Table of Contents

Annual Filing & Compliance of a Producer Company

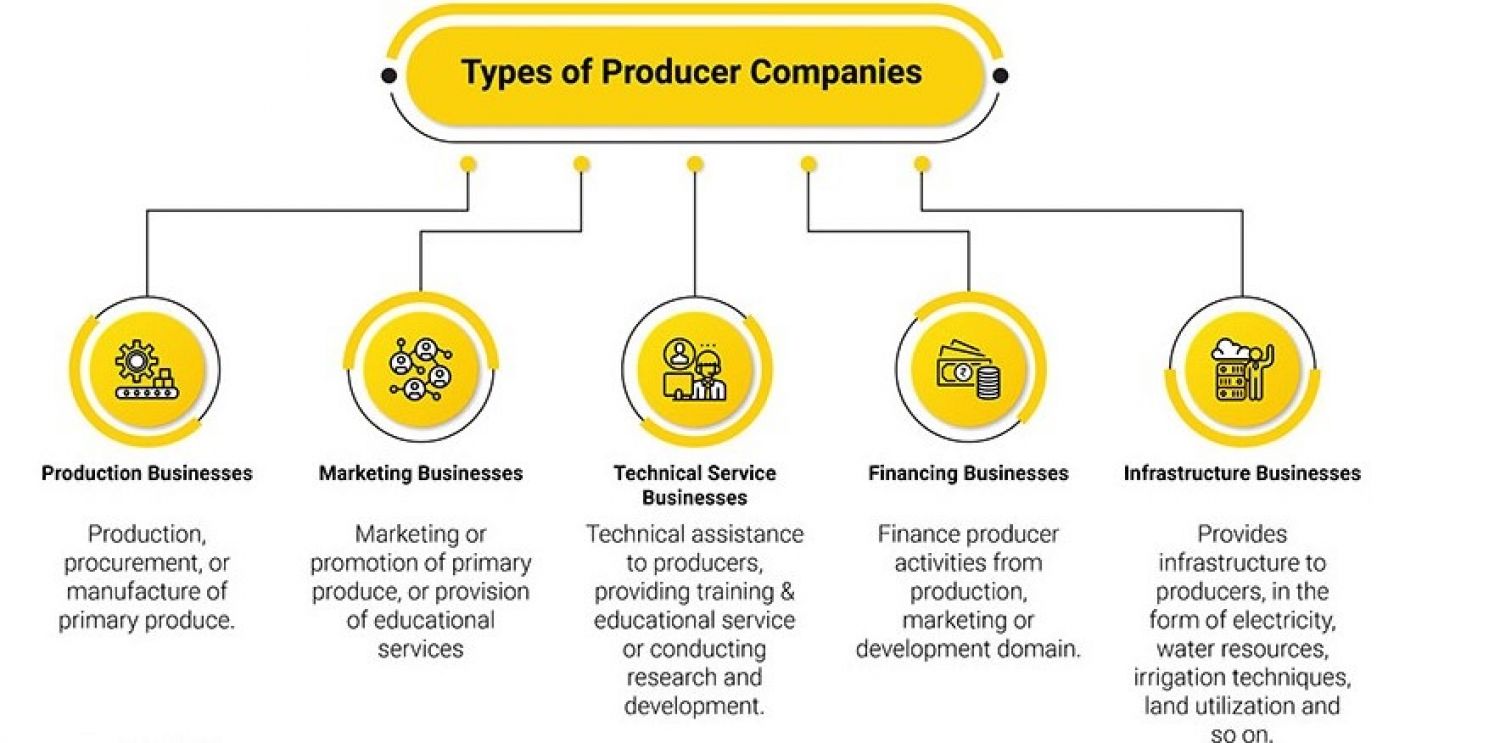

A Producer Company is a business registered under the Company Act 2013 with the aim of producing, harvesting, promoting mutuality techniques, etc. Like other registered companies, a producer company also needs to file compliance on a fair and annual basis in order to ensure a good legal status. Noncompliance may cause the government to punish you with varying degrees of penalties, ranging from the payment of the penalty fees to the closure of the company. These compliance requirements are therefore not voluntary, but compulsory. The following is the annual comply of the producer company:

- Hold the AGM in every financial year.

- Producer Company annual Return Filing,

- Producer Company Audit balance-sheet and P & L Accounts.

