Table of Contents

Validity of Partnership remuneration disallowed U/s 40A(2)(a)

Problem based on provisions of Sections 40(b)(v) & 40A(2)(a) of the Income Tax Act, 1961.

LETS see the applicability of provision of applicable of section.

- SECTION 40(b)(v) of income tax provides that: Remuneration to Partners exceeding the limit prescribed u/s 40(b) to be disallowed;

- SECTION 40A(2)(a) of income tax provides that deals with powers of disallowance of expenditure on related party by Assessing Officer.

Where the assessee incurs any expenditure in respect of which payment has been or is to be made to any person referred to in clause (b) of this sub- section, and the AO is of opinion that such expenditure is unreasonable or excessive having regard to the FMV of the services or goods, or facilities for which the payment is made or the legitimate needs of the business or profession of the assessee or the benefit derived by or accruing to him therefrom, so much of the expenditure as is so considered by him to be unreasonable or excessive shall not be allowed as a deduction under income tax act

Responses on above Queries:

Situation of this case are similar to the facts in CIT Vs. Great City Manufacturing Co, wherein the High Court found that:

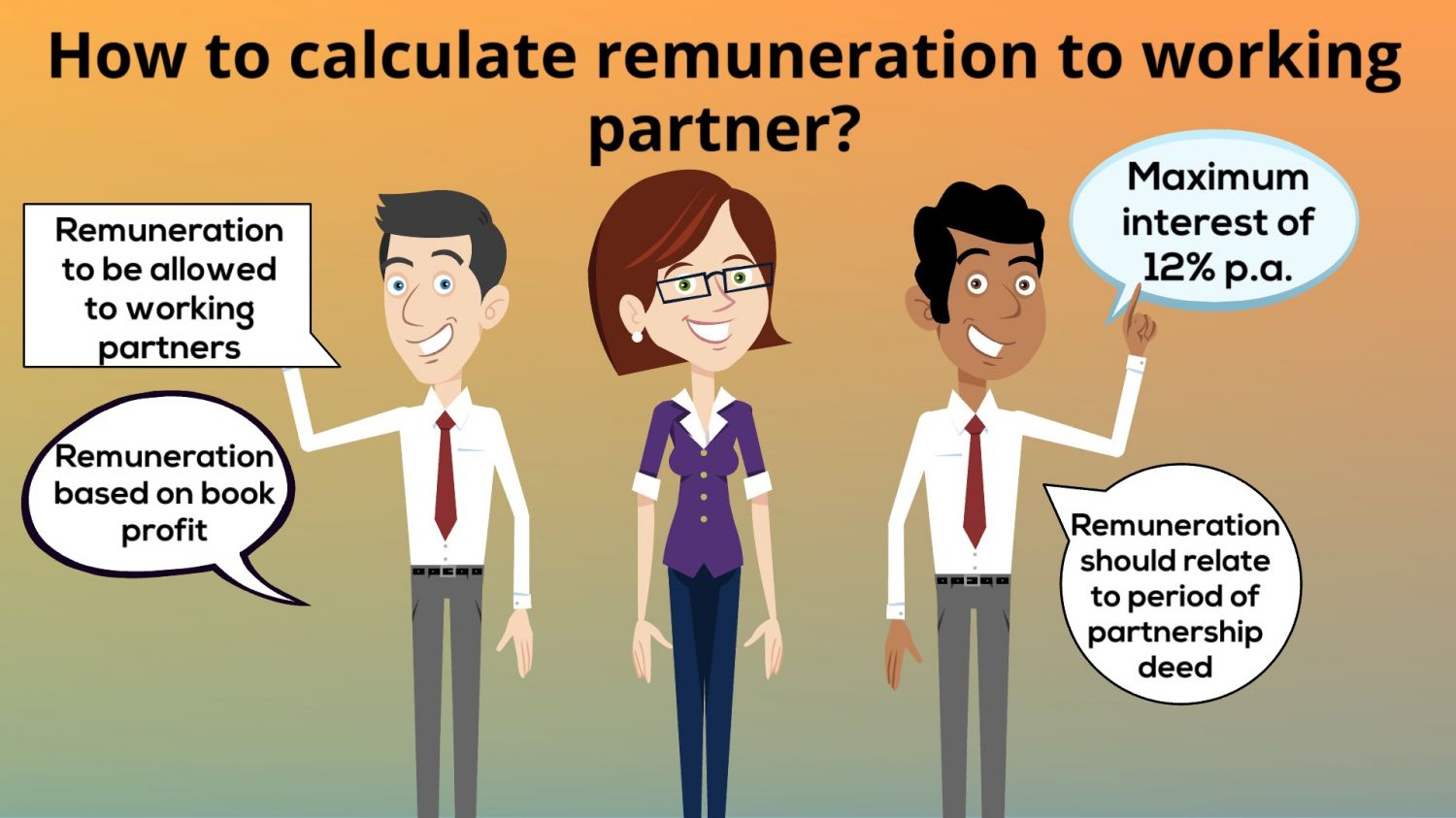

- U/s 40(b)(v) provide limit of remuneration to working partners of firm & deduction is allowable up to such limit while computing the business income.

Maximum amount of remunration or salary or bonus or commission or other salary to all the partners of partnership firm during the previous year must not cross limits specify below:

- On 1st INR 3,00,000/- of book profit or in case of firm having loss – INR 1, 50,000 or 90 percentahe of book profits (whichever is higher).

- On the balance part of book profit 60 percenatage of book profit.

- If partner remuneration paid is within the limit specified u/s 40(b)(v), then recourse to provisions of U/s 40A(2)(a) cannot be taken.

AO is needed to ensure that partner remuneration is paid to the working partners of the firm mentioned in Partnership Deed, the conditions & terms of the Deed stated payment of such partner remuneration to working partners & remuneration is within the limits specified u/s 40(b)(v) of the Income tax Act, 1961. If these provisions are complied with then the Assessing Officer cannot disallowed any part of remuneration on the ground that it is in excess or it is excessive.

From the point of view of specified above judgement, the increased partner remuneration, which is authorized by the Partnership Deed & is within limits specified U/s 40(b)(v) & paid to working partners, cannot be disallowed by invoking provisions of u/s 40A(2)(a) of the Income Tax Act, 1961.

