Project Financing > CIBIL Report

What is CIBIL?

CIBIL (Credit Information Bureau of India Limited) is the India's first credit information bureau. A credit bureau is a repository of credit information of all customers of its members, which comprises banks and financial institutions. CIBIL is one such organization that collates credit information contributed by its members and disseminates it to lenders, helping them in their credit-decision-making and lending process. In addition to above activities it also maintains account of settled loans and credit card for 7 years to come.

Why you should be concerned about CIBIL?

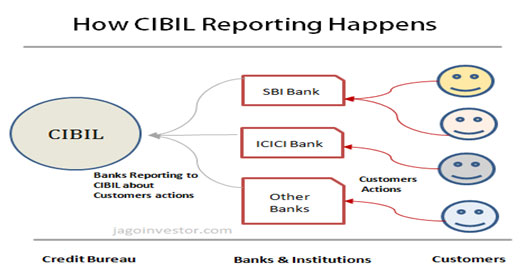

CIBIL is Credit Information Bureau of India Limited, which acts like a central repository of credit information in India. As many as 500 different banks and financial institutions are CIBIL’s clients and they report each of their customers (like me and you) actions to them. CIBIL is the India's first credit information bureau. A credit bureau is a repository of credit information of all customers of its members, which comprises banks and financial institutions.

So if you take a credit card from ICICI Bank, then ICICI bank reports to CIBIL about it. If you enquire about car loan to HDFC Bank, hold your breath! as even that enquiry is reported to CIBIL, if you can’t pay your EMI for home loan with SBI Bank for a particular month, that also gets reported to CIBIL.

Not just your bad actions, but even your good actions like paying EMI’s on time, paying credit card with punctuality also gets reported with CIBIL. You can see that this way, a history is maintained at CIBIL for each person, which can be good history or bad history depending on the case and this information is very useful for banks to decide if they want to give loan to you in future or not. All the banks are now looking at CIBIL report before taking the decision.

What is the CIBIL Credit Report?

Credit Information Report (CIR) is a report card of factual records provided by member group to the CIBIL. Credit grantors are leading Banks, State Financial Corporations, Non-Banking Financial Companies, Financial Institutions, and Credit Card Companies, Housing Finance Companies, who are Members of CIBIL. Its purpose is to help credit grantors make informed lending decisions – accurately and speedily at better terms. Are you looking to check your credit score and want to know why your loan application was rejected? Yes, if you are misusing your credit taking capacity, you are being watched at like never before in this country. I am talking about CIBIL here and in this article let me show you how your current behaviour related to credit card, personal loan, home loans are going to affect you in future in a good and bad way. Also see 2 real life cases where a person’s loan application got rejected because of Bad CIBIL report and how they didn’t even knew about it.

Good and bad credit Report

CIBIL report is not always bad. It’s an extremely good concept which is now taking shape in India recently. If there are two people A and B and A is a good guy and B is a bad guy, obviously A should get better rates of interest, faster processing, first right to loan. Whereas, guy B should get loan at higher rate of interest (because he is risky) and may be banks can even deny entertaining him at all.

CIBIL gives us the power to build our credit report. So if you become responsible and use your credit effectively and with planning, you can build a good credit history with CIBIL, which will help you in long run. Also note that taking a lot of loans without having the capacity is also a negative thing and that can affect your credit report.

You have to be super sensitive and careful with credit card and loan repayment, because one small mistake or being lazy in this area can cost you a lot. I would like to share some instances of readers who faced a lot of issues in area of getting loans and finally they checked their CIBIL report and found that they were having bad history