Yearly compliance management of a producer company

What is the compulsory Annual Company Compliance of a producer company?

-

·Preparation of Balance Sheet, Preparation of P & L Accounts

-

·Audit Report

-

·Auditor Appointment.

-

·Preparation & Filing of Form ADT-1 (Auditor Appointment).

-

·Director's Report

-

·Filing of e-form INC-20A.

Annual compliance with Producer Company:

The AGM of the producer company shall be held each FY. The gap between the 2 Annual General Meeting’s shall not exceed 15 months.

The 1st Annual General Meeting shall take place within ninety days of its incorporation, where the members adopt the articles of the Producer Companies and appoint the Board of Directors.

The below details shall be included in the notice of the Annual General Meeting:

- Previous AGM or EGM Minutes

- The names of the candidates to be elected.

- Agenda of the General Meeting

- The balance sheet is audited and the profit and loss accounts of the producer company and its subsidiary together with the BOD report.

- A motion for a resolution on the appointment of auditors

Financial Statements and Annual Returns

Each company shall need to submit its annual return to the Company registrar within 60 days of the Annual General Meeting in E-Form MGT-7. A company with a revenue of Rs 50 Cr or more shall be certified by the Practicing Company Secretary in the form MGT-8.

-

Preparation of Seven Registers: Registers to be maintained under the Companies Act, 2013

-

Preparation of Minutes of AGM

-

Filling of Form MBP- 1: Every Director of the Company in the First Meeting of the Board of Directors in each Financial Year needs to disclose his interest in other entities by filling the form. Fresh MBP-1 needs to be filed, whenever there is the change in his interest from the earlier given MBP-1

- Filling of Form DIR – 8: Every Director of the Company in each FY has to file with the Company disclosure of non-disqualification *ROF Fee (Approx INR 1000 Per FY ) for ADT-1, AOC-4 & MGT-7 Excluded.

- Preparation of 04 Minutes of Board Meeting: U/S 118 (10) of the Companies Act, 2013 requires every company to observe Secretarial Standards with respect to General & Board Meetings specified by the ICSI and approved as such by the Central Government.

- Income Tax Returns of the Company: All companies registered in India are required to file ITR each year on or before Sept. 30th.

- E-form: AOC-4: File Financial Statement: i.e Directors’ Report, BS along with Statement of Profit & Loss Account.

- E-form: MGT-7: File Annual Return within Sixty days of holding of AGM for the period 1st April to 31st March

- Use of DSC of Auditor in Form AOC- 4: Every Company is required to file its Financial Statements within Thirty days of its AGM with ROC in E-Form AOC-4. The same shall be digitally signed by one director and certified by Chartered Accountants /Company Sectary/Cost Accountant in Practice.

Punishments/ Penalties for producer company

Any default referred to below by the Directors of the Producer Companies shall be subject to the following penalty:

- Failure to convene AGM or other general meetings.

- Handover of the custody of the books of accounts

The Producer Companies may be punished by the fine of INR 1,00,000/-. If the default is in the nature of the continuation, the daily penalty of INR 10k will be levied until the default continues.

FAQ ON PRODUCER COMPANY

Q1- can a producer company have more than 15 directors?

Ans. Yes, a production company that has registered as inter cooperative society can have more than 15 directors.

Q2-can 2 directors in a meeting of the board can be considered as a quorum?

Ans.- no, the quorum of the meeting of the board must be 1/3 of the total no. of directors subject to a minimum of 3 directors.

Q3- what is the maximum tenure of holding the office of a director?

Ans.- the maximum tenure of holding the office of a director is 5 years.

Q4- is it mandatory to prepare minutes of the meeting of the committee of a producer company?

Ans.- yes, every minute of the meeting of the committee is prepared and placed before the meeting of board of directors.

Q5- what is the meaning of the special rights of the member?

Ans.- special rights means rights relates to additional produce by the member or any other rights relating to products that are given by the board.

Q5- can a member nominate a person after 1 year of becoming a member who will be the after his death?

Ans.-No, a member shall within 3 months of becoming a member nominate a person who will the member after his death.

Q6- Can a member still be a member after ceases to retain his qualification as per articles?

Ans.- No, after ceases to retain his disqualification the member needs to surrender his shares.

Q7- can a board surrender the shares of the member without giving any written notice to a member?

Ans.- No, the board needs to give written notice to the member of the producer company before the surrender of shares.