- The action of Assessing Officer in above mentioned case was not appropriate. So we can conclude the below on further Analysis the provision of above section

Allowability of Remuneration and Interest to Partners: Under Section 40(b) of Income Tax Act :

- where salary or remuneration etc is allowable by the firm only to working partners as provided in the under section 40(b)(iii) However payment of interest which is not exceeding 12 percentage P. A is allowable to any partner whether is working or not, Because word any partner is specified in section 40(b)(iv) of income tax act.

- According to the explanation 1 to section 40(b) of income tax where an person is individual, and who is a partner in a partnership firm on behalf, or for the benefit, of any other person( means Partner in a representative capacity), and interest paid by firm to individual otherwise than as partner in a representative capacity shall not be considered for the objective of provision of section 40(b) of income tax act

- However, interest paid by the partnership firm to such person as partner of partnership firm in a representative capacity & interest paid by the firm to the person so represented capacity shall be considered for the objective of this clause under the income tax act.

- Moreover the Explanation 2 to section 40(b) of income tax act further specified that where an person is a partner in a partnership firm otherwise than as partner in a representative capacity in the firm, interest paid by the partnership firm to such individual will not be consider for the objective of this clause, if such kind of interest is received by him on behalf, or for the benefit, of any other person.

Conclusion:

Income tax Provision in relation to Remuneration and Interest to Partners under section 40(b): below team & conditions has been satisfied before claiming any kind of deduction in respect of remuneration & salary or interest payable to partner of partnership firm .

- Remuneration & Interest paid to the partner must be a working partner only

- Interest and Remuneration to Partners must be approved & authenticate by Firm Partnership Deed

- Partnership Deed must specify Quantification of remuneration to Partners

- No Remuneration & Interest to Partner of partnership firm to be allowed which relates to any specified period falling before the date of such partnership deed.

- Remuneration to Partners exceeding specified limit provide under section 40(b) of income tax to be disallowed

- Any kind of interest to any partner of partnership firm exceeding 12% is disallowed.