How to get your CIBIL Report

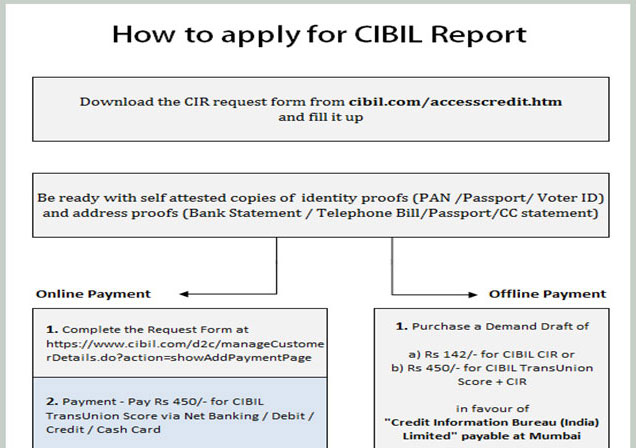

A borrower can now access his CIR directly from CIBIL. :- A CIR is a record of the credit payment history compiled from information received from credit institutions. The purpose is to help credit institutions make informed lending decisions - quickly and objectively - and enable faster processing of credit applications to help provide quicker access to credit at better terms. In order to get the report, one needs to fill up a requisition form available on CIBIL's website (www.cibil.com). After filling the form, you have to provide self-attested copies of some documents to CIBIL. The documents needed with the application are identity proof and address proof.

There are two kinds of reports which you can get from CIBIL. The basic one is called CIR Report which is nothing but a basic information on how is your credit history and what kind of information is there with CIBIL . The fee for obtaining the CIR is Rs 142.It must be paid through a demand draft favouring 'Credit Information Bureau (India) Ltd.', payable at Mumbai and sent to CIBIL. The documents can be sent either through email, post or fax. On receiving the documents and fees, CIBIL will process the request and send a copy of the CIR. This is good enough if you just want to check your status with CIBIL. You can also apply for your CIBIL Report Online

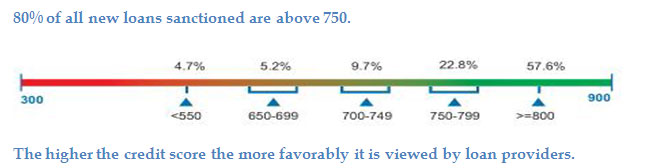

The second thing which you can get from CIBIL is your Credit Score which is called as CIBIL Trans Union Score and ranges from 300 – 900. This is number which scores your credit ranking. A lower number means your credit score is bad and you will be considered as Risky! If it is 900, you are doing great, Higher the better. The cost of CIBIL Trans Union Score along with your CIR report would be Rs 450. I would say this is not at all expensive if you can get this vital information at such a cost. If you are facing any rejection for loans or if you fear that your past history can haunt you, then it’s a good idea to check the CIBIL report each year and find out how it looks like. I have created a step by step procedure for you on how to apply for CIBIL report. Have a look

With the new base rate system of interest rates coming into effect, it would be all the more beneficial for home loan borrowers. The interest rates will henceforth be based on the base rate plus a premium depending on the credit rating of the borrower. A good credit rating helps in getting a loan at a lower interest rate as compared to a loan based on a bad credit rating.

The CIBIL Advantage!

Your credit score plays a critical role in the loan approval process. Your credit score gives loan providers an indication of your capability to pay back a loan, based on your Credit Information Report (CIR). However, it is important to note that every loan provider, that uses the CIBIL TransUnion Score, has its own benchmark of what constitutes a "good" score. For example, a score of 670 may be an adequate score for some loan providers, but reason enough to reject a loan application for some others.

Your CIBIL CIR is provided to you along with your score purchase, because it is the basis on which your credit score is generated. It's a record of your credit history, compiled from information received from loan providers, who are members of CIBIL.

How to get your CIBIL TransUnion Score

- Complete the Request Form Payment - Pay र 450 for the CIBIL TransUnion Score via Net Banking / Debit / Credit / Cash Card

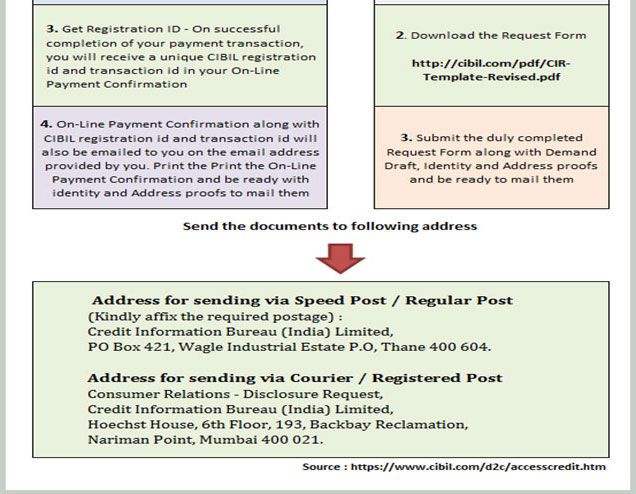

- Get Registration ID – On successful completion of your payment transaction, you will receive a unique CIBIL registration ID and transaction ID in your online payment confirmation

- Authentication - Answer 5 questions about your loans & credit cards to authenticate your application(Do keep your personal details and loan/credit card details ready)

- If authentication is successful: You'll receive your credit score and credit report at the e-mail address you have provided.

