All about Provisional Attachment of Property GST

Page Contents

Cases where Provisional Attachment of Property U/s 83 of CGST Act can be Initiated

Commissioner can freeze your bank account and attach your property if the Taxpayer and Any Person who commits any offence and the Commissioner wants to protect the government’s revenue, he has the power to attach the taxpayer’s property and bank account provisionally under Section 83 of the CGST Act.

-

Concept of Property Attachment

When the government seizes a person’s property, that individual is unable to transfer it to anybody else. Even if he is successful in transferring the associated property, the transfer will be void and thus unenforceable. He will not be able to move his funds to any other account, even if bank accounts are associated.

Under Section 122(1a) of the CGST Act:

- Provisional Attachment and Bank Property can now be made against the Taxable Person and any other person.

- The Provisional Attachment can be made against the property and bank account of a person who is causing to commit and maintaining the profit of four listed offences.

4 kind of Offences cover as per the CGST Act:-

- Input Tax Credit on the basis of Input Service Distributor wrongly distributed.

- Issuance of Invoice without supply of Services/Goods.

- Supply of Services/Goods without Invoice.

- Input Tax Credit wrongly availed or Utilized without actual receipt of Goods/Services.

- Also, read this article:-

TDS & GST on Google or FB Ad words advertisements

HSN & SAC CODES ALONG WITH GST RATE

As per CBIC Guidelines issued Via Circular No: – 359, on Feb 23, 2021 have issued & it have provide Six Parameters

- Supply of Goods/Services without Tax Invoice (Cash Sale)

- Availing Credit on such Invoice or utilizing such wrongful availed credit

- GST collected but fails to pay beyond three months from Due Date.

- Erroneous Refund is being taken.

- Fake Invoice i.e Issuance of Tax Invoice without supply of Services/ Goods.

- Passing on the input Tax credit to recipient & that GST tax has not been deposited with Govt.

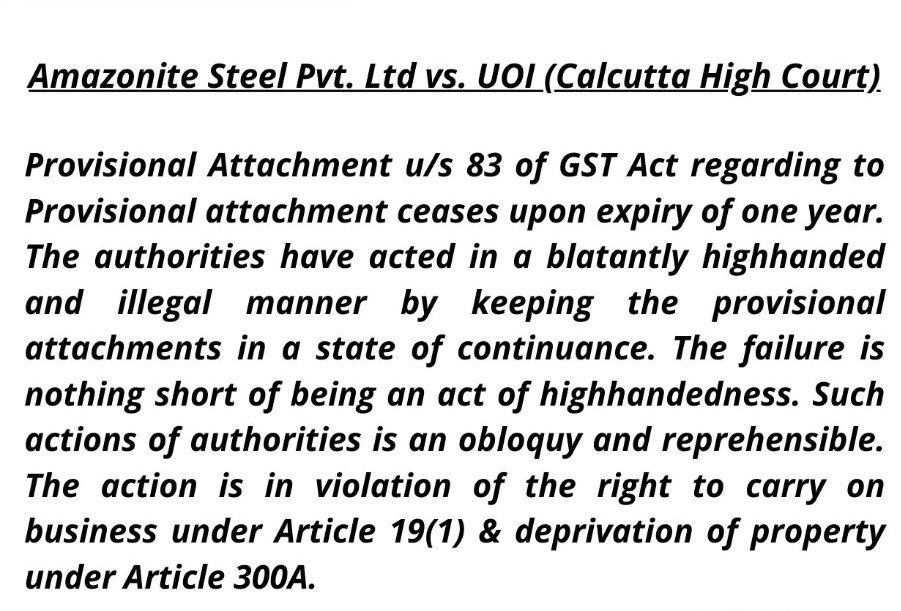

Its indicates that proper checking and verification, as well as this provisional attachment power, should not be employed as a mechanical/standard approach. If it needs to be attached, attach immovable property first, then moveable property; however, the commissioner cannot attach finished goods or raw materials when attaching movable property, and he should not disturb the business. If a business is halted and is not allowed to proceed, it is halted, and this is not mentioned in the statute.

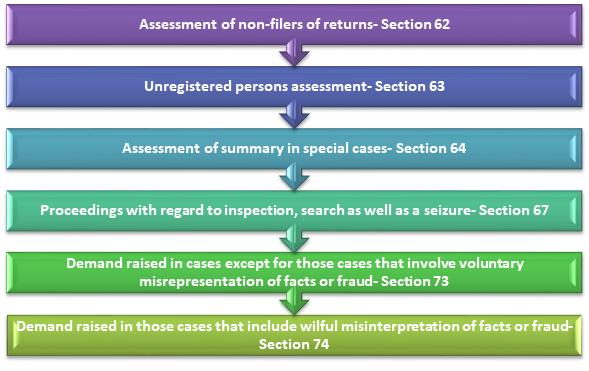

State of Affairs in Which Section 83 can be put into effect

At the time of the pendency of the proceedings given below, Section 83 could get invoked-

- Under Section 62:- Deals with Assessment of Non- Filers of Returns (Registered)

- Section 63:– Deals with Assessment of Unregistered Persons.

