Table of Contents

GST RETURN FILLING:

- GST Return filling means return prescribed or required to furnished by or under GST Acts or by the rules made thereunder. A GST return is a completed document that has details of sale/revenue which a taxpayer is required to file with the GSTN authorities. This is used by tax authorities to calculate tax liability.

- Under GST, a registered dealer has to file GST returns that include:

- Output GST (On sales)

- Purchases

- Input tax credit (GST paid on purchases)

- Sales

- For GST return files or GST filing, GST compliant sales & purchase invoices are required. By GST Return filing there is the transfer of information to the tax administrator with the help of information tax liabilities is fixed. It provides necessary inputs for taking policy decisions. There is a separate return for a taxpayer registered under different states. A taxpayer is required to filed returns depending on the activities undertaken.

THRESHOLDS AND ELIGIBILITY CRITERIA OF MONTHLY GST RETURN IS TURNOVER EXCEEDED 1.5 CR

The thresholds and eligibility criteria mentioned by the India Government are to boost up and benefit small and medium enterprises (SME). These SMEs will contribute to the country’s GDP and will help in eradicating unemployment.

The taxpayers whose aggregate turnover during the preceding financial year exceeded Rs. 1.5 Cr or the new registrants who estimate their turnover to exceed Rs. 1.5 Cr during the current financial year, have to file a return on a monthly basis.

The taxpayers, whose aggregate turnover during the preceding financial year remained up to Rs. 1.5 Cr or the new registrants who estimate their turnover to remain up to Rs. 1.5 Cr during the current financial year, but who intends to file a return on a monthly basis, can also upload the invoices for the month of August 2017.

- FURNISHING DETAILS OF OUTWARD SUPPLIES: UNDER SECTION 37

Every registered person other than

- Supplier of OIDAR service

- Composition taxpayer

- A non – resident taxable person

- ISD

- The person deducting tax at source

- E-commerce operator who is required to deduct tax collection at source.

Different types of GST Returns

You can find below a list of all the GST Returns to be filed as applicable under GST Act along with due dates. GST return filings according to the CGST Act subject to time to time changes made by As per CBIC Notifications

In the FORM GSTR – 1 monthly or the part of the month required to file the return before the 10th date of the next month.

RETURN BY REGISTERED PERSON: UNDER SECTION 39 (1)

Every registered person other than

- Supplier of OIDAR service

- Composition taxpayer

- A non – resident taxable person

- ISD

- The person deducting tax at source

(f) E-commerce operator who is required to deduct tax collection at source.

In FORM GSTR – 3 monthly or the part of the month required to file a return before the 20th date of the next month.

Return is required to be filed even no supply has been made.

RETURN OF COMPOSITE TAXPAYER: UNDER SECTION 39(2)

- Composition taxpayers are required to file the quarterly return in FORM GSTR – 4 before the due date of the 18th of the next month of the quarter.

RETURN BY REGISTERED NON RESIDENT TAXABLE PERSON: UNDER SECTION 39(5)

- A registered non-resident taxable person required to file the monthly return in FORM GSTR – 5 before the due date of 20th of the next month or the 7th day after the validity of the registration, whichever is earlier.

RETURN BY OIDAR: UNDER SECTION 39(5)

- OIDAR is required to file the monthly return in FORM GSTR – 5A before the due date of 20th of the next month

RETURN BY ISD: UNDER SECTION 39(4)

- ISD is required to file the monthly return in FORM GSTR – 6 before the due date of 13th of the next month

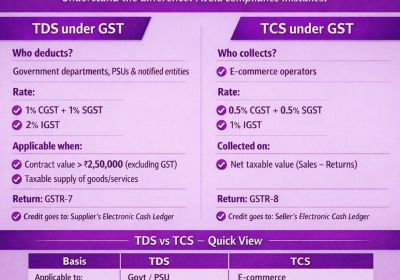

RETURN BY REGISTERED PERSON DEDUCTING TDS: UNDER SECTION 39(3)

- The registered person deducting TDS is required to file the monthly return in FORM GSTR – 7 before the due date of the 10th of the next month

RETURN BY ELECTRONIC COMMERCE OPERATOR: UNDER SECTION 52(4)

- Online E-commerce operator is required to file the monthly return in FORM GSTR – 8 before the due date of 10th of the next month.

