HSN & SAC codes alongwith gst rate

HSN & SAC CODES ALONGWITH GST RATE

- HSN codes: Basically HSN stands for a harmonized system of nomenclature. This harmonized system of the nomenclature coding system is developed by the World Customs Organization.

- Now This is a global standard of the Nomenclature of normal trading goods in foreign trade.

- The harmonized system of nomenclature is the codification of all tradable commodities into twenty broad sections with each and every chapter containing commodities of the same kind of nature.

- Its normal vision of classifying goods from all worldwide in a systematic & logical way. It is a 6th digit uniform code that classifies more than 5k products & is accepted globally.

- This HSN code is a set of defined regulations used for GST taxation objective in identifying the GST Rate of tax apply to a product in a Nation.

HSN codes of goods along with the rate of IGST, CGST, SGST mention in the below link

What is a harmonized system of nomenclature (HSN) classification?

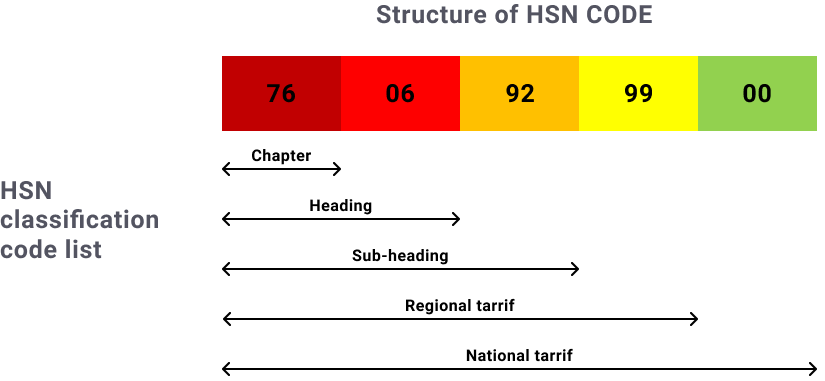

HSN(harmonized system of nomenclature) have twenty-one sections, ninety-nine chapters, 1,244 headings, & 5,224 subheadings. Sections & chapters are arranged in order of a product’s degree of manufacture/ in terms of its technological complexity.

Natural products like animals & vegetables appear in earlier sections; man-made/technologically advanced products like machinery appear later.

Chapters have a similar structure. Take cotton, for example – Chapter 52. Cotton that has not been carded or combed appears earlier in the chapter; cotton as a woven fabric appears later.

- Each Section is a collection of various chapters. Sections represent a broader class of goods, and chapters represent a particular class of goods.

- Each chapter is further divided into various headings depending upon different types of goods belonging to the same class.

- Each heading contains products, which are ultimately assigned an HSN code.

- For better identification of goods, India and a few other countries use eight-digit codes for deeper classification.

- few HSN codes also use dashes. A single dash (-) at the beginning of a description denotes an article that belongs to a group covered under a heading.

- A double dash (–) indicates that the article is a sub-classification of the preceding article that has a single dash. Similarly, a triple dash (—) or a quadruple dash (—-) indicates the article is a sub-classification of the preceding article that has a double dash or triple dash.