Table of Contents

- Foreign Remittance Compliance Update (effective 1 April 2026)

- Structural Changes In Foreign Remittance Forms & Law

- Key Practical Challenges In Foreign Remittance Compliance with Documentation & Legal Framework Changes

- Immediate Action Points For Foreign Remittance Compliance With Effective 1 April 2026:

- Key Changes In Foreign Remittance & Reporting Framework

Foreign Remittance Compliance Update (Effective 1 April 2026)

India’s foreign remittance framework is undergoing a major procedural shift under the Income-tax Act, 2025. While the new regime aims to streamline and digitize foreign remittance compliance, this creates significant transformation in foreign remittance compliance under the Income Tax Act, 2025, impacting both tax reporting and tax collected at source applicability. it also introduces higher accountability on professionals, stricter procedural discipline, and zero room for post-filing correction. Here’s what professionals and businesses must prepare for:

Structural Changes in Foreign Remittance Forms & Law

- Form 15CB → Form 146 (Accountant’s Certificate)

- Form 15CA → Form 145 (Remitter’s Declaration)

- Governed by Section 393 (replacing earlier Section 195 framework)

- Special Disclosure Opportunity : FAST-DS 2026 Scheme i.e . 6-month window for NRIs to disclose foreign assets & income with reduced penalties. so This reform is not just procedural—it fundamentally shifts compliance towards Pre-remittance validation, Higher accountability on professionals, Stricter reporting with zero-error tolerance

- This marks a foreign remittance complete overhaul of Tax deducted at source compliance on foreign remittances.

- INR 5 Lakh+ Remittance? CA Certification Mandatory: If total remittance exceeds INR 5 lakh (FY), then the taxpayer must obtain Form 146 (CA Certificate), which impacts freelancers, Startups & businesses, and high-value individual remitters.

- No Bulk Filing Facility allowed in Foreign Remittance: Each remittance requires separate online filing

- Pre-Remittance Foreign Remittance Compliance required : Foreign Remittance Forms must be filed before executing the remittance

- Detailed Reporting Introduced: Payments must now be classified into 65 specific categories and Improves traceability & audit trail

Key Practical Challenges in Foreign Remittance Compliance with Documentation & Legal Framework Changes

Key practical challenges in foreign remittance compliance with effect from 1 April 2026 are mentioned here under :

- Form 15CA/15CB replaced: Form 145 – Remitter’s Declaration

- Mandatory CA Authorization for Foreign Remittance: Clients must first authorize their Chartered Accountants on the portal before filing Form 146 , so Income tax Form 146 – Chartered Accountants Certificate (where applicable) : Governed by Section 393 (replacing earlier Section 195)

- Chartered Accountants Certification Requirement: Mandatory where remittances exceed INR 5 lakh (FY) and requires prior Chartered Accountants' authorization on the portal. Thereafter, the certificate (Form 146) must be filed before remittance.

Immediate Action Points for Foreign Remittance Compliance with Effective 1 April 2026:

We needed to ensure “Add Chartered Accountants” authorization is completed by clients, then Align internal systems for real-time compliance before remittance thereafter. Train teams on new Foreign Remittance forms & workflow changes

- Tax collected at source under the Liberalized Remittance Scheme – Major Changes : Threshold Increased INR 10 lakh per financial year (earlier INR 7 lakh) and revised tax collected at source Rates

- Education / Medical (Non-loan cases) : 2% TCS (above INR 10 lakh)

- Education via Loan (from financial institution) : Nil Tax collected at source

- Overseas Tour Packages : Reduced to 2% (earlier 5% / 20%)

- Other Liberalised Remittance Scheme Remittances (travel, gifts, investments, etc.) : 20% Tax collected at source beyond INR 10 lakh

- Tax Treaty Benefits → More Paperwork Earlier. TRC (Tax Residency Certificate) was often sufficient. Now mandatory filing of Form 41 and additional disclosures are required: contact details, Indian address , and declaration of completeness. So higher scrutiny on DTAA claims.

- Critical Compliance Facts for Foreign Remittance Compliance

- Threshold Limit Foreign Remittance: INR 5 lakh (unchanged)

- No Edit Facility during Foreign Remittance: Once Form 146 is filed, it cannot be modified

- Foreign Remittance form Withdrawal Window: Allowed within 7 days (subject to conditions)

- Penalty Exposure of Foreign Remittance: Up to INR 10,000 per certificate under Section 463

- Operational & Compliance Changes

- Fully Digital Reporting Ecosystem: End-to-end online compliance & tracking

- No Bulk Filing: Each remittance requires separate filing

- No Edit After Submission: Forms once filed cannot be modified

- Withdrawal Window: Allowed within 7 days (conditional)

- Penalty Exposure: Up to INR 10,000 per certificate u/s 463

Quick Takeaway related to Foreign Remittance Forms & Law

- More compliance in Foreign Remittance Forms & Law → Additional forms like income tax new forms 145, 146, 41, 44, 45

- More disclosures Foreign Remittance Forms & Law → Exact nature of payment, foreign tax IDs, and transaction purpose

- More verification: Foreign Remittance → Mandatory Chartered Accountant involvement

- More scrutiny foreign remittance → System-driven monitoring of global fund flows

- Cross‑border transactions / Foreign remittances are no longer just reported—they're tracked, verified, and analyzed end‑to‑end.

