All About GST on rental property

Page Contents

Overview on GST on property rental

The GST has affected the impacted the real estate sector and aspects such as sales, purchases, buildings, rents, renting, and so on like other economic industries. Furthermore, a number of GST regulatory provisions on rental income have been laid down, for example on the place of supply, on taxable GST services, on exemptions from GST, etc.

With the implementation of GST in India, a structured system of collecting taxes from different sectors has come into place. The renting of real estate is no exception to this new development. Before going ahead, let us first know what real estate means.

It’s like a piece of land or house that cannot be transported unless it has changed and destroyed, as an object or property fixed to the Earth. GST shall apply to immovable characteristics. CGST, SGST, or IGST shall depend on where the service is provided, for the type of GST charged.

Under the GST regime, the mechanism for property owners has changed entirely. Following the introduction of GST, the threshold limit was raised to Rs. 20 Lakhs, from 10 lakhs paid under the old tax regime.

This arrangement helps several landlords stay out of the GST area and is no tax on rental income up to 20 lakhs. GST’s rental applicability depends on the nature of the asset or property.

Different services for the rental of real estate is covered as under:

Residential or Commercial Rental of Immovable Property:

- The taxable limit is increased to 20 lakhs after implementation of the GST The taxability of rent also depends on the type of property from which it was acquired.

- In accordance with the Central Tax Notice 12/2017 of 28-06-2017, rental of residential property is GST-free. However, commercial property rental is taxable in compliance with GST.

Renting of a religious place:

Goods and Services Tax Act has given relief to religious organizations & trust. if such religious organization & trust is registered U/s 12AA of the I Tax Act & also prescribed other condition as explained further. As per entry number 13 of notification no 12/ 2017-CT(rate), Services by way of renting of precincts of a religious place meant for Trust registered u/s 10(23C)(v) or authority covered u/s 10(23BBA) of the Income-tax act 1961 or general public owned or managed by a charitable trust registered u/s 12AA as per Income tax :

- In case of renting of community hall or an open area & like where charges are not more than INR 10000 per day

- the renting of rooms where charges not more than Rs. 1000 per day

Hence, as per aforesaid conclusion, we can see that service of renting of the room is exempt if room rent is less than Rs. 1,000 per day and in case service of renting of community hall shall be exempt if the rent per day is not more than Rs. 10,000 per day.

Read more about: ITC on Marketing Expenses/Sales Promotion Scheme

Read more about: All about GST Offenses, Penalties & Appeals

Brief about the conclusion of services relating to immovable property is as follows:

| Kind of Services | GST Exempt / Taxable |

| Renting of precincts of a religious place with rent per day not more than INR 1000 per day by a trust or charitable trust registered u/s 12AA | Exempt |

| Renting of Immovable property for residential purpose | Exempt |

| Renting of Kalyanamandapam or hall or an open area of a religious place with rent per day not more than INR 10,000 per day, by a trust or charitable trust registered u/s 12AA | Exempt |

| Transfer of development rights and floor space index for construction of residential apartments | Taxable |

| Renting of precincts of a religious place with rent per day more than Rs. 1000 per day, by a trust or charitable trust, registered u/s 12AA of the income tax act, 1961 | Taxable |

| Renting of Kalyanamandapam or hall or an open area of a religious place with rent per day more than Rs. 10,000 per day, by the trustor charitable trust, registered u/s 12AA | Taxable |