ANNUAL RETURN: UNDER SECTION 44

All the taxpayers filing return in GST – 1 to GST – 3 are required to file an annual return:

Exception for filing annual return by the certain taxpayer –

- Casual taxable persons

- A non – resident taxable person

- Input service distributors and

- The person authorized to deduct and collect tax at source under section 51 and section 52.

- Any department of central government or a state government or a local authority whose books of accounts are subject to audit by the comptroller and auditor general of India or auditor appointed for auditing the accounts of the local authority under any of the law for the time being in force.

- The Return required to be filled by 31st December of the next financial year.

- The annual return is filed electronically in FORM GSTR – 9 through the common portal.

- The composition scheme supplier is required to file an annual return in FORM GSTR – 9A.

FINAL RETURN: UNDER SECTION 45

- Registered person is required to furnish the final return u/s 39(1) and whose registration either surrendered or canceled shall need to file a final return in FORM GSTR – 10 through the common portal.

NOTICE

- GST Authority may issue the notice in GSTR – 3A if a taxpayer fails to file the return. on receiving notice taxpayers must file returns along with the penalty within a period of 15 days.

- If a taxpayer even after receiving the notice did not file the return then his tax liability is assessed and uploaded on his GST Portal along with the penalty.

|

Return Form |

Description |

Due Date |

Frequency |

|

GSTR-1 |

Details of outward supplies of taxable goods or services affected. |

The due date is 11th* of the next month with effect from October until September. *last time, the due date was the 10th of the next month. |

Monthly |

|

|

|

End of Month next upcoming Quarter. |

Quarterly (If opted) |

|

CMP-08 |

challan cum Statement to make a tax payment by a taxpayer GST registered under the composition scheme U/s 10 of the central goods and services tax act, (supplier of goods) and CGST (Rate) notification no. 02/2019 dated 7th March 2020 (Supplier of services) |

18th of Month next upcoming quarter. |

Quarterly |

|

GSTR-4 |

Return for a taxpayer registered under the composition scheme under section 10 of the central goods and services tax act (supplier of goods) and central goods and services tax act (Rate) notification no. 02/2019 dated 7th March 2020 (Supplier of services). |

30th of Month succeeding an FY. |

Annually |

|

GSTR-5 |

Return for a non-resident foreign taxable person. |

20th of Next month. |

Monthly |

|

GSTR-6 |

This is a return for an input service distributor to distribute the eligible input tax credit to its branches. |

13th of Next month. |

Monthly |

|

GSTR-7 |

Return for Govt authorities deducting tax at source (TDS). |

10th of the next month. |

Monthly |

|

GSTR-8 |

Details of supplies effected through e-commerce operators and the amount of tax collected at source by them. |

10th of the next month. |

Monthly |

|

GSTR-9 |

Annual return for a normal taxpayer. |

31st December of next FY. |

Annually |

|

GSTR-9A |

Annual return to be filed by a taxpayer registered under the composition levy anytime during the year. |

31st December of next FY. |

Annually |

|

GSTR-9C |

Statement of Certified reconciliation |

31st December of next FY. |

Annually |

|

GSTR-10 |

Final GST Return to be filed by a GST taxpayer whose GST Registration is canceled. |

Within three months of the date of cancellation or date of cancellation order, whichever is later. |

Once, when GST registration is canceled or surrendered. |

|

GSTR-11 |

Details of inward supplies to be furnished by a person having UIN and claiming a refund |

28th of the month following the month for which statement is filed. |

Monthly |

|

GSTR-3B |

Simple return in which summary of outward supplies along with input tax credit is declared and payment of tax is affected by the taxpayer. |

