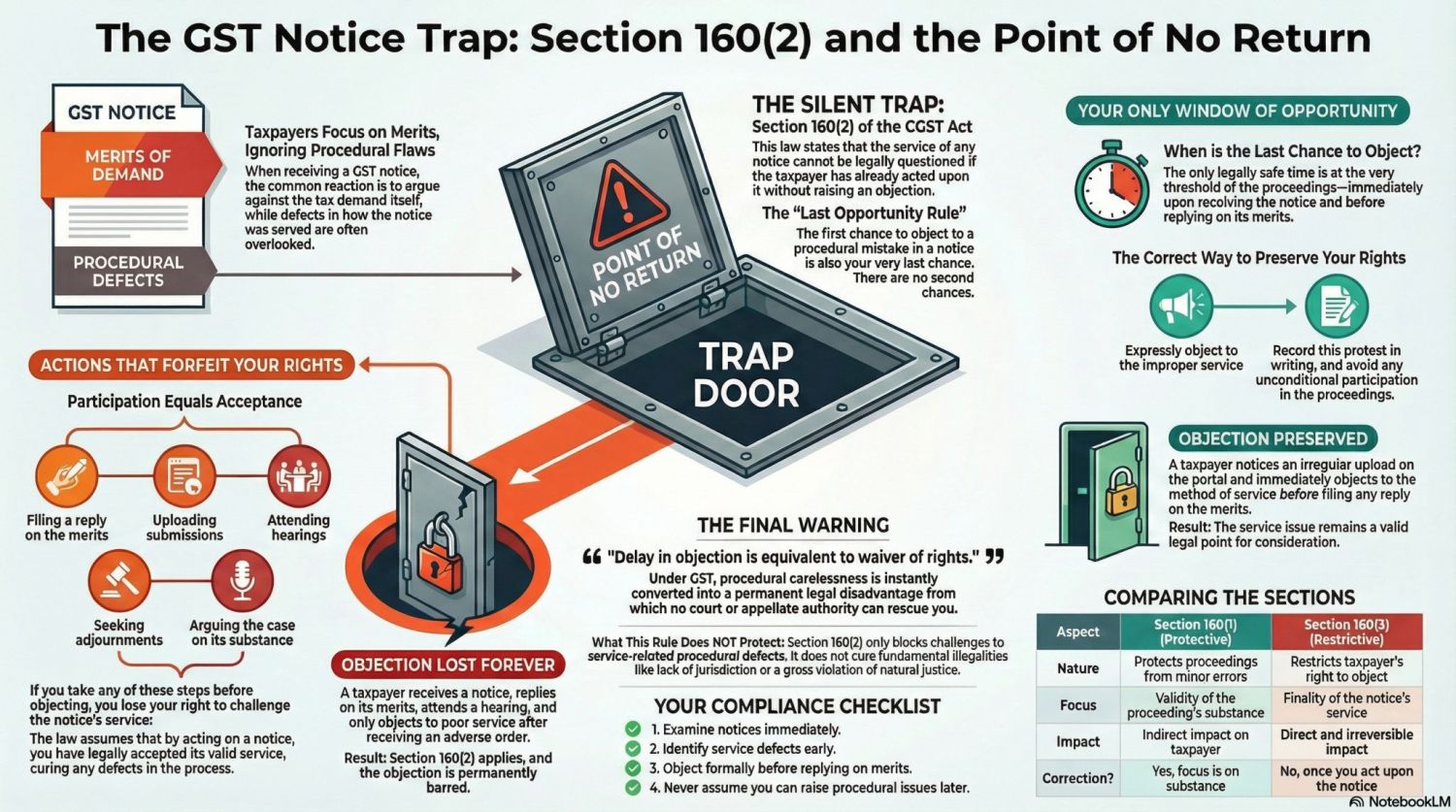

Section 160(2) of the CGST Act creates a critical but silent trap for taxpayers who receive any GST notice with procedural defects. If a GST notice, order, or communication is made available on the GST portal, it is deemed to be validly served even if the taxpayer claims they never saw it. No email opened., No SMS read., No login done. Then Legally irrelevant. Once it hits the portal, the clock starts ticking.

