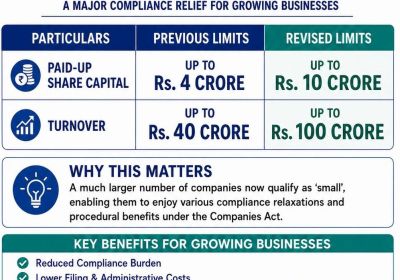

Change in Small Co. Limits: Major Compliance Relief for Businesses

paid-up capital limit from INR 4 crore to INR 10 crore and the turnover limit from INR 40 crore to INR 100 crore, MCA increased the limits of small ...

Read MoreA joint venture is a tactical partnership where two or more people or companies agree to put in goods, services and/or capital to a uniform commercial project.A joint venture is a new enterprise owned by two or more participants. Though, the joint venture represents a newly created business enterprise, its participants continue to exist as separate firms. A joint venture can be organized as a partnership firm, a corporation or any other form of business organisation which the participating firms choose to select.

Setting up A Joint Venture Registration can be complex.

We can make this simple & Hassle Free

Step by step assistance

For Indian & foreign companies/ other person

Our services are quick & affordable

In sectors where 100 percent FDI is not allowed in India, a joint venture is the best medium, offering a low risk option for companies wanting to enter into the vibrant Indian market. For any successful JV into India, compatibility is important for both the parties. To maintain a successful joint venture in India both of the associated parties should have a long term goal and conditions should be written in the clauses in JV.

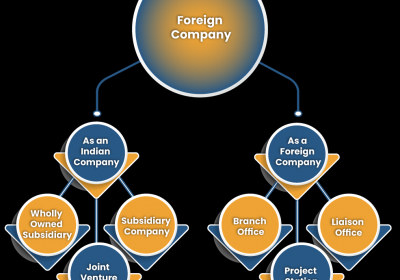

Foreign Companies can set up their operations in India by forging strategic alliances with Indian partners.

Company

Unincorporated

A foreign company can invest in an Indian company through a joint venture agreement (or as a wholly owned subsidiary) in the areas which are otherwise not reserved exclusively for the public sector or which are not under the prohibited categories such as real estate, insurance, agriculture and plantation. Foreign investment into India is governed by the Foreign Direct Investment (FDI) policy and the Foreign Exchange Management Act, 1999 (FEMA).Foreign investments into India, a two tier approval has been provided.

FDI in sectors or activities to the extent permitted under automatic route does not require any prior approval either by Government of India or Reserve Bank of India (RBI). The investors are only required to notify the Regional office concerned of RBI within 30 days of receipt of inward remittances and file the required documents with that office within 30 days of issue of shares to foreign investors.

FDI in activities not covered under the automatic approval route requires prior Government approval and are considered by the Foreign Investment Promotion Board (FIPB).The FIPB has been set up in the Ministry of Finance to promote inflows of FDI into the country, as also to provide appropriate institutional arrangements, transparent procedures and guidelines for investment promotion and to consider and approve/recommend proposals for foreign investment.

A joint venture company in India is like any other Indian company for the purposes ofIndian Companies Act, Indian Income Tax Act and other applicable laws, rules andregulations.. Regarding approvals for the participation of aforeign company in India, permissions and approvals will be required from the ReserveBank of India or Foreign Investment Promotion Board (FIPB), as the case may be.

Approvals of composite proposals involving foreign investment or foreign technical collaboration are also granted on the recommendations of the FIPB. The companies having foreign investment approval through FIPB route do not require any further clearance from RBI for receiving inward remittance and issue of shares to the foreign investors.The proposals to FIPB shall contain the following information:-

For Setting up Joint Venture of foreign company in India. We adopt a transparent method of pricing which is fixed and certain and same to all our customers. We do not have any discount policy. Our expertise in Setting up Joint Venture of foreign company in India is well known in India and outside India. We have helped many originations of all size and sector. We can also help in the following areas:

200+

550+

2009

700+

Why Joint venture option can be choice by entrepreneur?

