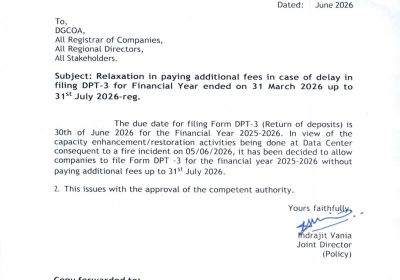

MCA Extends DPT-3 Filing Due Date to 31 July 2026

MCA Extends DPT-3 Filing Due Date, Extends DPT-3 date, MCA Extends DPT-3 Filing Due Date to 31 July 2026, Companies may file Form DPT-3 for the financial ...

Read MoreUnder the Companies Act 2013 there are various requirement and lot of filings required to be undertaken with the Registrar of Companies. To provide a quick of view of such filings, we have compiled the list of requirements under which various filings has to be done. Apart from the filing requirement, the list of documents that are required to be filed is also available.

Every Company must fulfil the requirements as specified in the companies act 2013, otherwise the company has to face various actions from Registrar of companies like payment of late fees, disqualification of directors, company strike off etc.

Registrar of companies has the power to close the companies or disqualify the directors of the companies in case the company is not fulfilling the compliances requirements of the company as specified in the companies act 2013.

We have provided the list of annual compliances as applicable to private and public companies.

The following are the benefits of annual compliances :

| Form /Event | Time limit | Explanation |

| First Board Meeting | within 30 days of Incorporation of the company | Every Company is required to Conduct the First Board meeting of the company within 30 days of its Incorporation |

| Appointment of first Auditor | within 30 days of the Incorporation of the company | Every Company is required to Appoint the first auditor of the Company within 30 days of the Incorporation of the company |

| Subsequent Board Meeting | At least 4 in every financial year | Every Company is required to conduct at least 4 Board meetings in every financial year. The gap between two Board meetings shall not exceed 120 days. |

| Form INC-22 | Within 30 days of incorporation | Every Company is required to file with the registrar of companies Form INC 22 for verification of registered office of the company. |

| Form NC-20A | within 6 months of incorporation | Every Company is required to file with the registrar of companies Form INC-20A before Commencement of business of the company |

| Disclosure of interest of directors | First Board meeting after appointment and thereafter in every first board meeting held in every financial year and whenever there is a change in the disclosure already made, in the Board meeting held thereafter. | Every director shall disclose the interest of the director in Form MBP-1. |

| Annual General meeting | First Annual General meeting – within 9 months of closure of the first financial

year Subsequent Annual General meeting - within 6 months of closure of the financial year |

Every Company is required to conduct one Annual General meeting in every financial year |

| Form PAS-6 | Within 60 days of each half of financial year | Every unlisted public company shall file with the Registrar of companies a reconciliation of audit report in form PAS - 6 |

| Form AOC-4 | Within 30 days of the Annual General meeting of the company | Every company is required to file Form AOC – 4 in every financial year |

| Form MGT-7 | Within 60 days of the Annual General meeting of the company | Every company is required to file with the registrar of companies the Annual return in Form MGT-7 in every financial year |

| Form ADT-1 | Within 15 days of Annual General meeting of the company | Every company shall after the appointment of Auditor in the Annual General meeting of the company is required to file with the registrar of companies Form ADT-1 with the registrar of the company |

| Form MGT-8 | Required to be attached in Form MGT-7 by prescribed companies |

shall be required to get a certificate from a practicing company secretary and attach it in form MGT-7 |

| Form MGT-9 | Required to be attached in Form AOC-4 | Every company is required to file with the registrar of companies the extract of annual return in Form MGT-9, which is required to be attached in Form AOC-4 |

| Form BEN-2 | Within 30 days of receipt of form BEN – 1 | Every company which has received information from registered owner in Form BEN-1 is required to file with the registrar of companies form BEN-2 with Registrar of companies |

| Form DPT-3 | Upto 30th June every year | Every company is required to file with the registrar of companies form DPT-3, the information related to deposit or particulars of transactions not considered as deposit or both |

| Form DIR-3 KYC / web based KYC | Upto 30th September every year | Every company is required to file with the registrar of companies Form DIR – 3 KYC or do web based KYC of every director of the company |

| Form MSME | Upto 31st October / 30th April | Every company having outstanding payments to MSME’s is required to file with the registrar of companies Form MSME in each half of the Financial year of the company |

| Minutes of meetings | Every company is required to maintain minutes of Board meetings and general meetings held in the company |

| Form /Event | Time limit | Explanation |

|---|---|---|

| Form DIR-12 | Within 30 days of appointment / resignation / change in designation of director | Every company is required to file with the registrar of companies form DIR – 12 for appointment / resignation / change in designation of director of the company |