- If authentication is unsuccessful: Print the online payment confirmation and mail it along with your identity and address proofs (check the options given below) to the address mentioned below.

Documents Required along with the online payment confirmation in cases of unsuccessful authentications:

- Online Payment Confirmation

- Identity Proof - PAN / Passport / Voter's id (Identity proof should be valid and not expired)

- Address Proof - Bank Statement / Electricity Bill / Telephone Bill / Passport / Credit Card Statement (Address proof should be not more than 3 months from the date of application and should be in your name)

- Demand Draft - CIBIL Trans Union Score (including CIR) OR only CIR :

- Purchase a Demand Draft (DD) of 450/- for CIBIL TransUnion Score + CIR OR 142/- for CIBIL CIR in favour of "Credit Information Bureau (India) Limited" payable at Mumbai.

- Download the Request form

- Submit the duly completed Request Form along with Demand Draft, Identity and Address proofs to any one of our below mentioned address

Notes :- Address: Consumer Relations - Disclosure Request, Credit Information Bureau (India) Limited, Hoechst House, 6th Floor, 193, Backbay Reclamation, Nariman Point, Mumbai 400 021

Submit the duly completed CIR Request Form along with demand draft, identity and address proofs and send it to the address mentioned in the site http://www.cibil.com/accesscredit.htm. Remember CIBIL has no authorised agents. Please do not contact anyone other than CIBIL in order to gain access to a copy of your Credit Information report.

Can you fix the CIBIL report have wrong Information?

A lot of times Banks makes mistakes in CIBIL Report and it is mostly manual mistakes or lot of times delay in communicating the details. If you check your CIBIL report and find out any problems, please ask your bank to communicate it to CIBIL as soon as possible. Also if based on your CIBIL report, if you clear some loans , make sure you ask your bank to communicate to CIBIL that you have cleared the liabilities , so that it can get updated in CIBIL report. CIBIL report is your lifeline for future, don’t do anything which makes its dirty, else that will affect you in long run.

You can access your Credit Information Report (CIR) directly from CIBIL. As you may be aware, your CIBIL CIR is a factual record of your credit payment history compiled from information received from credit grantors. The purpose is to help credit grantors make informed lending decisions - quickly and objectively, and enable faster processing of your credit applications to help provide you speedier access to credit at better terms.

What CIBIL'S Credit Report Includes?

Name and address of borrower Identification and PAN numbers Passport details Date of birth Records of all the credit facilities availed by the borrower Past payment history Amounts overdue Number of inquiries made on that borrower by different members Suits filed and their status The CIR does not contain Income and revenue details Amounts deposited with banks Details of assets Details of investment. Now, individuals can access their credit information as analyzed by CIBIL. In case of any mistakes, they can be rectified.

Previously, a borrower used to get credit information from the bank where he applied for the home loan. A home loan application was liable to be rejected on account of negative or poor scoring by CIBIL. Lenders never provided the CIR to borrowers. Once a borrower found out that the credit information was incorrect, on his request, the lender would provide him a nine digit unique borrower control number. With the control number, the borrower was supposed to contact CIBIL to get the exact details related to the negative or poor scoring details. Many times, due to wrong reporting by member organizations, it was found that the CIBIL report was incorrect. In order to get the mistakes rectified, the borrower had to go through a long process.

Is CIBIL the only credit bureau in the country?

As of September 2008, CIBIL is the only credit bureau in India. But some other credit bureaus are planning to set up in India soon.

Where does CIBIL get the information from?

All leading banks and financial institutions are members of CIBIL. CIBIL collects information from these Members, collates and disseminates it in order to create a truly comprehensive snapshot of a borrower's credit history.

When is a credit facility classified as 'default'?

CIBIL IS not FOR classifying any accounts as default accounts or any borrowers as defaulters. It merely reflects this information after the Member has classified. The Number of Days Past Due and / or Asset Classification as per RBI definition as submitted by Members is reflected in the CIBIL Credit Report.