| Renting of Immovable property for commercial purpose | Taxable |

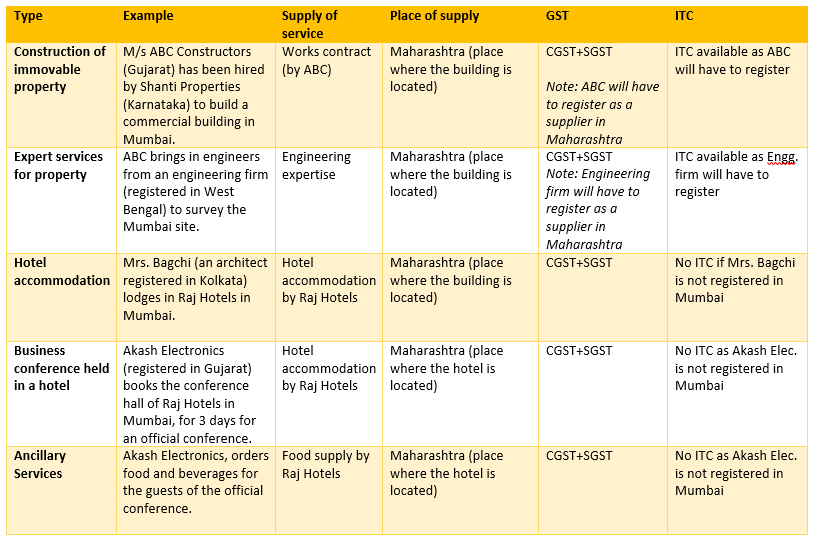

Place of supply in case of Immovable properties:

Brief about the conclusion of services relating of the place of supply relating to immovable property is as follows:

| Place of supply in case location of suppliers and recipient are located in India. | ||

| Service | Place of supply | |

| Services provided in relation to immovable property including services provided by architects, interiors decorators, surveyors, engineers, Other experts or estate agents, service of grants of rights to use immovable property, etc. in India | Location of Immovable property | |

| Where supplier and recipient of service are in India and the immovable property is located outside India | Location of the recipient | |

| Place of supply in case location of suppliers and recipient is located outside India |

| Service | Place of supply |

| Services provided in relation to immovable property including services provided by architects, engineers, interiors decorators, surveyors, Other experts or service of grants of rights to use immovable property, estate agents, etc. outside India | Location of Immovable property |

KAR AAR: GST on Rent received from Backward Classes Welfare Dept.

The Karnataka Authority of Advance Ruling passed an order that No GST shall be levied on the rent received from the ‘Backward Classes Welfare. It is because the hostel works for the welfare of young girls studying in the Backward Classes. The reason is the above-mentioned precedent. The above-mentioned service, therefore, falls purview of Article 243G of the Constitution.

In case Rents the property to the Department of Backward Classes, which in its turn uses it for the benefit of weaker groups from backward class society, so that it provides an exempt service for the post-metric Girl’s Hostel, as covered by Article 243G of the Constitution of India, to Backward Classes Welfare Department.

And the above activity is covered by Notification No. 12/2017-Central Tax (Rate) of 28 June 2017, entry number 3. The service is therefore exempt from the provisions of the CGST Act, 2017. The activity is also exempt pursuant to KGST Act 2017 for similar reasons.

Who must require to be registered under GST if the property is rented out for business purposes?

- A taxpayer that receives more than the exempt threshold must register in accordance with GST and pay taxes as per GST law. Thus it’s taxable if you give your property to a Business. Then Person must register under GST Law. if you receive over Rs 20 lakh as rent from the same one.

All the below States for which Thresh-hold for GST Registration is INR 10,00,000/-: Uttarakhand, Manipur, Meghalaya, Arunachal Pradesh, Mizoram, Nagaland, Sikkim, Tripura, Assam, Jammu & Kashmir, Himachal Pradesh,