| Form PAS - 3 | Within 30 days of allotment of shares (Within 15 days of allotment in case of private placement of shares) | Every company is required to file with the registrar of companies form PAS – 3 for allotment of shares |

| FORM SH-7 | Within 30 days of approval from shareholders | Every company is required to file with the registrar of companies form–SH-7 for increase in authorised share capital of the company |

| Form MGT-14 | Within 30 days of approval from shareholders | Every company is required to file with the registrar of companies form MGT -14 for change in objects of the company |

| Form INC - 24 | Within 60 days of new name approval but After approval of Form MGT-14 | Every company is required to file with the registrar of companies Form INC – 24 for change in name of the company |

| Form CHG - 1 | Within 30 days of creation / modification of charge | Every company is required to file with the registrar of companies form CHG -1 for creation / modification of charge of the company. |

| Form DIR - 3 | As and when Director identification number is required | Every company is required to file with the registrar of companies Form DIR -3 for obtaining Director identification number. |

New : Checklist Point for Completing the Annual Compliance for Private Start-ups Company :

A start-up which operates as a private limited company must comply with the characters laid down in the various statutes and other administrative bodies. This included, but are not limited to, regular filing of tax as well as other returns, accommodation of board and other meetings, management of approved books of account, etc.

We offer all kinds of Consultancy and Compliances Services in relation all kinds of companies. We have empanelled various experts to provide the expert advisory and Compliances services for all types of companies.

The services that we offer includes the following:

200+

550+

2009

700+

What is Annual Return?

Filing of an Annual return is a mandatory for all companies in India. Return must be filed with the MCA along with the necessary documents. Filing of an annual return with the dept. of Income Tax (IT dept.) is different from filing an annual return with the MCA.

What information is needed in the annual return?

Annual return consists in an Annual return i.e.

Who should sign the Annual Return?

The Annual return of the Company must be signed by the Directors of the Company and certified by CA / CS / CMA. The financial statements filed along with the Annual return must be audited and signed by a Chartered Accountant.

When is the due date for filing Annual Return?

Annual return in Form MGT-7 is required to be filed within 60 days of Annual general meeting of the company

What is the procedure for an Annual Return filing?

Annual return can be prepared and submitted electronically through the Ministry of Corporate Affairs (MCA) E-Filing portal with the help of Professional. Rajput Jain & Associates Financial Expert can assistance you in e-filing the annual return of your company.

Annual return under the Companies Act, 2013: each company shall prepare a return (hereinafter referred to as the annual return) in Form No. MGT-7 containing the information as it stood at the end of the financial year.

Excerpt of an Annual return: An excerpt of an annual return in Form No MGT-9 will form part of the Board 's report.

Annual return filing: each corporation shall submit a copy of the annual report with the Registrar. For a period of 8 years from the date of filing with the Registrar shall kept the copies of all annual returns, certificates and documents required to be affixed.

What is the penalty for non-filing of annual return?

If any Company fails to submit an annual return with the ROC within the prescribed time limit, the Company shall be liable for payment of the penalty until return is filed. The penalty amount will depend upon the number of days in default until the default runs on.

What is the expected due date for the an Annual return filing?

Annual return is expected to be filled before 6 months from the end of the financial year, or by September 30th. For newly established company, an annual return should be filed with the Ministry of Corporate Affairs (MCA) and an Annual General Meeting (AGM) should be held within 18 months from the date of establishment or 9 months from the date of closing of financial year, whichever is earlier.

MCA Extends DPT-3 Filing Due Date, Extends DPT-3 date, MCA Extends DPT-3 Filing Due Date to 31 July 2026, Companies may file Form DPT-3 for the financial ...

Read More

Risk-Based Physical Verification by MCA , MCA Form Consolidation, ROC Form Consolidation, Companies (Incorporation) Amendment Rules, 2026, SPICe+ & DIN Reforms, Registered Office & Verification, Flexible Address Proof (Rule 25 ...

Read More

Roll out a new auditing regime aligned with global standards, 40 auditing standards proposed by NFRA. India’s New Audit Regime, Standard on Auditing 600, principal auditors ...

Read MoreWe are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

All the information related to any client is considered confidential and never be disclosed to anyone.

Having years of experience in respective areas and backed by skilled and experienced workforce keep us ahead.

We believe in the building the good relationship with the clients that ensures the great impression.

If you are not happy with our services then you can request a refund within 30 days.

We provide 24*7 supports through phone, email and live chat.

You can pay online through EMIs, PayPal, net banking, debit card, credit card and more.

We are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

© 2016 Rajput Jain & Associates. All Rights Reserved | Sitemap