- No PAN? Conditional Relief for non-residents may file without PAN only if they are not legally required to obtain one. But reporting obligations remain fully intact Foreign Income & Tax Credit to tightened controls and structured reporting formats , possible CA certification for higher FTC claims. Focus on accuracy & consistency in global income reporting

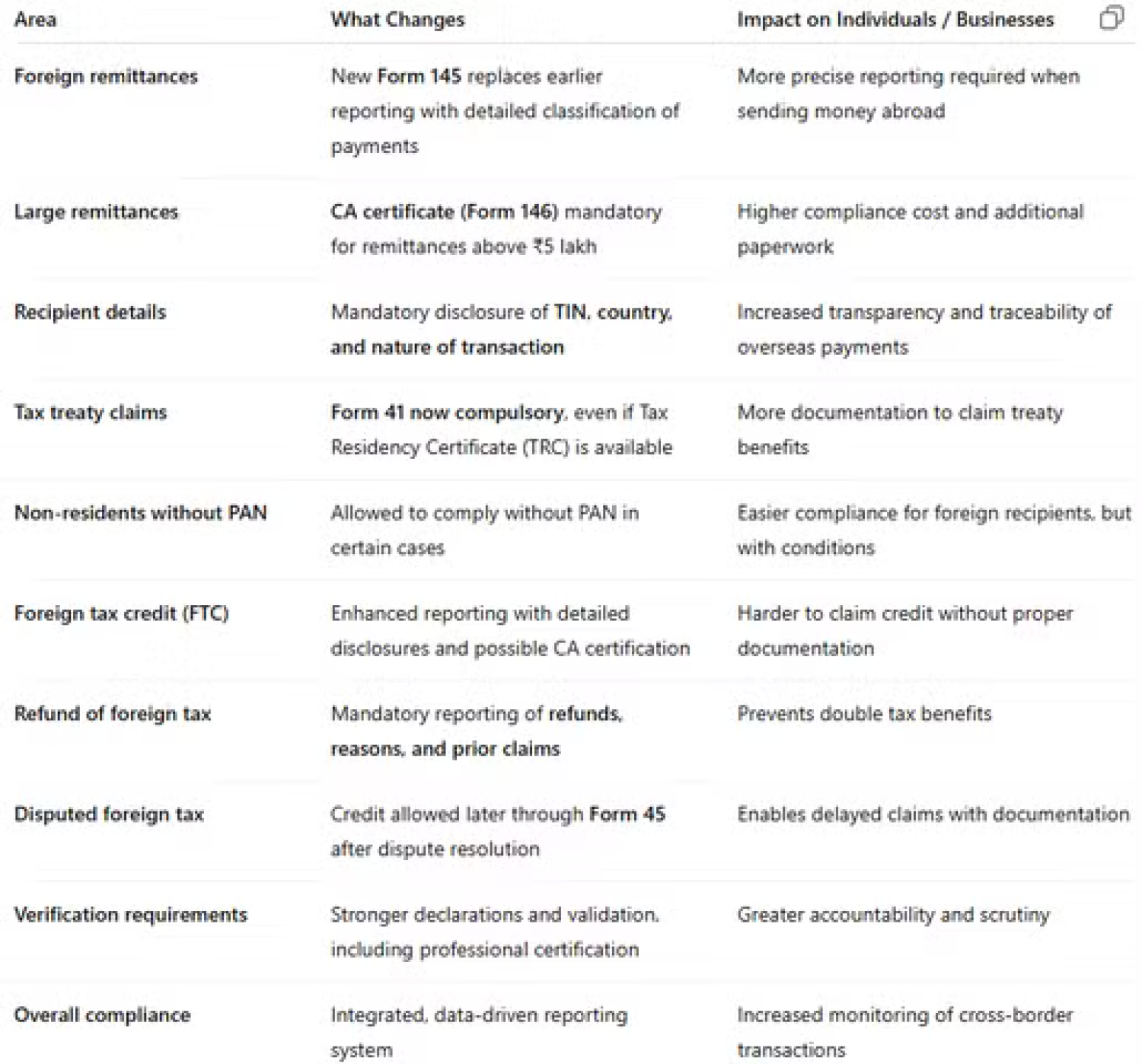

Key Changes in Foreign Remittance & Reporting Framework

| Area | What Changes | Impact on Individuals / Businesses |

|---|---|---|

| Foreign remittances | Form 145 introduced, replacing earlier formats with granular payment classification | More precise and detailed reporting while remitting funds overseas |

| Large remittances | CA Certificate (Form 146) mandatory for remittances above ₹5 lakh | Higher compliance cost and additional documentation |

| Recipient details | Mandatory disclosure of TIN, recipient country, and nature of transaction | Improved transparency and traceability of overseas payments |

| Tax treaty claims | Form 41 compulsory, even if TRC is available | Additional documentation burden to claim treaty benefits |

| Non‑residents without PAN | Compliance allowed without PAN in specified cases | Easier compliance for foreign recipients, subject to conditions |

| Foreign tax credit (FTC) | Enhanced disclosures and possible CA certification | FTC claims become stricter and documentation-driven |

| Refund of foreign tax | Mandatory reporting of refunds, reasons, and prior claims | Prevents double benefits and misuse of credits |

| Disputed foreign tax | Credits allowed later via Form 45 after dispute resolution | Enables deferred FTC claims with proper documentation |