Staggered^ from the month of January onwards* *Previously 20th of the next month for all taxpayers. |

Monthly |

|

^20th of next month for taxpayers with a Total sales/ receipt in Last more than INR 5 Crore. For the taxpayers with a Total sales/ receipt equal to or below INR 5 crore, 22nd of next month for taxpayers in category X states/UTs, and 24th of next month for taxpayers in category X states/UTs

|

|||

|

GSTR-2 Suspended from September onwards |

Information/details of inward supplies of taxable services and/or goods and/or effected claiming the input tax credit. |

15th of Next month.

|

Monthly |

|

GSTR-3 Suspended from September onwards |

Monthly return on the basis of finalization of details of outward supplies and inward supplies along with payment of tax. |

20th of Next month.

|

Monthly |

* Each & every Subject to changes by Orders/ Notifications.

**Statement of self-assessed tax by composition dealers – that is same as the erstwhile form GSTR-4, which is now made a GST Annual Return with effect from FY onwards.

Late Fees for Not Filing Time Return

- In case GST Returns is not filed on the due date, you will be liable for interest & late fees.

- Moreover, the interest rate is 18 percentage on annual basis. The taxpayer must measure the amount of the tax outstanding to be paid. Further time frame is from the next day of filing to the date of payment.

- Moreover, Late fees are Rs. 100 per day per Act. So it's INR 100 under CGST Act and INR 100 under the SGST Act. The total is going to be INR 200 per day. Which is Maximum up to is INR 5,000. There is no late fee for IGST Act.

Due to GSTR Return

Relief in GSTR compliance

- All businesses to file GSTR-1 and GSTR-3B till March 2018.

- GSTR-2 and GSTR-3 filing dates for July 2017 to March 2018 will be worked out later by a Committee of Officers

- Turnover under Rs 1.5 Cr to file quarterly GSTR-1

- Turnover above Rs 1.5 Cr to file monthly GSTR-1

- All businesses to file GSTR-3B by the 20th of next month till March 2018.

Extension of GSTR-1 filing Due Dates

- Filing of GSTR-1 for the tax period of August 2017 and onwards is likely to commence soon. In the meantime, such taxpayers can upload the invoices for August, September, October 2017 to avoid the last-minute rush.

- All other taxpayers liable to file GSTR-1 shall upload the invoices and file GSTR-1 for the quarter ending September 2017 after the option to file the same is available on the portal. The taxpayers eligible to file a return on a quarterly basis but have already filed the return for the month of July 2017, shall have to upload the invoices of August and September jointly and have not to include the invoices of July month again.

- The taxpayers who have not filed GSTR-1 for the month of July, are advised to file the same quickly as they will not be able to file GSTR-1 for the remainder of the quarter (August-September) till they have filed GSTR-1 of July.

Businesses with an annual turnover of up to 1.5 crores will submit quarterly returns. Taxes will be paid quarterly. Due dates of filing GSTR-3B for August to December – 20th of Next Monthly

In case you are confused about GST as a business owner, feel free to consult the GST experts at Rajput Jain & Associates. You can get comprehensive assistance on GST Registration online and GST Return Filing. You can also use our GST compliance software for doing end-to-end GST compliance.

FAQ ON GST RETURN FILING:

Q. 1 – Weather taxpayers can file GSTR – 1 before the end of the current tax period?

Ans. - No, a taxpayer cannot file GSTR – 1 before the end of the current tax period.

Q. 2 – Definition of tax period?

Ans. – Tax period means the period for which the return is required to be furnished.

Q. 3 – Is there is any extension of GSTR – 1?

Ans. – Extension may be granted as permitted by the commissioner.

Q. 4 – Is there is an exception to file GSTR – 1 before the end of the current financial year?

Ans. - Yes, the following are the exceptions –

- Casual taxpayer

- Cancellation of GSTIN of a normal taxpayer.