For all other states – the threshold limit is INR 20,00,000/-

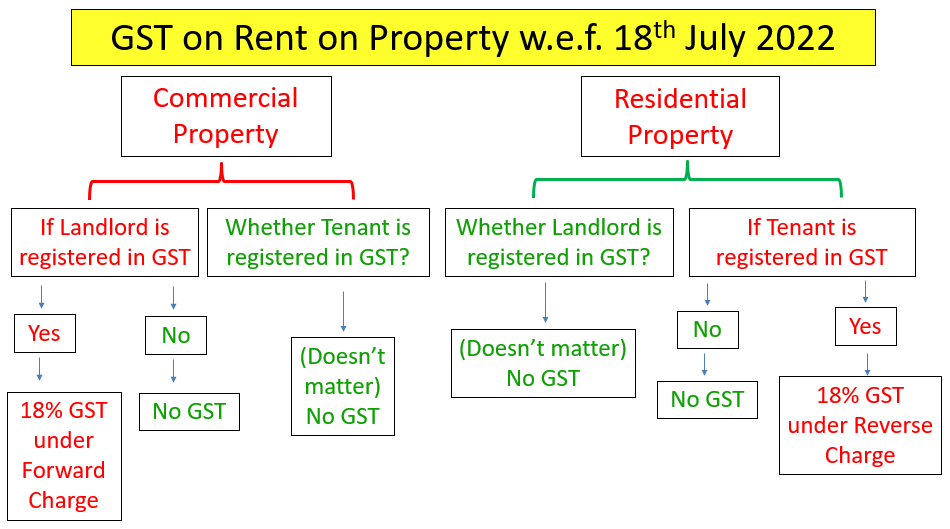

How GST is calculated to be made, In case Renting a property for commercial use?

- GST will be 18 percent of the taxable value and rent would be treated as a taxable supply of service for all commercial spaces rented.

- If a registered charitable trust or a religious trust owns and manages a religious place meant for the public then it is exempt from GST.

- These rooms are rented for less than Rs. 1000 per daily – business rental is lower than Rs. 10,000 per month –

- Community halls or open areas are rented at less than Rs 10,000 per day

Input Tax Credit provisions on GST payable on the rent.

- If a Person pays GST for rent, his other tax dues can normally receive credit for taxes paid. In other words, if it’s Input Tax Crédit is satisfied with all provisions, ITC may be requested on GST payable on the rent.

Commission Paid to Broker

- The commission paid by the landlord to the real estate broker is covered by GST. The courier must be registered with GST and the landlord should collect GST. GST applies even if the residential real estate commission is paid.

How to Raise Invoice for GST on Rent?

- If GST has been paid in respect of rental, the property owner has to prepare an appropriate GST Invoice, clearly specify the invoice No, invoice date, rent received, GST rate, and a number of other items, pursuant to Invoice Rules.

- No format for raising the GST Invoice is prescribed by the government. The Govt has ordered certain items to be included in the invoice. It is not mandatory to locate these items. In addition, the landlord is free to mention any items other than the Govt’s mandate.

GST Compliance:

- GST returns should be filed by the landlord & the GST collected by the Govt based on the GST Return filing schedule deposit.

Reverse Charge Mechanism under GST

- According to the GST Act, if a registered person is rented by the government or the local authorities, the GST is paid in return by the tenant. In the event that the tenant is unregistered, GST under the forward charge mechanism is collected by the Govt.

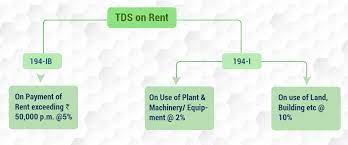

Provision for a TDS on income tax for the rented property:

- The property’s owner (payable on rent) must collect the GST from the payer. If the rent for property exceeds Rs. 2.40 lakh/year from AY 20-21, the payer of the rent must deduct income tax at the source of 10 percent. The TDS applies to both residential and business property. TDS is not going to have GST.

Recalling important point: In accordance with the reverse charge mechanism(RCM), GST on rents charged to a registered person for immovable properties by the government or local authority. But the government would deduct GST itself if the property is rented to an unregistered person (Forward charge mechanism).

