New Environmental, Social & Governance SEBI Compliance

Page Contents

India Imposes New Environmental, Social And Governance Compliance Reporting Requirements: SEBI Reporting

- New environmental, social, and governance (ESG) reporting standards have been implemented for the top 1,000 listed firms in India by market capitalization.

- The Securities and Exchange Board of India (SEBI) mandates that the information be disclosed in a new format called the Business Responsibility and Sustainability Report (BRSR) (BRSR).

- BRSR reporting will be optional For FY 2021-22 but it will be required compulsory for FY 2022-23,

Benefits of implementing ESG principles

- There has been a rise in investor knowledge of ESG issues, prompting them to seek out assets that are more sustainable. Several firms, including “Nike” and “Volkswagen,” have been driven to alter their supply chains as a result of these investors’ participation.

- ESG investment generates better returns, according to the study, because companies with a higher “Sustainability Rating” are less risky to invest in due to improved operational performance.

- With the growing relevance of ESG in India, investors will benefit not just from improved long-term returns, but also from a significant positive influence on the environment.

- Extreme climate change-related natural disasters can be avoided, reducing environmental and societal hazards significantly. There will also be an increase in Sustainable Finance, which refers to financial services that include ESG criteria into their business and investing decisions, benefiting both investors and the environment as a whole.

- It supports long-term development and economic efficiency, as well as helping to improve and restore ecological systems.

India’s new ESG policy imposes disclosure requirements.

- BRR (Business Responsibility Reporting) and CSR (Corporate Social Responsibility) reporting constrained ESG reporting in several ways. The top 1000 listed firms by market capitalization submit a report (as part of their annual report) to Indian stock exchanges. The deadline is May 2020.

- The Business Responsibility and Sustainability Report (BRSR) was designed by the Committee on Business Responsibility Reporting, and it was recommended that it be connected with the MCA21 portal.

- The framework is based on the “National Guidelines on Responsible Business Conduct’s” nine principles (RBC Guidelines).

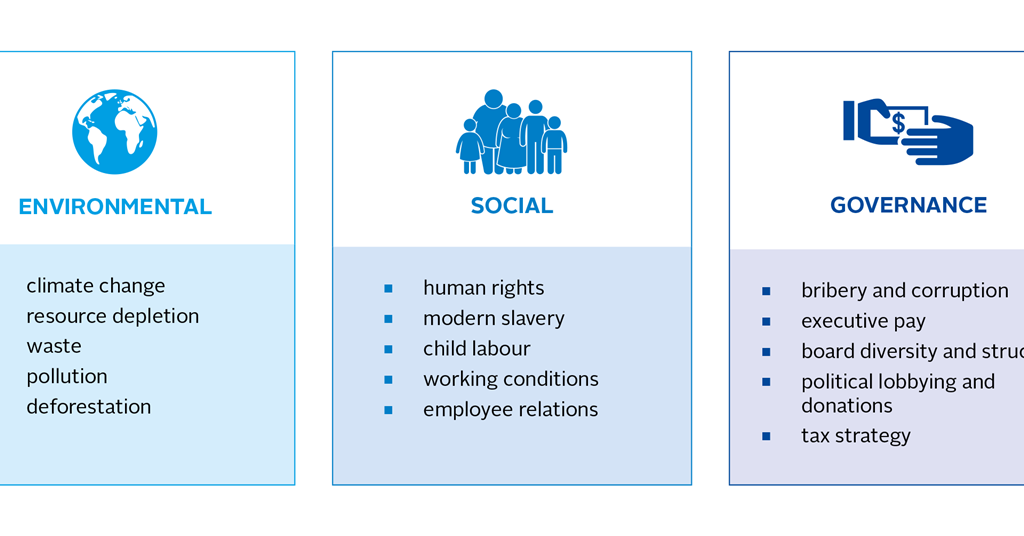

ASPECTS-GOVERNANCE

Disclosure requirements:

a) Training on the principles stipulated in the “National Guidelines on Responsible Business Conduct” (RBC Guidelines) for members of the Board, senior managers, and employees

b) Anti-corruption and anti-bribery policies

c) Awareness programs conducted for value chain partners on the principles in the RBC Guidelines

Principles:

- Businesses should conduct and govern themselves with integrity, and in a manner that is ethical, transparent, and accountable.

CONSUMERS

Disclosure requirements:

a) Product labeling

b) Product recall

c) Consumer complaints with respect to data privacy, cyber security, etc.

Principles:

- Businesses should engage with and provide value to their consumers in a responsible manner.

ASPECTS-ENVIRONMENT

Disclosure requirements:

a) Resource usage (energy and water) and intensity metrics

b) Air pollutant emissions

c) Greenhouse gas emissions (Scope 1, Scope 2, and Scope 3)

d) Waste generated and waste management practices

e) Impact on biodiversity

Principles: Businesses should respect and make efforts to protect and restore the environment.

ASPECTS-SOCIAL EMPLOYEES

Disclosure requirements:

a) Gender and social diversity, including measures for differently-abled employees

b) Turnover rates

c) Median wages

d) Welfare benefits to permanent and contractual employees

e) Occupational health and safety

f) Trainings

Principles:

- Businesses should respect and promote the well-being of all employees, including those in their value chains.

- Businesses should respect and promote human rights.

ASPECTS-GENERAL

Disclosure requirements:

a) Overview of the company’s material environmental, social, and corporate governance risks and opportunities and approach to mitigate or adapt to these ESG risks as well as relevant financial implications.

b) Sustainability related goals and targets and related performance

c) Management structures, policies, and processes related to sustainability

Principles: General management and process disclosures

COMMUNITIES

Disclosure requirements:

a) Social impact assessments

b) Rehabilitation and resettlement

c) Corporate social responsibility

Principles:

Businesses should promote inclusive growth and equitable development.

The Securities and Exchange Board of India has issued a consultation paper proposing to implement same-day settlement (T+0) & instant settlement on an optional basis in Indian stock market in 2 phases. The capital market regulator has stated that shorter settlement cycles will be added to the current T+1 cycle while also inviting public comments on the issue on the matter.

Conclusion

- The new reporting rules encourage listed firms in India to provide transparent, uniform disclosures on ESG metrics and sustainability-related risks and opportunities.

- This strategy will assist organizations in better demonstrating their sustainability aims, position, and performance to the market, resulting in long-term value creation and improving investors’ capacity to make educated ESG-related decisions.

- BRSR reporting will be optional in FY 2021-22 and mandatory in FY 2022-23 For the top 1,000 listed businesses by market capitalization. This gives organizations that are subject to these rules enough time to adjust to the new standards. Companies are encouraged, however, to adopt the BRSR as soon as possible in order to be among the first to report on sustainability.

- The new reporting rules encourage listed firms in India to provide transparent, uniform disclosures on ESG metrics and sustainability-related risks and opportunities.

This strategy will assist organizations in better demonstrating their sustainability aims, position, and performance to the market, resulting in long-term value creation and improving investors’ capacity to make educated ESG-related decisions.

Popular blog:-