Does the CIBIL Credit Report indicate if credit should or should not be given?

The CIBIL Credit Report only submitted by CIBIL members and does not provide any indication or comment pertaining, to whether credit should or should not be granted. The credit grantors who have received an application for credit will make their own credit decision depending on their risk management policies. CIBIL does not grant or deny credit.

On what ground does CIBIL provide a credit report?

CIBIL is a repository of credit information and in the consumer ground it provides information on the various loans availed of and cards held by an individual from a member bank. Its commercial report covers the credit availed of by non-individuals.

How is a credit report helpful to credit underwriters?

The credit report shows account information such as repayment record, defaults, type of loan, amount of loan, etc. of the customer. This information facilitates prudent decision-making when the credit underwriter processes the loan/credit-card application.

Is it possible a customer’s name be removed from CIBIL’s database?

A customer’s name cannot be removed from CIBIL’s database because member banks contribute to CIBIL on a monthly basis data of all their customers who maintain a loan/credit-card account with them.

If a loan is denied to a customer by one bank on the grounds of the CIBIL report, will it be denied by other banks too?

Approval or rejection of a credit application depends on the bank’s policies. Rejection by one bank on the grounds of the CIBIL report might not imply rejection by another bank.

If a customer’s family member has defaulted, will it affect the customer’s status in CIBIL’s records?

The CIBIL report has information of loan/credit details of the borrower only. Therefore, for a retail customer, it would not matter if someone in his/her family has defaulted. If the customer’s repayment track record is okay, his/her credit score will not be affected by that of his/her family members.

Can you fix the CIBIL report have wrong Information?

A lot of times Banks makes mistakes in CIBIL Report and it is mostly manual mistakes or lot of times delay in communicating the details. If you check your CIBIL report and find out any problems, please ask your bank to communicate it to CIBIL as soon as possible. Also if based on your CIBIL report, if you clear some loans , make sure you ask your bank to communicate to CIBIL that you have cleared the liabilities , so that it can get updated in CIBIL report. CIBIL report is your lifeline for future, don’t do anything which makes its dirty, else that will affect you in long run.

Does it affect your loan application?

Yes. CIBIL rating affects your loan application in different ways. CIBIL report will show the details of all the loans taken by you. It will also show details such as your regularity in paying back the loan -details of installments due but not cleared on time etc Applicants who have defaulted earlier in paying back their loan installments will be easily caught and their loan application will be rejected.

Does every bank have CIBIL check?

Of course yes. All lending institutions will check CIBIL reports so that they can take firsthand information about your credit history. Not only banks, anybody interested in checking your credit history can access your information from CIBIL by paying a small fee.

How can I improve my CIBIL rating/ Credit History?

You can improve your credit score by repaying your loan EMI’s on time and always pay the minimum payment on your credit card to avert from the bad credit score. Remember Below Points to Maintain Good Credit History

- Always pay your bills on time. Late payments are viewed as the negative guidance on your financial status.

- Keep the loans and credit card balance low. It shows that you are financially well able to manage without need of many loans. This gives positive guidance to the banks to offer loans.

- Also have the mix of credits like loans, credit cards, etc. For example, having multiple credit cards for one person doesn’t look for your financial status. Even if you have multiple cards, use only one card will show that you don’t depend on multiple credit cards.

- If you paying the loans through EMI, don’t miss any of the EMI. It is advisable to auto-deduct from the bank account (nowadays this method only used by each loan). Keep checking that you have enough money in the bank account to pay the monthly EMI. If the EMI is returned, it will adversely affect your reputation with the bank and reflect in the credit history.

- Also, you have to be very careful when taken the joint-loan and paying the money together. If your co-applicant is not correct, that will affect you. You need to monitor your co-applicant that he pays the money on time.

- It shows good when you prepay the loan before the actual tenure. If you are prepaying the home loans or auto loans before the actual completion date, it will reflect as you are financially sound and good in closing the loan account. Bank will not fear on default payments from you.

- Review your credit history periodically to ensure that everything is proper on your name. Sometimes banks may not upload the data or miss something.

You can request CIBIL for the Credit Information report (CIR). This report will show the complete details of your credit history.

What Rajput Jain & Associates Offers

We provide a start to end solution with regard to CIBIL Report.