54 GST Council Meeting amendment | GST में Commercial property पर लगेगा RCM

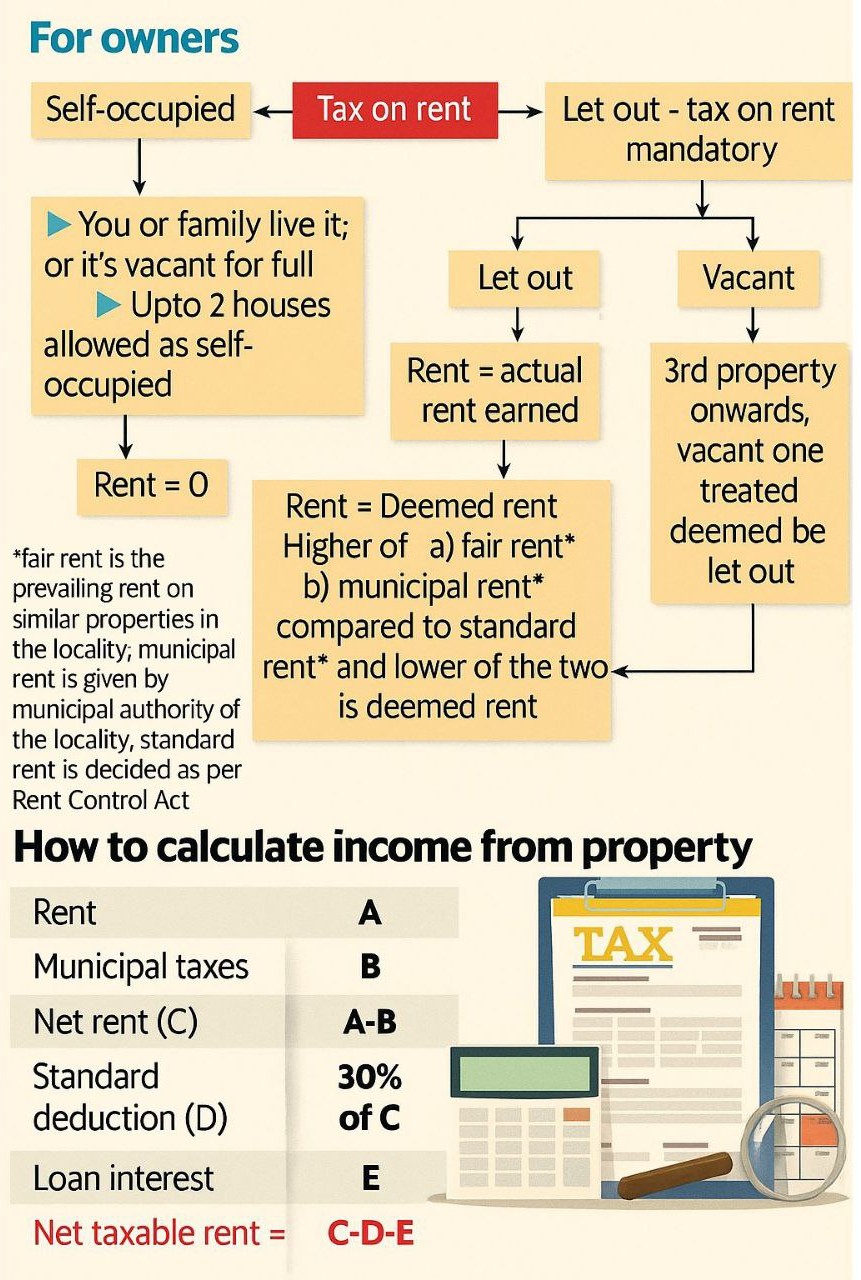

How income from house property is calculated for tax purposes in India.

Types of Property Usage & Rent Calculation- Let me break it down for you:

-

Self-Occupied Property

- If you or your family live in the house, or it’s vacant for the full year,

then it is treated as self-occupied. - Up to 2 houses can be treated as self-occupied.

- Rent = ₹0

- If you or your family live in the house, or it’s vacant for the full year,

-

Let-Out Property

- Property is rented out.

- Rent = Actual rent received

- Tax on rent is mandatory.

- If the property is rented, then tax is mandatory on rent received & Rent is calculated as Actual Rent Earned.

-

Vacant Property (Deemed Let-Out)- (3rd House Onwards)

- Vacant Property From the 3rd property onwards, if the house is vacant, it will be treated as deemed to be let out.

- Rent = Deemed rent, which is:

- Higher of: Fair rent or Municipal rent

- Compared to: Standard rent (as per Rent Control Act)

- Lower of the two is considered as deemed rent..

-

Income Calculation Formula

-

- Rent (A) – Actual or deemed rent

- Municipal Taxes (B) – Paid by owner

- Net Rent (C) = A − B

- Standard Deduction (D) = 30% of C

- Loan Interest (E) – Interest paid on home loan

Net Taxable Income from Property = C − D − E. So, the taxable income from property is computed after considering municipal taxes, 30% standard deduction, and interest on housing loan.

Rajput Jain and Associates provides clients with adequate support and guidance from our side in dealing with various GST issues (GST registration, filing of GST declarations, requesting refunds, and GST audits). Contact us if you have a question or want to know more about GST cancellation.