Joint venture companies are mainly the chosen form of corporate houses for doing business in India. There are no separate laws for joint ventures in India. The companies registered in India, even with up to 100 percent overseas equity, are considered the same as local companies. A JV may be with any of the business entities existing in India.

Entering into a JV in India

Choosing of a good home partner is the most important tool to the success of any joint venture. Once an associate is selected, normally a memorandum of understanding (MoU) or a letter of intent is signed by the parties stressing the foundation of the future joint venture agreement.

An MoU and a joint venture agreement must be marked after consulting a chartered accountants firm well versed in the Foreign Exchange Management Act, Indian Income Tax Act, Indian Companies Act, international laws and applicable Indian rules, regulations and procedures.

Terms and conditions should be properly assessed before signing the contract. Negotiations need an understanding of the cultural and legal background of the parties. The JV union should be a subject matter to obtaining all required governmental approvals and licenses within specified period.

What are the Joint venture methods in India?

| Equity joint venture | Contractual joint venture |

| The equity joint venture is an understanding whereby an independent legal entity is created in accordance with the agreement of two or more parties. | The contractual joint venture might be used where the organization of a detached legal entity is not needed or the creation of such a separate legal entity is not feasible. |

Where one or more legal methods are used in the founding of the joint venture company to execute its operations is based on the partnership between the parties, the results of which reproduce in the joint venture agreement entered into between the parties. The licensing agreement, know-how agreement, technical services or technical assistance agreement, royalty payment , franchise agreement and agreement including all other profit-making matters including use of intellectual property rights normally form annexes or attachments to the main joint venture agreement. They can be signed simultaneously or after the joint venture company is recognized. |

|

Can remittances be made to acquire Joint Ventures abroad?

With effect from August 05, 2013, this Scheme can be used by Resident individuals to set up Joint Ventures (JV)/ Wholly Owned Subsidiaries (WOS) outside India for bonafide business activities within the limit of USD 125,000 subject to the terms & conditions stipulated in FEMA Notification No.263.

What are the basic considerable point while considering as JV?

Pre-incorporation due diligence

Management

Tax consideration

Intellectual property rights

Royalty payments

Profit repatriation

Removal of the condition of prior approval in case of existing joint ventures/technical collaborations in the same field

Human resource

Exit strategy

What is the Foreign Direct Investment policy on Venture Capital Fund (‘VCF’) and Venture Capital Company (‘VCC’)?

FDI up to 100 per cent is permitted for venture capital activities subject to capitalization norms. Registered Foreign Venture Capital Investors are allowed to invest in domestic venture capital undertaking or in a venture capital fund through the automatic route, subject only to SEBI regulations and sector specific caps on FDI.

Foreign Direct Investment (FDI) is permitted under the following forms of investments:

Is it mandatory to furnish Annual Performance Reports (APR) of the overseas JV/WOS based on its audited financial statements?

What are the penalties for non-submission of Annual Performance Reports (APRs)?

Delayed submission/ non-submission of APRs entail penal measures, as prescribed under FEMA 1999, against the defaulting Indian Party:

Is any recent Example of Joint Ventures in India?

Following are recent joint ventures in India

paid-up capital limit from INR 4 crore to INR 10 crore and the turnover limit from INR 40 crore to INR 100 crore, MCA increased the limits of small ...

Read More

Highlighting the advantages of GIFT City & Services, Advantages of GIFT City, NRI in GIFT City, Why NRIs Should Consider GIFT City, Investment Opportunities in GIFT ...

Read More

Functions & Features of Wholly Owned Subsidiary in India, Minimum criteria Pre-Conditions of 100% Wholly Owned subsidiary, Incorporate Wholly Owned Subsidiary in India,

Read MoreWe are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

All the information related to any client is considered confidential and never be disclosed to anyone.

Having years of experience in respective areas and backed by skilled and experienced workforce keep us ahead.

We believe in the building the good relationship with the clients that ensures the great impression.

If you are not happy with our services then you can request a refund within 30 days.

We provide 24*7 supports through phone, email and live chat.

You can pay online through EMIs, PayPal, net banking, debit card, credit card and more.

We are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

© 2016 Rajput Jain & Associates. All Rights Reserved | Sitemap