COMMON FATAL ERRORS (Seen Daily in Practice)

- Reply filed without preliminary objection

- Defect raised after adverse order

- “Accountant will handle it” mindset

- Missed “Additional Notices” tab Assuming defective notice is void automatically

- All cured by Section 160(2)

Why this becomes a “Point of No Return”: Section 160(2) of the CGST Act blocks one of the most common defenses used by taxpayers: “I never received the notice.” Courts and authorities routinely reject this argument because the GST law presumes digital awareness, portal availability = legal service, and ignorance ≠ excuse. Like, miss the deadline, then the order becomes final, and appeal rights weaken thereafter, and recovery proceedings start.

The Fatal Mistake Taxpayers Make: Many taxpayers File a reply, attend a personal hearing, and upload documents but do not object that Notice is vague, the wrong section is invoked, No proper opportunity is given, and the time limit is not followed. Which results in the law concluding, “You accepted the notice as valid.” Later, during appeal or writ, “Notice was defective” and rejected due to Section 160(2).

Real-life consequences seen in practice: Because of Section 160(2) of the CGST Act, taxpayers have faced Ex-parte assessment orders, ITC reversals without hearing, penalty and interest demands, GST registration cancellation, and bank account attachment (DRC-13). All because the notice sat quietly on the portal.

1. What Section 160(2) of the CGST Act Says: If a GST notice has a procedural defect (wrong section, wrong format, wrong officer, wrong date, wrong reference, etc.) but you still participate in the proceedings, then GST Taxpayer are deemed to have accepted the notice as valid. You lose the right to challenge the notice later. Any objection to procedural lapses becomes time‑barred. This is commonly known as the “Point of No Return”. Following are Common misconceptions (and why they fail)

|

Myth |

Reality |

|---|---|

|

Email didn’t come |

Portal posting is enough |

|

Accountant didn’t inform |

Taxpayer is still responsible |

|

Login issues |

Not a valid legal defence |

|

No physical notice |

GST law allows electronic service |

2. How Taxpayers Fall into the Trap: Most taxpayers respond based on merits, ignoring procedural defects like Improper SCN format, Wrong DIN, Incorrect officer jurisdiction, Vague or missing allegations, Time-barred demand notice, non-speaking SCN. When you upload submissions, attend hearings, argue on merits, seek adjournments, and provide documents. You automatically validate the defective notice. This is why it’s called the Trap Door.

3. Actions That Forfeit Your Rights: According to the infographic, if you do ANY of these before objecting, you lose your right forever Filing reply on merits, Uploading documents, participating in personal hearing, Arguing the case and Seeking adjournment Once you do this → Section 160(2) of the CGST Act shuts the door permanently.

4. The Only Window to Save Yourself: You get just one chance, and that too before you participate. The correct action Immediately object to the procedural defect in writing, clearly and specifically. What this achieves: It preserves your right to challenge the notice later. It protects you during appeal/writ, It prevents the “deemed acceptance” under Section 160(2) of the CGST Act

5. Objection Preserved (What Happens Next) : When you give a timely objection. The officer must address the defect; GST taxpayers are not deemed to have accepted the notice, and the GST taxpayer's right to contest the legality remains intact. Appeals/writ petitions remain open to you

6. Objection Lost Forever (If You Delay) : If you object after participating, “Delay in objection is equivalent to waiver of rights.” You lose Right to challenge procedural defect, right to question jurisdiction, and the right to question validity of the notice And the defect becomes non‑challengeable.

7. Compliance Checklist (To Avoid the Trap): How to stay out of the trap (practitioner-tested): This is no longer optional hygiene; it’s risk management. Before replying to any GST notice: Log in to GST portal at least once a week

- Step 1: Check procedural validity—Check: Services → View Additional Notices/Orders. Is DIN present? Whether jurisdiction is correct? Whether Section cited correctly. Whether SCN format, correct? Is the reasoning complete and specific? Track due dates, not just notices

- Step 2: If defective → Authorise a professional but retain oversight & File objection first

- Step 3: Only after objection → proceed on merits and

- Step 4: Retain proof of objection and maintain an internal GST Notice Register

8. Comparison: Section 160(1) vs 160(2) of the CGST Act

|

Aspect |

Section 160(1) of of the CGST Act |

Section 160(2) of the CGST Act |

|

Nature |

Protects the government from minor errors |

Penalizes taxpayer for participation |

|

Focus |

Administrative actions |

Proceedings following a notice |

|

Impact |

Notice generally stands |

The right to object is lost |

|

Correction possible? |

Yes |

No, once you participate |

The Golden Rule for GST Notices

Object first. Participate later. Or lose the right forever A safe reply structure Preliminary Objections (jurisdiction, validity, defects) then Statement: “Reply without prejudice to objections.” Thereafter, reply on merits (only if objections are rejected).