- Under Section 64:- Deals with Summary assessment in certain special cases.

- Section 67:- Deals with proceedings related to search, inspection and seizure

- Under Section 73:- Deals with Demand raised when tax not paid or short paid or erroneously refunded in other than fraud, willful misrepresentation of facts

- Section 74:- Deals with Demand raised when GST not paid or erroneously refunded or short paid in case of willful misrepresentation of facts or fraud.

- Also, read this article:-

All about Provisional Attachment of Property GST

Key GST Compliance Calendar for 2022

Invoice Furnishing Facility (IFF) Under QRMP Scheme

Analysis of Provisions of issue of Summon Under GST

Our Comments :

- If the Taxpayer is harassed in the form of illegal search, seizure, and detention, or illegal Provisional Attachment, we believe it is because the Commissioner is granted the power “REASON TO BELIEVE,” which is not stated anywhere in the Act.

- There should be a thorough check system in place to see if a commissioner is using his power correctly. If not, the Commissioner should be sanctioned, and the taxpayer should be compensated; the Commissioner should not be harassing the honest taxpayer in this manner.

- There is a provision in the Union Budget that has yet to be notified. Section 83(1), which gives the commissioner the ability to seize the property and bank accounts of taxable persons and anyone else, should be repealed before it takes effect. To protect government revenue, the government should begin actions under section 78 (Demand and Recovery), since if it begins processes under section 83, it will stifle business and harass honest taxpayers.

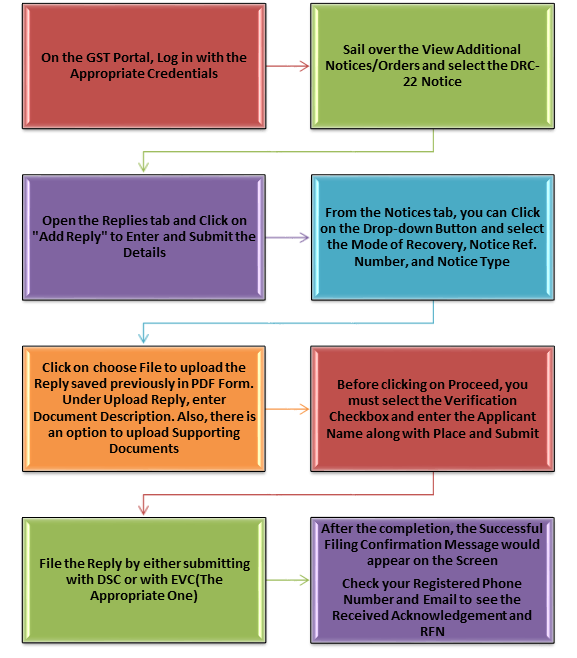

Step-by-Step Guidance for Filing a Reply to Notice in DRC-22

- As a prerequisite, have the response to the notice filled out and saved in a PDF prepared file. The format is not specified in any way. However, it should be verified that the file size does not exceed 5 MB.

- The steps to responding to a notice in DRC-22 form on the goods and service tax site are outlined below.

- In a nutshell, the purpose of provisional attachment of property under GST (Section 83) is to defend the revenue’s interests. Our GST experts at RJA will be at your disposal if you require expert advice on concerns relating to the Provisional Attachment of Property under GST.

What is CBEC Guidelines for Provisional Attachment under section 83 of CGST ACT

GST Officer will Give “Reasonable Time” to explain the GST Mismatch between returns.

- The government has declared that before beginning recovery action for short payment or non-payment of taxes, GST officers will give firms “reasonable time” to explain any discrepancies between GSTR 1 and GSTR 3B.

- Furthermore, if the said businessman fails to reply within the time limit or fails to explain to the satisfaction of the Officer the reasons for the short payment or non-payment of tax, then proceedings under section 79 of the CGST Act 2017 would be commenced.

- This Instruction was sent to Officers in response to concerns expressed by the business sector when Section 75 was modified on January 1st, allowing GST officers to initiate immediate recovery action where the monthly payment of GSTR 1 Return indicates more sales than GSTR-3B.

- CBIC through Instruction No. 01/2022-GST dated 07.01.2022 issued guidelines for recovery proceedings under u/s 79 of the CGST Act, 2017 in cases covered under explanation to section 75(12) of the CGST Act

CBEC Guidelines for recovery proceedings section 79 of the CGST Act,201

Popular Articles :