Table of Contents

- How To Claim Hra Allowance, While Filing Income Tax Return?

- Who Is Qualified For The House Rent Allowance Exemption?

- Eligibility Requirements For House Rent Allowance Exemption

- How Can You Claim The House Rent Allowance Exemption On Your Income Tax Returns?

- If The Rent Receipts Are Not Obtained By The Employer:

How to claim HRA allowance, while Filing Income tax return?

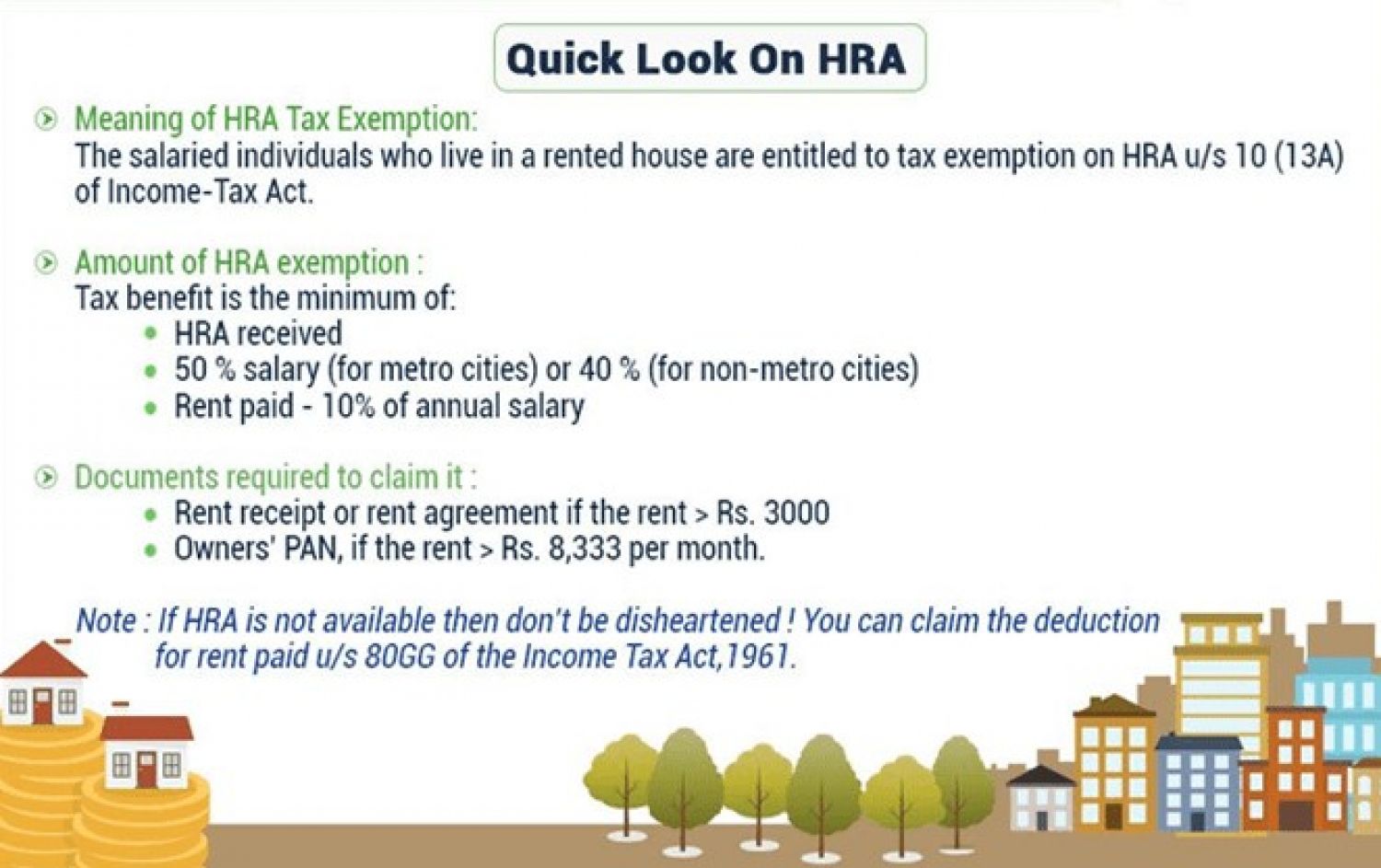

- HRA is one of the most significant benefits accessible to salaried workers (House Rent Allowance).

- You can utilise the HRA to partially or totally lower your tax liability if you are a salaried individual who lives in a leased home. The allowance is meant to cover the costs of renting a property.

- Your landlord could even be your parents in this case. If you do not live in your own house, however, the HRA is fully taxable.

- When submitting your tax returns, you can claim the HRA exemption.

- Only if your employer does not claim House Rent Allowance on your behalf is this possible.

- Here's how to claim House Rent Allowance exemption on your tax returns, step by step.

Who is qualified for the House Rent Allowance exemption?

- Salaried employees who receive a house rent allowance as part of their salary and make a payment toward the rent of the area they live in are eligible for House Rent Allowance exemption. The HRA exemption may completely or partially reduces taxable income.

- At the start of the fiscal year, the House Rent Allowance amount is reflected on the employer's tax forecast statement. Your company deducts the HRA from your compensation. When you file your ITR, you can see the deduction in Part B of Form 16 generated by your employer (Income Tax Returns).

- If you do not file your House Rent Allowance claim with your ITR, you can file an amended return before the end of the assessment year.

Eligibility requirements for House Rent Allowance exemption

Employee can get House Rent Allowance exemption only if.

- Your wage structure includes an HRA component.

- You’re a salaried worker.

- You are a tenant in a rented house.

If your employer does not provide House Rent Allowance, you may be able to claim a deduction under Section 80GG of the Indian Income Tax Act if you pay rent on any residential property you own. To be eligible for this exemption, however, you must meet specific criteria, such as:

- You’re either employed or self-employed.

- You did not get any House Rent Allowance during the tax year for which you are seeking 80GG deduction.

- You, your spouse, your HUF (if you are a member) or your minor child do not own residential property in the area where you now live, work or conduct business.

If you own residential property in a location other than those indicated above, you cannot claim the benefit of self-occupied housing. In this case, the other lodging would be considered rented, allowing you to claim the 80GG deduction.

How can you claim the House Rent Allowance exemption on your income tax returns?

- Insurance premiums are exempt from taxation under Section 80C of the Income Tax Act of 1961.

- Furthermore, any benefit received under the savings insurance policy is tax-free under Section 10 of the income tax department.

- Most employers will require you to submit your rent receipts in the final quarter of the fiscal year so that you can claim an HRA exemption on the Form 16 that the employer creates. If you don't give your employer your rent receipts, he or she will deduct TDS (Tax Deducted at Source) without taking HRA into consideration.

- In this case, you can still claim HRA exemption on your ITR. You'll have to calculate the exempt HRA amount by yourself.

If the rent receipts are not obtained by the employer:

- If you did not or could not submit your rent receipts to your employer, you can claim HRA exemption on your ITR. In this case, the HRA exemption would not have been included in the taxable wage, resulting in a higher TDS deduction.

- If you claim an HRA deduction on your ITR, the extra TDS will be refunded to you. However, you must calculate the exact HRA exemption amount and deduct it from your income.