GST is notice-driven, and that movement of Portal silence is legally dangerous; Section 160(2) blocks late challenges. And Defects are not self-executing; the taxpayer must raise them, then Compliance discipline > litigation brilliance

- If a GST notice is defective, your silence equals acceptance. Object before participating or losing your rights forever. Section 160(2) of the CGST Act converts silence into consent In GST law, What you don’t read can still legally hurt you. The portal is the courtroom door and if you don’t show up, the case proceeds anyway.

- GST law doesn’t punish ignorance. It presumes awareness. It doesn’t wait for you to read. It waits for you to respond.

Practitioner-grade GST Notice Risk Matrix prevents irreversible damage under Sections 160(2), 73, 74, 75 & 169 of the CGST Act.

GST NOTICE RISK MATRIX:

GST Notice Risk Matrix prevents irreversible damage under Sections 160(2), 73, 74, 75 & 169 of the CGST Act. (Silence → Waiver → Finality → Recovery)

VERY HIGH RISK (Point of No Return Zone)

|

Type of Notice |

Legal Trigger |

Risk if Ignored / Mishandled |

Why Section 160(2) Hurts |

|---|---|---|---|

|

SCN u/s 73 / 74 |

Demand + penalty |

Ex-parte order, tax + interest + penalty |

Defective SCN deemed valid if not objected |

|

ASMT-10 |

ITC / return mismatch |

Best-judgment assessment |

Acceptance inferred by silence |

|

DRC-01 / DRC-01A |

Tax demand initiation |

Demand crystallises |

Later challenge barred |

|

REG-17 |

Cancellation SCN |

GSTIN cancelled |

Participation waives defects |

|

Summons u/s 70 |

Investigation |

Penal exposure |

Jurisdiction objections waived |

Action Window: 7–30 days : Golden Rule: Object first. Reply later.

HIGH RISK (Rights Start Shrinking)

|

Type of Notice |

Section |

Typical Trap |

Consequence |

|---|---|---|---|

|

ASMT-02 / ASMT-03 |

Provisional assessment |

Failure to seek hearing |

Unilateral finalisation |

|

DRC-06 / DRC-07 |

Final order |

Missed appeal window |

Demand becomes final |

|

GSTR-3A |

Non-filing |

Ignored reminder |

Best judgment order |

Action Window: 7–15 days and Mistake: Replying on merits without objections.

MEDIUM RISK (Recoverable Only with Cost)

|

Communication |

Risk |

What Goes Wrong |

|---|---|---|

|

System-generated intimations |

Misread as advisory |

Becomes SCN later |

|

Portal messages without email |

Ignored |

Service deemed valid |

|

Rectification order u/s 161 |

Missed correction window |

Error becomes permanent |

Action Window: 15–30 days, Cost: Litigation + pre-deposit.

|

LOW RISK (But Not Safe) : Item |

Risk |

Control Measure |

|---|---|---|

|

General alerts |

Complacency |

Weekly portal review |

|

Informational emails |

False comfort |

Portal overrides email |

Action Window: Ongoing Rule: Portal > Email > SMS

SAFE RESPONSE PROTOCOL (Must-Follow SOP)

- Step—IDENTIFY: Section invoked, Due date, Nature (SCN / Order / Intimation)

- Step—OBJECT (MANDATORY): Raise objections on jurisdiction, limitation, wrong section, natural justice, vagueness/DIN/service. Use the words “without prejudice.”

- Step—PARTICIPATE: Reply on merits only after objections, Attend hearing, Upload documents

- Step—TRACK FINALITY: DRC-07 issued? The appeal clock started. (3 months)

If GST taxpayers don’t object when they can, then they can’t object when it hurts. Create a GST Notice Register with Date of portal upload, Section, Due date, Objection filed. (Y/N), reply status, appeal deadline. This single register saves clients lakhs. Section 160(2) weaponizes silence. The GST portal is not passive storage. it is active legal service. Ignore it, and the law assumes. You saw it. You accepted it. You waived your rights. If you want next printable GST Notice Risk Matrix, Draft “Preliminary Objection” reply and cite case laws where silence killed strong cases. Internal SOP for firms.